Meticulous EMA Crossover Strategy

Overview

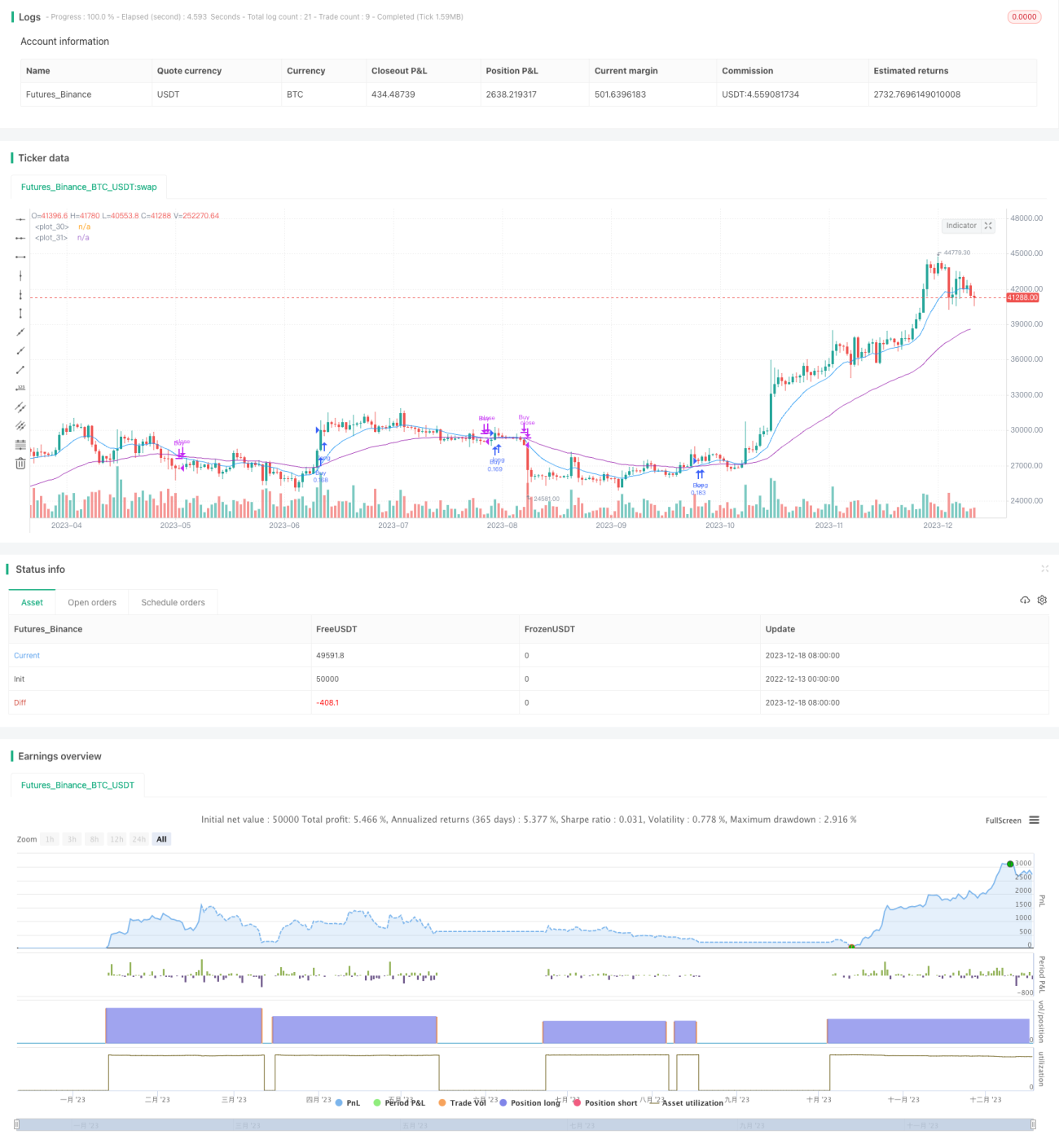

The Meticulous EMA Crossover Strategy is a trend trading system based on the crossover signals between two exponential moving average lines (EMAs) with different parameter settings. It uses a shorter-period fast EMA line and a longer-period slow EMA line and generates trade signals when they cross over. A long signal is triggered when the fast line crosses above the slow line, and a close position signal is triggered when the fast line crosses below the slow line. This system also incorporates risk management means like stop loss, trailing stop to lock profits and control risks.

