Momentum Capture Channel Strategy

Overview

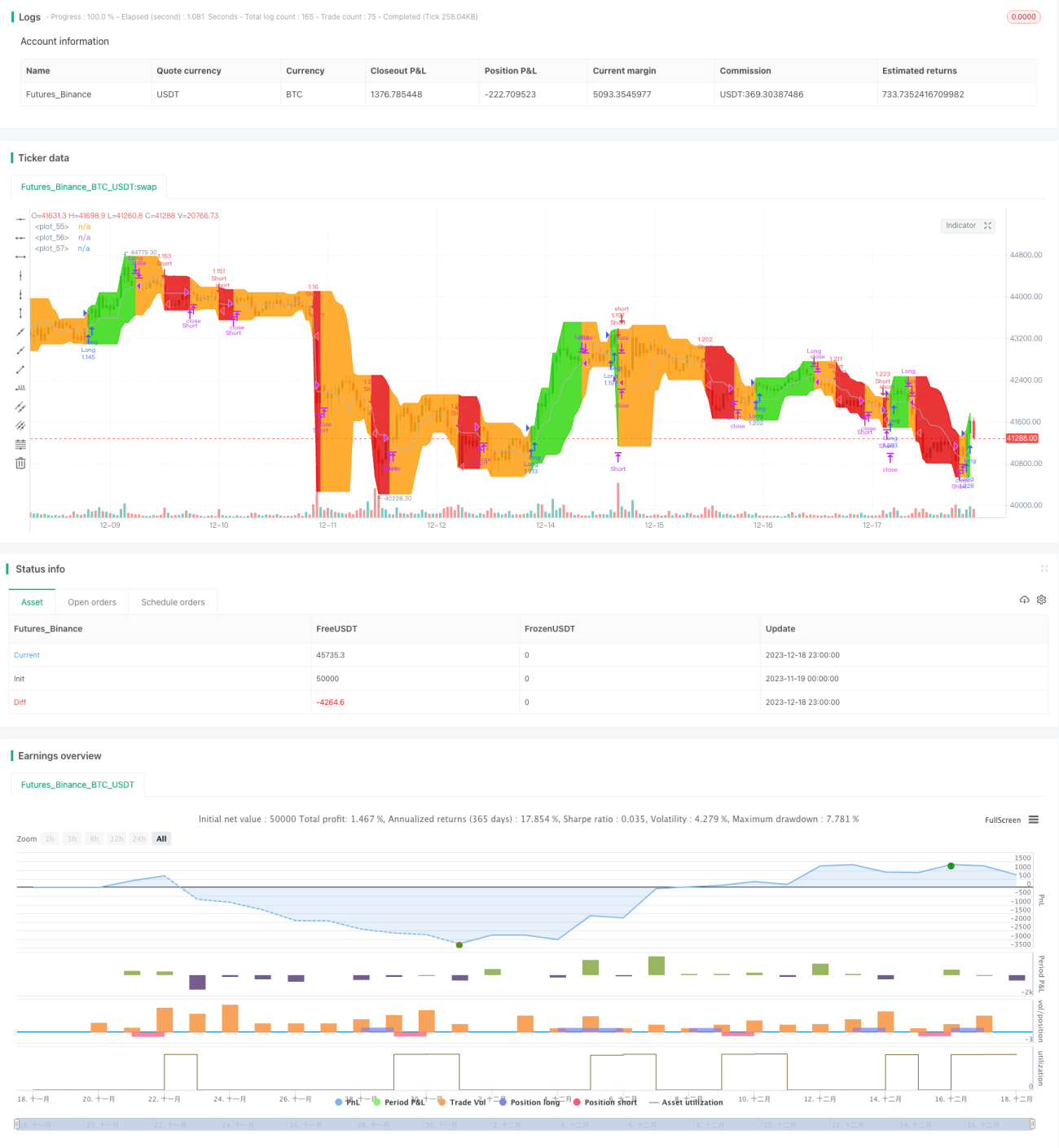

The Momentum Capture Channel Strategy is a variation of the Donchian Channel trading strategy. It consists of a highest-high band, a lowest-low band, and a baseline which averages the highest-high and lowest-low bands. This strategy works very well on trending instruments across weekly and daily timeframes. This is the implementation used in the QuantCT app.

You can set the operation mode to Long/Short or Long-only.

You can also set a fixed stop-loss or ignore it so the strategy acts solely based on entry and exit signals.

Strategy Logic

The core logic of this strategy is based on the Donchian Channel indicator. The Donchian Channel consists of the highest high, lowest low, and closing price average over the past 20 days. Trend direction and potential reversals are judged by price breaking through the upper and lower bands of the channel.

This strategy is a variation on the Donchian Channel. It consists of a highest-high band, a lowest-low band, and a baseline which averages the highest-high and lowest-low bands. The specific logic is:

- Calculate the highest high and lowest low over a certain period as the upper and lower bands of the channel

- Calculate the average of the upper and lower bands as the baseline

- Go long when price breaks above the upper band

- Close long position when price breaks below the baseline

- Go short when price breaks below the lower band (if shorting is allowed)

- Close short position when price reclaims the baseline

The advantage of this strategy is it can effectively capture the momentum of price trends. By waiting for price to break the upper/lower bands to determine the real start of a trend, unnecessary losses from fakeouts can be avoided.

Advantage Analysis

- Captures price trend momentum for profit growth

- Avoids unnecessary losses from being trapped by fake breakouts

- Flexible parameter adjustment makes it suitable for different products

- Can choose Long-only or fully traded to suit different needs

- Integrated stop-loss mechanism effectively controls per trade loss

Risk Analysis

- While capturing trends, failed breakouts also amplify losses

- Stop-loss set too wide could lead to enlarged per trade loss

- Improper parameter settings may lead to overtrading and increased transaction costs

- Breakout signal judgement has some lag, could miss best entry points

Solutions:

- Choose stop-loss percentage carefully to control loss yet give trend enough room

- Increase parameter period values to reduce trading frequency

- Incorporate other indicators to judge signal reliability, select better entry timing

Optimization Directions

- Incorporate other indicators to determine entry timing

- Dynamically adjust stop-loss placement

- Optimize parameter settings based on instrument characteristics

- Incorporate machine learning to judge breakout success rate

- Add position sizing logic

Conclusion

The Momentum Capture Channel strategy provides considerable profit opportunities by capturing price trends. At the same time, it also has certain risks that need to be controlled by properly adjusting parameters. By continually optimizing entry timing selection and stop-loss logic, this strategy can become an excellent trend following system. Its simple trading rules and clear signal judgement make it easy to understand and implement, highly suitable for novice traders.

- 1