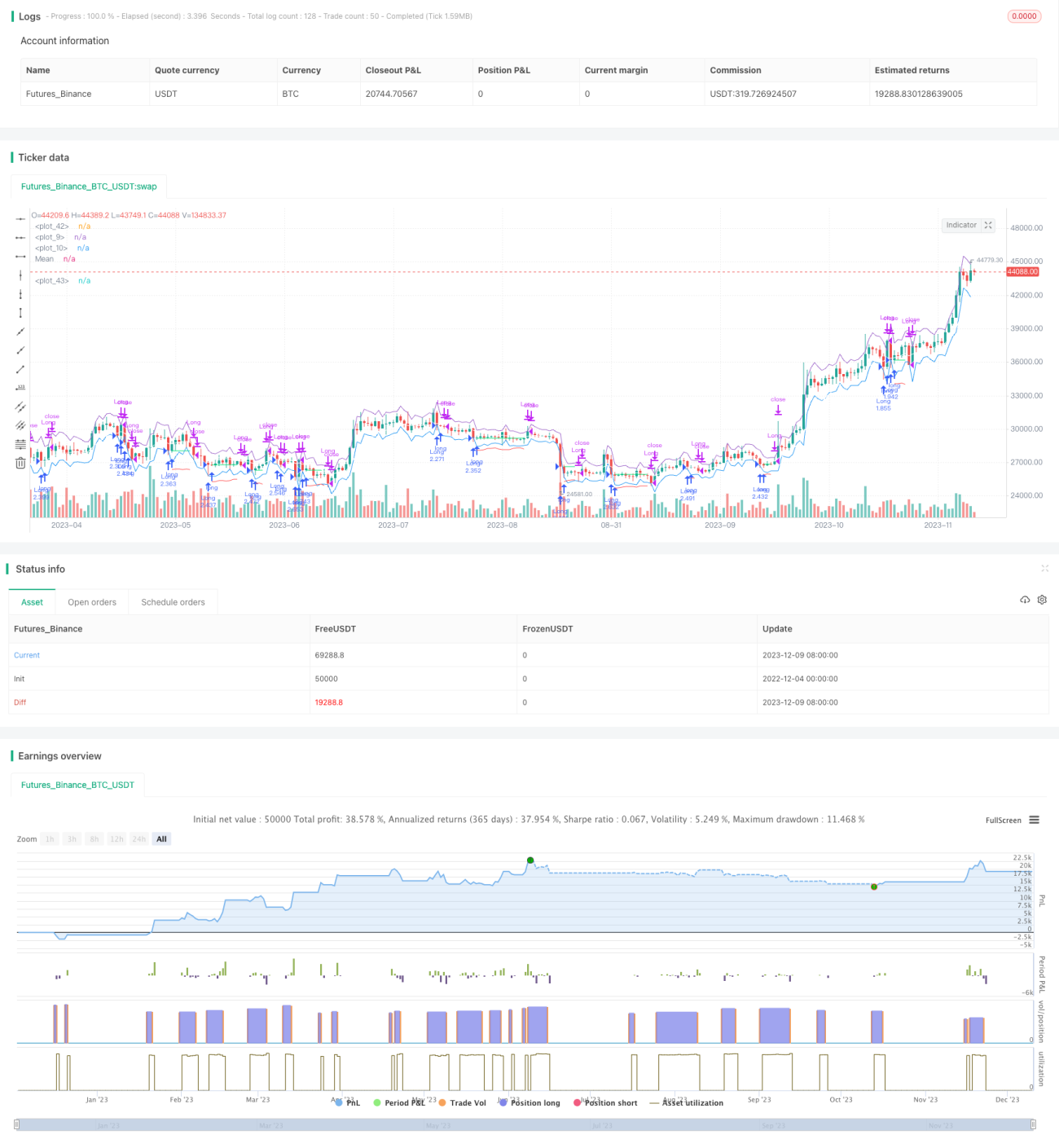

ATR Channel Mean Reversion Quantitative Trading Strategy

Overview

This is a long-only strategy that identifies entry signals when prices break below the lower band of the ATR channel, and takes profit when prices reach the middle band (EMA) or upper band of the ATR channel. It also uses ATR to calculate stop loss levels. This strategy is suitable for quick short-term trades.

Strategy Logic

When the price breaks below the lower ATR band, it signals an anomaly drop. The strategy will go long at the next candle's open. The stop loss is set at entry price minus ATR stop loss multiplier times ATR. Take profit is at the middle band (EMA) or upper ATR band. If current bar's close is lower than previous bar's low, then use previous bar's low as take profit.

Specifically, the key logic includes:

- Calculate ATR and middle band (EMA)

- Define time filters

- Identify long signal when price < lower ATR band

- Enter long at next bar's open

- Record entry price

- Calculate stop loss price

- Take profit when price > middle band (EMA) or upper ATR band

- Stop out when price < stop loss price

Advantage Analysis

The advantages of this strategy:

- Uses ATR channel for reliable entry and exit signals

- Only long after anomaly drop avoids chasing highs

- Strict stop loss controls risk

- Suitable for quick short-term trades

- Simple logic easy to implement and optimize

Risk Analysis

There are some risks:

- High trading frequency leads to higher transaction costs and slippage

- Consecutive stop loss triggers may happen

- Inappropriate parameter optimization impacts performance

- Large price swings may result in oversized stop loss

These risks can be reduced by adjusting ATR period, stop loss multiplier etc. Choosing brokers with low trading fees is also important.

Optimization Directions

The strategy can be improved by:

- Adding other filter indicators to avoid missing best entry signals

- Optimizing ATR period

- Considering re-entry mechanism

- Adaptive stop loss size

- Adding trend filter to avoid counter-trend trades

Conclusion

In summary, this is a simple and practical mean reversion strategy based on ATR channel. It has clear entry rules, strict stop loss, and reasonable take profit. There is also room for parameter tuning. If traders can choose the right symbol and control risk with stop loss, this strategy can achieve good results.

- 1