Momentum Tracking Trading Strategy

Strategy Overview

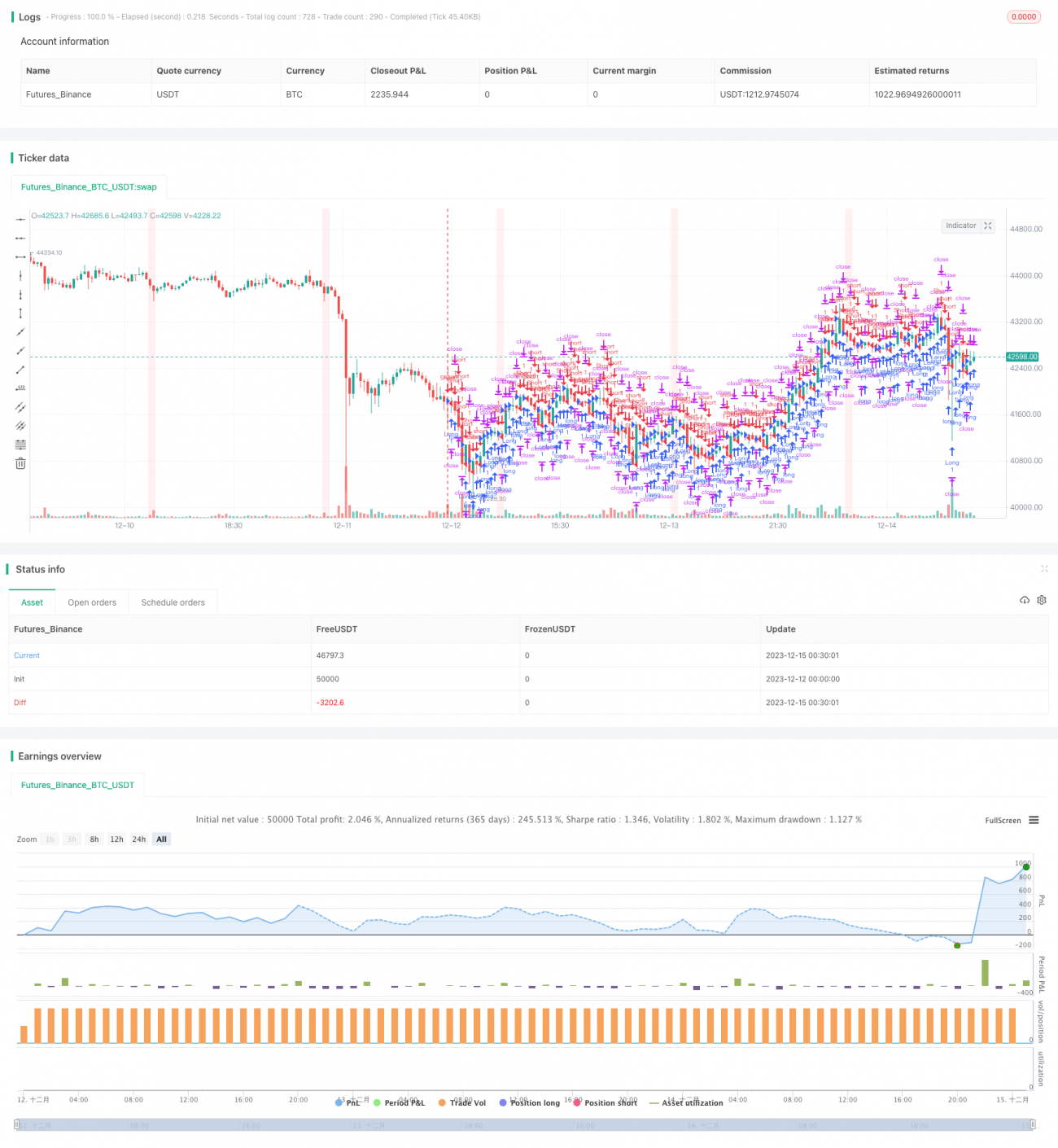

The Momentum Tracking Trading Strategy is an automated trading strategy that mainly tracks market momentum trends and uses multiple technical indicators as auxiliary judgments. This strategy parses K-line information to determine the direction and strength of the current market's main funds, and then issues trading signals based on indicators such as volume price and moving average to achieve trend tracking.

Overall, this strategy is suitable for medium and long term trend trading, and can effectively capture market trends and reduce trading frequency to pursue higher single profits. At the same time, after optimizing the strategy parameters, it can also be used for short-term trading.

