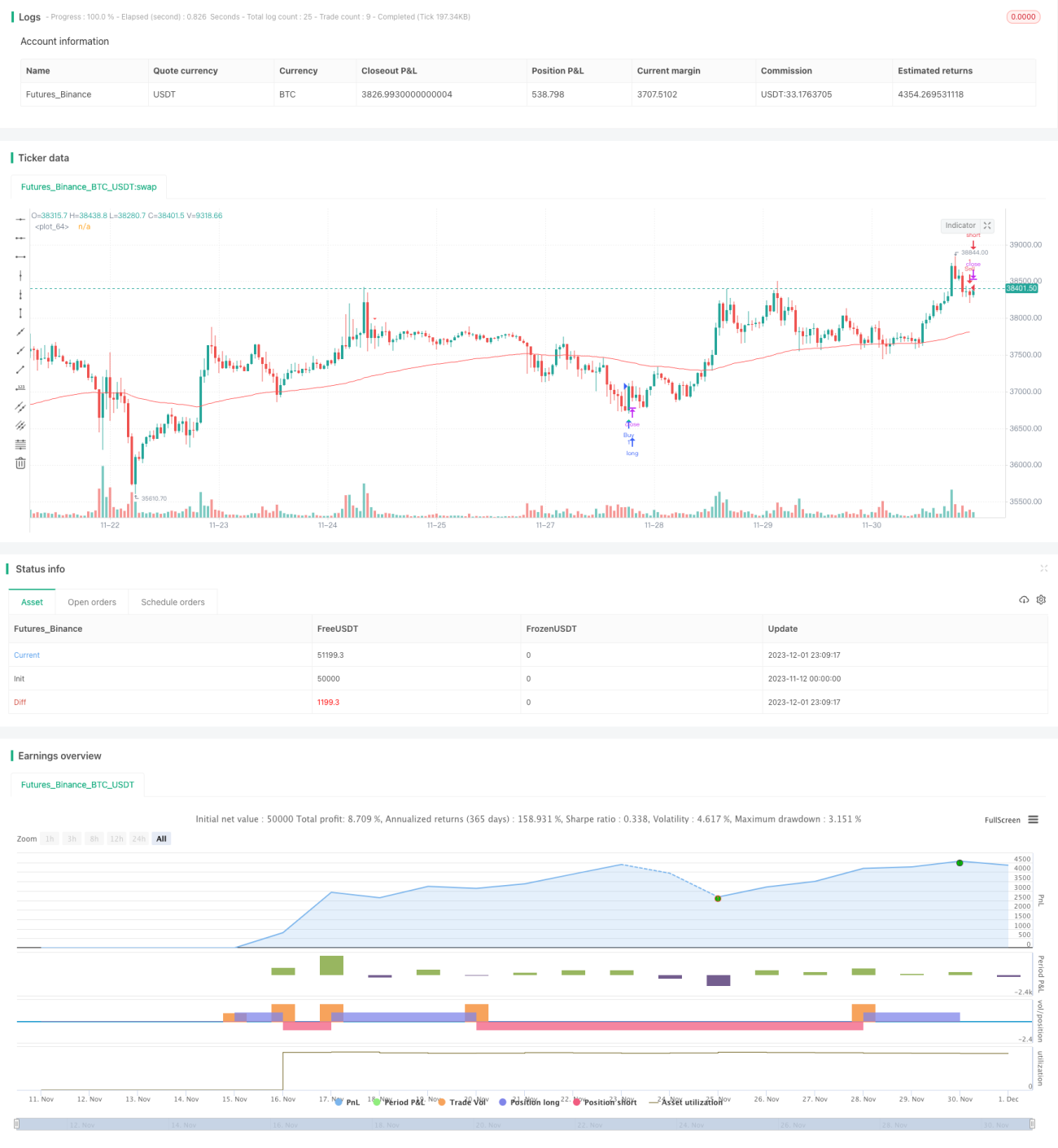

Reverasal Indicator Strategy

Overview

This is a revasal trading strategy based on multiple technical indicators. It combines CCI, Momentum indicator, RSI and other indicators to identify potential long and short trading opportunities. The strategy generates trading signals when indicators show overbought/oversold signals and prices pull back.

Strategy Logic

The strategy's trading signals come from a custom indicator called "Edri Extreme Points Buy & Sell". It takes into account CCI, Momentum indicator and RSI crossovers. Specific logics are:

Long signal conditions:

- The "Edri Extreme Points Buy & Sell" indicator triggers a buy signal, i.e. CCI crossing above 0 or Momentum crossing above 0, and RSI is below oversold level.

- The price pulls back to or below the 100-period EMA.

Short signal conditions:

- The "Edri Extreme Points Buy & Sell" indicator triggers a sell signal, i.e. CCI crossing below 0 or Momentum crossing below 0, and RSI is above overbought level.

- The price pulls back to or above the 100-period EMA.

The strategy can also be configured to find regular bullish/bearish divergences, generating trading signals only when RSI diverges significantly from price.

When trading signals are triggered, the strategy sets stop loss at entry price ± 2ATR, take profit at entry price ± 4ATR. This allows reasonable stop loss and take profit range based on market volatility.

Advantage Analysis

- Combining multiple indicators avoids false signals from a single indicator.

- Reversal trading style catches mid-term opportunities in range-bound markets.

- ATR-based stop loss and take profit can adjust positions based on market volatility.

- Finding divergence avoids opening positions without extreme overbought/oversold levels.

Risk Analysis

- Improper indicator parameters may lead to missing opportunities or too many wrong signals.

- Reversal trading may cause consecutive stop loss in trending markets.

- ATR has lagging effect and cannot update stop loss/take profit timely in fast-moving markets.

Solutions:

- Backtest and optimize indicator parameters to find the best combination.

- Consider suspending the strategy when trend is strong.

- Combine with other stop loss methods like moving stop loss or contrarian stop loss.

Optimization Directions

- Test different parameter combinations of CCI, Momentum length, RSI parameters, ATR multiplier etc.

- Add other filtering conditions like price patterns, volume changes etc.

- Adjust position sizing rules like ATR-based position ratio.

- Set parameter templates for different products and timeframes.

- Consider adding trend tracking to suspend reversal trading in trending markets.

Summary

The strategy mainly works for range-bound markets, capturing mid-term reversals for relatively steady gains. It helps identify short-term price stretches and generates trading signals based on multiple indicators. With proper optimization and risk management, its advantages can be effectively utilized. Still be aware the intrinsic weaknesses of reversal trading, the possibility of continuous losses in strong trends. Overall the strategy suits investors with some quant and risk management experience.

- 1