Momentum TD Reversal Trading Strategy

Overview

The Momentum TD Reversal Trading Strategy is a quantitative trading strategy that utilizes the TD Sequential indicator to identify price reversal signals. This strategy is based on momentum analysis and takes long or short positions after confirming the price reversal signals.

Strategy Logic

This strategy uses the TD Sequential indicator to analyze price fluctuations and identify the price reversal pattern after 9 consecutive candlesticks. Specifically, when it detects a downturn candlestick after 9 consecutive rising candlesticks, the strategy determines it as a short opportunity. On the contrary, when it identifies an upturn candlestick after 9 consecutive falling candlesticks, the strategy regards it as a long opportunity.

By leveraging the advantage of the TD Sequential indicator, the strategy can capture price reversal signals ahead of the market. Together with the chase-rise-kill-drop mechanism in this strategy, it can timely establish long or short positions after confirming the reversal signals, so as to obtain relatively better entry opportunities at the beginning stage of price reversals.

Pros Analysis

- Use the TD Sequential indicator to identify price reversal opportunities in advance

- Establish the chase-rise-kill-drop mechanism to determine the confirmation of price reversals more timely

- Enter positions at the forming stage of reversals to obtain relatively better entry points

Risks Analysis

- TD Sequential indicator may have false breakouts. Other factors are needed to confirm the signals

- Appropriately control the position sizing and holding period to mitigate risks

Optimization Directions

- Incorporate other indicators to validate reversal signals to avoid false breakout risks

- Establish stop loss mechanism to control single trade loss

- Optimize position sizing and holding period to balance profit scale and risk management

Conclusion

The Momentum TD Reversal Trading Strategy utilizes the TD Sequential indicator to judge price reversals beforehand and establishes positions swiftly after confirmations, making it very suitable for momentum traders. This strategy has the advantage of identifying reversal opportunities, but still calls for proper risk control to avoid huge losses caused by false breakouts. With further optimizations, it can become a balanced strategy regarding risk-reward ratio.

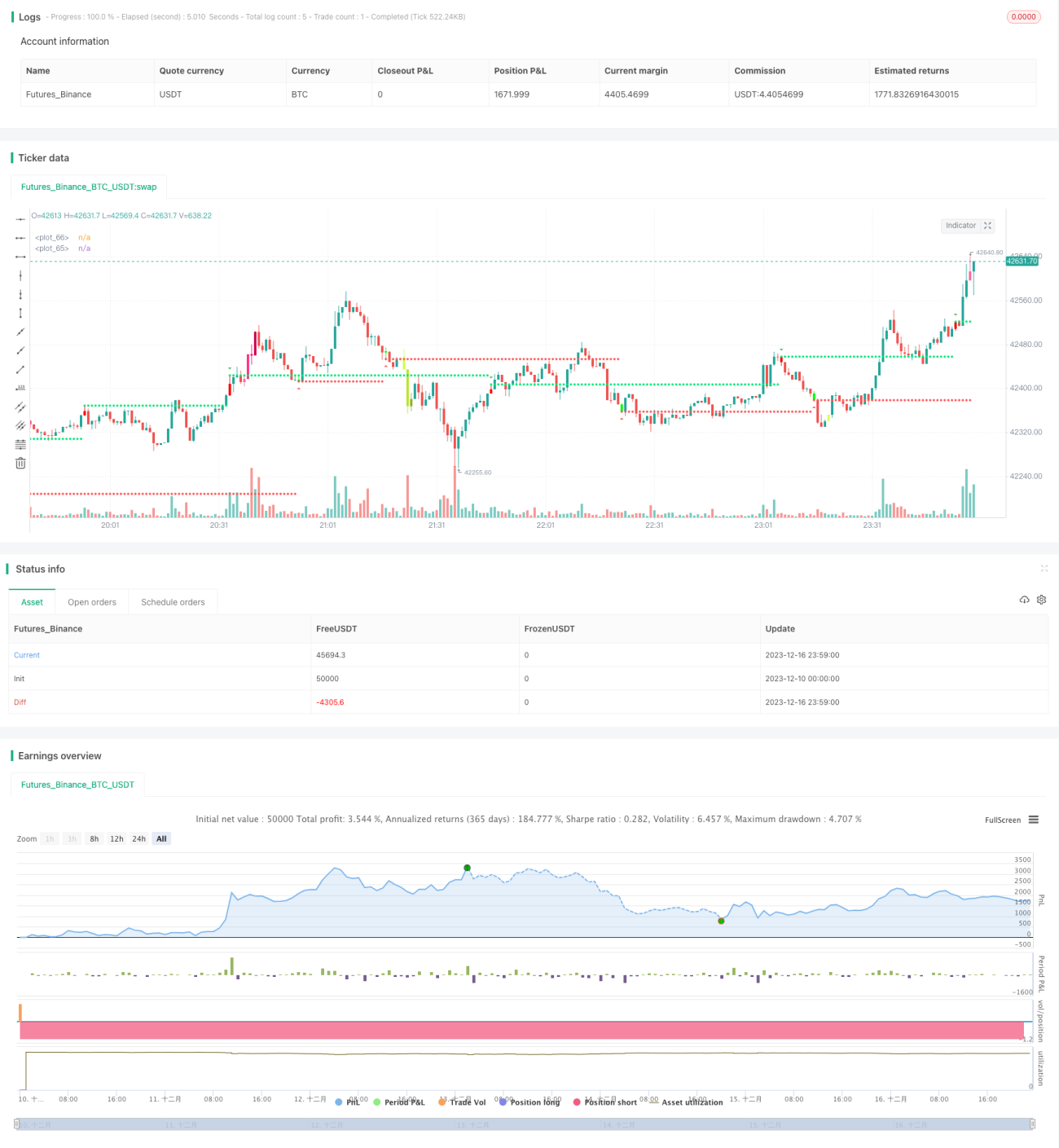

/*backtest

start: 2023-12-10 00:00:00

end: 2023-12-17 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//This strategy is based on TD sequential study from glaz.

//I made some improvement and modification to comply with pine script version 4.

//Basically, it is a strategy based on proce action, supports and resistance.- 1