Momentum Breakout Strategy

Overview

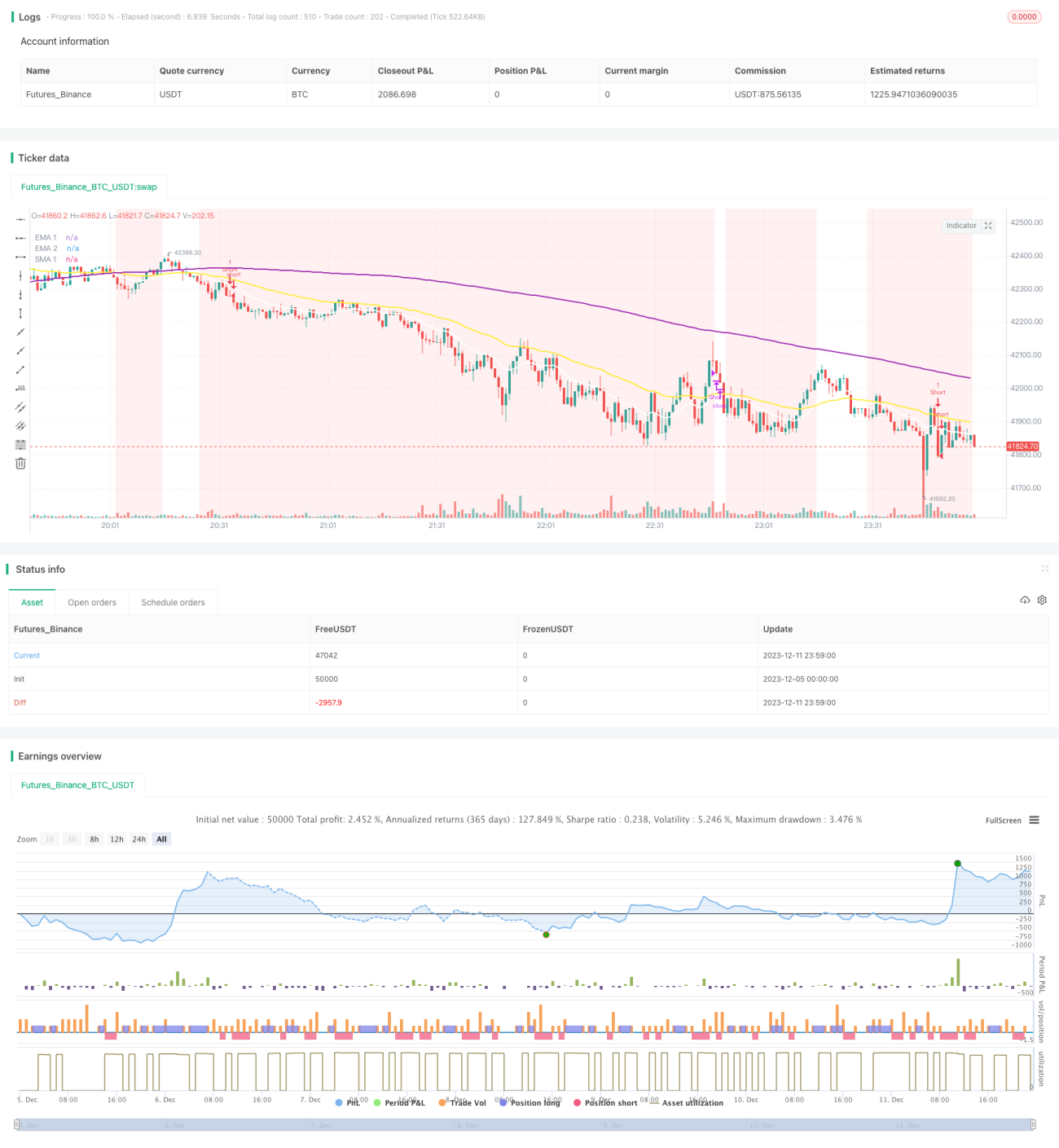

This strategy combines moving average, Laguerre RSI indicator and ADX indicator to implement breakout trading. It goes long when the fast moving average crosses above the slow moving average, Laguerre RSI is greater than 80, and ADX is greater than 20; it goes short when the fast moving average crosses below the slow moving average, Laguerre RSI is less than 20, and ADX is greater than 20. This strategy captures the momentum characteristics of the market and enters the market at the beginning of trend development.

Principle

The strategy mainly uses the following indicators to determine trends and entry timing:

-

Moving average combination: 16-day EMA, 48-day EMA, 200-day SMA. An uptrend is determined when the short-term average crosses above the long-term average, and a downtrend when crossing below.

-

Laguerre RSI indicator to determine overbought and oversold zones. RSI greater than 80 is a long signal, and less than 20 a short signal.

-

ADX indicator to determine trend status. ADX greater than 20 indicates a trend, suitable for breakout trading.

Entry signals are determined by the direction of the moving average combination, entry timing by the Laguerre RSI, and non-trending markets are filtered out by the ADX. Exit signals are generated when the moving averages cross back. The overall strategy judgment framework is quite reasonable, with the different indicators working together to determine long/short entries and exits.

Strengths

The advantages of this strategy include:

-

Catching trend momentum: The strategy only enters the market at the start of trend development, capturing exponential profits from trends.

-

Limited losses: Stop losses set appropriately limit losses from individual trades. Even losing trades have chances of making profits.

-

Accurate combined indicators: The moving averages, Laguerre RSI and ADX can relatively accurately determine market direction and entry timing.

-

Simple implementation: The strategy only uses 3 indicators and is easy to understand and implement.

Risks

There are also some risks to the strategy:

-

Trend reversal risks: As a trend following strategy, large losses can occur if trend reversals are not detected in time.

-

Drawdown risks: In ranging markets, stops can be hit leading to account drawdowns.

-

Parameter optimization risks: Indicator parameters need to be adjusted for different markets to avoid failures.

Countermeasures:

-

Strict stop losses to limit single trade loss amounts.

-

Optimize indicator parameters and breakout thresholds.

-

Use futures hedging etc. to manage drawdowns.

Optimization Directions

Some ways to optimize the strategy include:

-

Parameter optimization: Test combinations of moving average periods, Laguerre RSI parameters, ADX parameters to find optimum settings.

-

Breakout optimization: Test different moving average breakout thresholds to balance trade frequency and profitability.

-

Entry optimization: Test other indicators combined with Laguerre RSI for more accurate entry timing.

-

Exit optimization: Research other exit signals in combination with moving averages.

-

Profit taking vs. stop loss optimization: Test different strategies to optimize returns.

Summary

In summary, this strategy effectively captures trending moves by using the combination of moving averages, Laguerre RSI and ADX to determine entries and exits. By entering early in trend developments and closely following the trend runs, exponential profits can be made, while stop losses help limit losses. The strategy suits investors comfortable making market judgments, as well as those doing automated trading after parameter optimization. Overall the strategy has strong practical utility.

- 1