Ichimoku Moving Average Crossover Strategy

Overview

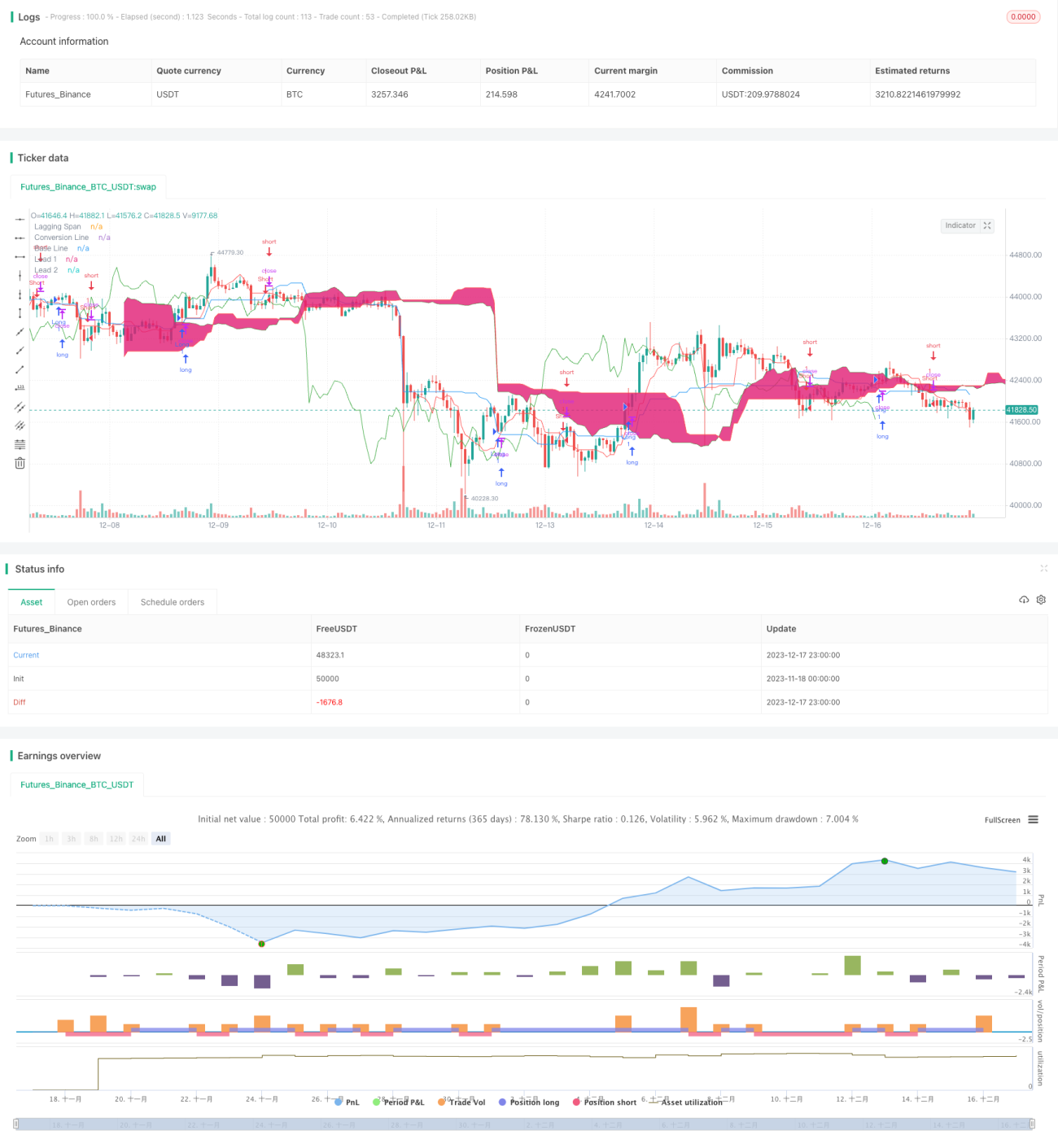

The Ichimoku moving average crossover strategy identifies long and short signals by calculating a set of moving averages and detecting price crosses. This strategy combines multiple technical indicators and provides solid and reliable trading for middle-to-long term operations.

Strategy Logic

The Ichimoku strategy utilizes a specialized system consisting of 5 moving average lines, namely the conversion line, base line, leading span 1, leading span 2, and lagging span. Specifically, the conversion line depicts recent price momentum, the base line shows the medium-to-long term trend, the leading lines combine the conversion and base to predict future moves, and the lagging span displays past prices for reference. Trading signals are generated when the price breaks through the base line. The strategy also incorporates body filters and candlestick colors to avoid false breaks.

Advantages

The Ichimoku strategy amalgamates the strengths of various technical indicators into one system. It fuses concepts of moving averages, price channels, volume confirmation etc., forming a systematic methodology. This ensures accuracy and directionality of the trading signals. Compared to single-indicator strategies, it greatly reduces false signals and increases profit factors.

Risks

As a trend following system, the Ichimoku strategy has relatively long trading intervals. This means short-term price oscillations cannot be captured. Also, moving averages fail when prices fluctuate violently. Such situations can lead to wrong signals and losing trades. It is advisable to use stops to control risks.

Enhancement Opportunities

The Ichimoku strategy can be improved in areas like: 1) Adjusting average parameters for different periods and products; 2) Incorporating volume indicators to confirm price-volume relations; 3) Introducing machine learning models to refine signal determination; 4) Adding more filters to lower incorrect trade probability.

Conclusion

The stable and reliable Ichimoku moving average crossover strategy is suitable as a core strategy combined with other algorithms. Its clear trend guidance and flexibility owing to parameter tuning and multi-indicator optimization make it worthwhile for in-depth research and long-term application by quant traders.

- 1