Super Trend LSMA Long Strategy

Overview

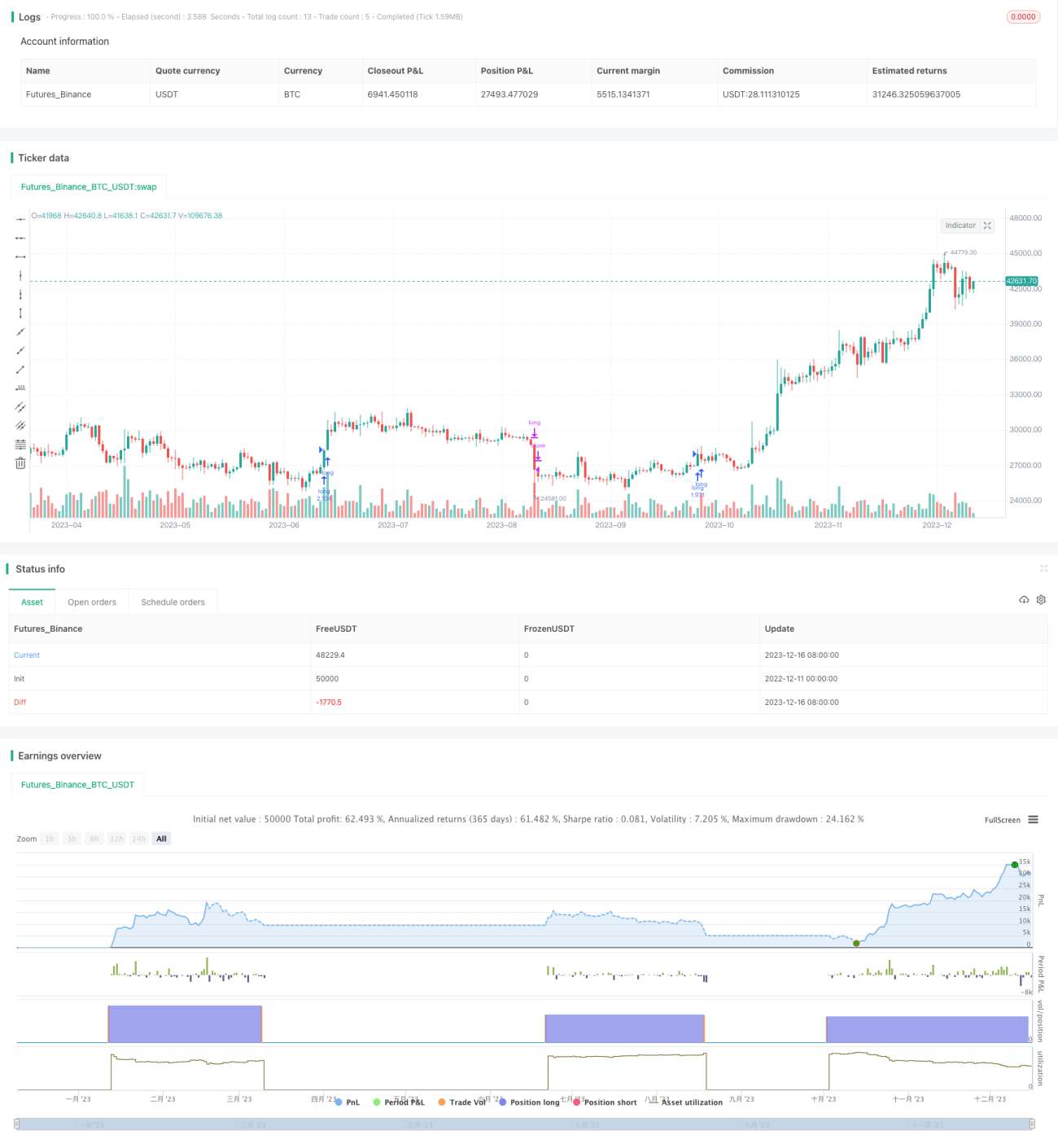

The Super Trend LSMA Long Strategy is a long strategy that combines the Super Trend indicator with the LSMA moving average. It is suitable for long-term trending markets such as stocks and cryptocurrencies, and works better under larger time frames.

Strategy Logic

The trading rules of this strategy are as follows:

Long entry signal: When the Super Trend indicator gives a long signal and the closing price is above the LSMA moving average, go long.

Long exit signal: When the Super Trend indicator gives a short signal, close the long position.

That is, the Super Trend is used to determine the overall trend direction, while the LSMA is used to determine specific entry points.

Advantage Analysis

This strategy combines trend following with moving averages. It can both catch the big trend and use the moving average to filter out false signals, thus avoiding being trapped. Compared with using only a single trend indicator or moving average, it has better risk control.

In addition, the Super Trend itself has some laggingness. Combined with the smoothing feature of LSMA, it can effectively filter out market noise and avoid being misled by false breakouts.

Risk Analysis

The biggest risk of this strategy is the inability to accurately determine trend reversal points. Due to the lagging of Super Trend and LSMA, losses may be magnified when the trend changes. Timely stop loss should be used to control risks.

In addition, parameter settings also affect strategy performance. If ATR parameters or factor parameters are set improperly, the effectiveness of Super Trend will be compromised. If the LSMA period is set too short, the filtering effect will be poor and it will be vulnerable to noise. Therefore, parameter optimization is crucial.

Optimization Directions

This strategy can be optimized in the following aspects:

-

Use machine learning algorithms to automatically optimize parameters to better suit different market environments.

-

Add stop loss mechanisms. Mandatory liquidation when losses reach a pre-set stop loss level.

-

Add position management module. Appropriately increase positions when major trends form, and reduce positions when trends end.

-

Add more filtering indicators, such as volatility indicators, volume indicators etc, to avoid trend reversal risks.

-

Use deep learning models instead of simple Super Trend to judge trends, making trend determination more intelligent.

Conclusion

The Super Trend LSMA Long Strategy integrates the advantages of trend tracking indicators and moving average indicators. It can catch the big picture over longer periods of time, and use moving averages to filter out noise. With parameter optimization, stop loss mechanisms, stronger risk control modules, the profitability and risk control capabilities of this strategy can be further enhanced, making it a very practical quantitative strategy.

/*backtest

start: 2022-12-11 00:00:00

end: 2023-12-17 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title = "Supertrend LSMA long Strategy", overlay = true, pyramiding=1,initial_capital = 100, default_qty_type= strategy.percent_of_equity, default_qty_value = 100, calc_on_order_fills=false, slippage=0,commission_type=strategy.commission.percent,commission_value=0.1)

- 1