Momentum Breakout and Trend Following Combination Strategy

Overview

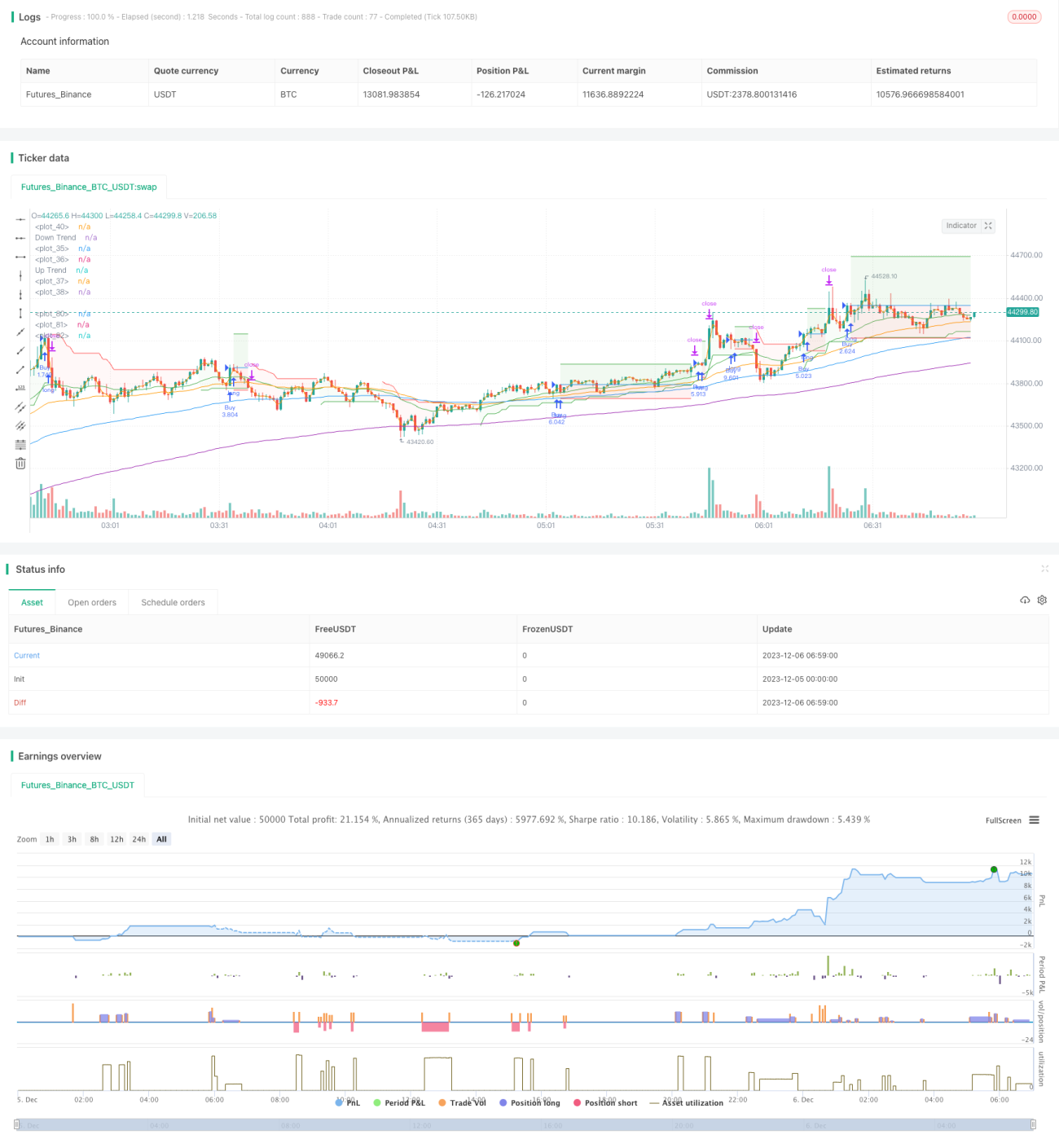

This strategy is a combination strategy that integrates momentum indicators, trend following indicators and moving average indicators to realize trend following and breakout entry/exit. It mainly uses the combination of Stochastic indicator and Supertrend indicator to determine entry/exit timing, and uses EMA lines to judge the main market trend.

Strategy Principle

The strategy consists of the following indicators:

-

EMA lines: Use EMA 25, 50, 100 and 200 to determine the main trend. When EMA25 crosses above EMA50 and EMA100 crosses above EMA200, it is an upward trend, otherwise it is a downward trend.

-

Supertrend trend following indicator: Parameters are Factor 3 and ATR 10 to judge whether the current price is in an uptrend or a downtrend. When Supertrend is green, it is an uptrend. When it is red, it is a downtrend.

-

Stochastic momentum indicator: %K 8 and %D 3 to determine if Stochastic generates golden cross or dead cross. When %K line crosses %D line from below, it is a golden cross signal, and vice versa for dead cross.

The buy strategy is: EMA shows uptrend + Supertrend shows uptrend + Stochastic golden cross.

The sell strategy is: EMA shows downtrend + Supertrend shows downtrend + Stochastic dead cross.

This strategy integrates trend, momentum and breakout indicators to reliably determine market moves and trading points.

Advantage Analysis

The main advantages of this strategy are:

-

Combining multiple indicators improves robustness and filters out fake breakouts effectively.

-

Adding momentum indicator can early spot turning points.

-

Customizable parameters suit different market environments.

-

Realizes relatively efficient stop loss and take profit setting.

-

Works well when backtested on high timeframes like daily.

Risk Analysis

There are also some risks:

-

Improper parameter settings may cause too frequent trading or unstable signals. Parameters need to be optimized.

-

There can still be misjudgements in timing. More filter indicators may be added.

-

Stop loss set on Stochastic extremes may be too close. Wider stop is worth testing.

-

Insufficient backtest data may cause bias in parameter fitting. Expand backtest period.

Optimization Directions

The strategy can be optimized in the following ways:

-

Test more parameter sets to find optimum. E.g. adjust Supertrend Factor.

-

Add more filter indicators like energy or volatility to reduce misjudgements.

-

Test different stop loss ways, e.g. percentage-based stop loss.

-

Optimize take profit, like trailing stop to lock in more profits.

-

Expand scope, adapt to more products or higher timeframes.

Conclusion

The strategy's logic is clear and indicator selection reasonable. It realizes trend following and momentum breakout trading with good backtest results. But there is still room for optimization, e.g. parameter tuning, adding filters, improving stops and profit taking. Multi-dimensional optimization can make the strategy more robust.

- 1