Strategy Principle

Main Power Judgement

The core of the momentum tracking strategy is to judge the direction of the market's main funds. The strategy calculates the ATR indicator to monitor the volatility of the market in real time. When volatility increases, it means the main funds are accumulating or distributing, and the strategy will temporarily exit the market to avoid the period when the main funds are operating.

When volatility weakens, it means the main force accumulation or allocation is complete, and the strategy will re-enter the market to determine the specific direction of the main force. The judgment method is to calculate the market's support and pressure positions to see if there are signs of breakthroughs. If there is a clear breakthrough, it will prove that the main funds have chosen that direction.

Auxiliary Judgement

After determining the direction of the main funds, the strategy will also introduce multiple auxiliary technical indicators for verification again to avoid misjudgments. Specifically, MACD, KDJ and other indicators will be calculated to determine whether they are consistent with the direction of the main funds.

Only when the direction of the main funds and auxiliary indicators issue signals in the same direction will the strategy open positions. This effectively controls the trading frequency and only enters at high probability.

Stop Loss Exit

After opening positions, the momentum tracking strategy will track price changes in real time, and use the expansion of ATR values as a stop loss signal. This means that the market has entered the main operating stage again and must exit to cash immediately to avoid being trapped.

In addition, if the price movement exceeds a certain range and then pullbacks, stop loss will also occur. This is a normal technical retracement and needs to be stopped out immediately for risk control.

Advantages of the Strategy

High Systematicness

The biggest advantage of momentum tracking strategies is their high degree of systematization and standardization. Its trading logic is clear, and each entry and exit has clear principles and rules instead of arbitrary trading.

This makes the replicability of this strategy very strong. Users can apply it for long-term use after configuration without manual intervention.

Mature Risk Control

The strategy has built-in multi-level risk control mechanisms, such as main power judgments, auxiliary verification, stop loss line setting, etc., which can effectively control non-systematic risks.

Specifically, the strategy only opens positions in high probability situations and sets scientific stop loss points to maximize avoidance of losses. This ensures stable capital growth.

Relatively Sustainable Returns

Compared to short-term strategies, the holding period of momentum tracking strategies is longer, and each profit is higher. This makes the overall strategy returns more stable and sustainable.

In addition, the strategy tracks medium and long-term trends, which can fully capture the volatility of trends. This is especially noticeable in major trending markets.

Risk Warnings

Difficult Parameter Optimization

The momentum tracking strategy involves multiple parameters, such as ATR parameters, penetration parameters, stop loss parameters, etc. There is a certain correlation between these parameters, requiring repeated testing to find the optimal parameter combination.

Improper parameter configuration can easily lead to excessive trading frequency or insufficient risk control. This requires the user to have certain experience in strategy optimization.

Breakout Trap

When the strategy determines the main power and indicator signals, it relies on the breakthrough of prices to confirm. But there may be false breakouts in penetration operations, which will increase the probability of being trapped.

If a key breakthrough fails, it may lead to greater losses. This is an inherent weakness of the strategy.

Optimization Directions

Introduce Machine Learning

Machine learning algorithms can be used to automatically detect correlations between parameters and find optimal parameter combinations. This is much more efficient than manual testing.

Specifically, the EnvironmentError algorithm can be used to continuously iterate parameters based on reinforcement learning to maximize strategy returns.

Increase Filters

More auxiliary filters can be introduced on the basis of existing indicators, such as trading volume indicators, capital flow indicators, etc., to verify breakthrough signals three or four times to improve reliability.

But too many filters can also lead to missing opportunities. Filter intensity needs to be balanced. In addition, the filters themselves should also avoid correlation.

Strategy Fusion

Combine the momentum tracking strategy with other strategies to take advantage of the strengths of different strategies to achieve orthogonality and improve overall stability.

For example, incorporating short-term reversal strategies and opening reverse trades after breakthroughs can lock in more profits.

Summary

In general, the Momentum Tracking Trading Strategy is a systemized trend tracking strategy worth recommending. It has clear trading logic, sufficient risk control, and can bring users stable and efficient investment returns.

But the strategy itself also has some inherent weaknesses. It requires users to have the ability to optimize parameters and integrate strategies in order to maximize the effectiveness of this strategy. Overall, the momentum tracking strategy is a quantitative product suitable for quantitative enthusiasts with some foundation.

- 1