Strategy Principles

The core indicators of this strategy are two EMA lines: fast line and slow line. The fast line's parameter is defaulted to a 13-period line for faster reaction to price changes. The slow line's parameter is defaulted to a 48-period line for slower responses. When the short-term trend rises rapidly, the fast line will rally ahead of the slow line. And when the prices fall, the fast line will drop faster than the slow line. Therefore, the fast line's crossing above the slow line signals an upward trend, and the fast line's crossing below the slow line signals a downward reversal.

Based on this principle, the strategy goes long when the fast EMA line crosses above the slow EMA line, indicating an upward trend so you can buy. When the fast line crosses below the slow line, it closes positions, showing the end of uptrend and the time to take profit. To control risks, the strategy also sets an initial stop loss at 8% below entry price and a trailing stop defaulted to be 120 points from market price. This allows the system to exit early and minimize losses when there is a trend reversal.

In coding implementation, the "crossover" and "crossunder" functions are used to determine the EMA crossover signals. The corresponding "entry" and "close" commands will then be triggered to buy or close positions.

Advantage Analysis

The Meticulous EMA Crossover Strategy has the following key advantages:

-

The signals are simple and clear, easy to understand and implement. Suitable for beginners.

-

The MA filter can discover trend changes with less market noise.

-

Highly configurable parameters on fast/slow EMA lines, stop loss levels, etc.

-

Stop loss means effectively control risks.

-

Relatively stable system across various market conditions.

Risk Analysis

There are also some inherent risks of this strategy:

-

EMA signals may lag during violent market swings, unable to reflect price changes timely.

-

Overly fast parameter tuning of the MA indicators can produce more false signals.

-

Weak price trends may generate fewer EMA crossovers thus unable to capture moves.

-

No analysis of overall market trends means going against the main trend.

The risks can be mitigated through:

-

Adding filters like MACD and KD to confirm crossover signals.

-

Adjust EMA parameters based on different markets to decrease false signals.

-

Incorporate analysis of overall trend based on long-term moving averages.

Optimization Directions

The strategy can be upgraded from the aspects below:

-

Adding open position filters to avoid overtrading in range-bound markets. Can combine volatility and volume indicators to set position opening threshold.

-

Set stop loss and take profit levels based on swing high/low levels and support/resistance zones for better accuracy.

-

Add a trend module to analyze longer-timeframe trends as filters for short-term signals, avoiding trading against major trends.

-

Use machine learning to train and optimize ideal EMA parameters fitting the practical markets to decrease false signals.

The above are the major directions for improving this basic EMA crossover strategy going forward. Properly combining more technical indicators and risk management means can surely enhance the strategy's efficacy.

Conclusion

The Meticulous EMA Crossover Strategy is a foundational trend following system based on EMA fast and slow line crossovers to determine price trends and incorporates stop loss to control risks. Its signals are simple and clean, easy to understand for beginners, making it one of the typical starter quant strategies. But inherent lags and false signals risks exist. Going forward, introducing more filters and means can better optimize this strategy for more sophisticate market environments and achieve more stable returns.

/*backtest

start: 2022-12-13 00:00:00

end: 2023-12-19 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// *** USE AT YOUR OWN RISK ***

//

strategy("EMA Strategy", shorttitle = "EMA Strategy", overlay=true, pyramiding = 3,default_qty_type = strategy.percent_of_equity, default_qty_value = 10)- 1