Dual Indicator Quantitative Strategy

Overview

This strategy generates trading signals by combining the 123 Reversal indicator and the RAVI indicator. The 123 Reversal belongs to the reversal type strategy, using the price movement in the last two days to determine future price trends. The RAVI indicator determines whether the price has entered the overbought or oversold zone. The strategy decides to go long or short based on the combined signals from both indicators.

Strategy Logic

123 Reversal

This indicator is based on the K value of the Stochastic indicator. Specifically, it goes long when the close price today is lower than the previous two days and the 9-day slow stochastic line is lower than 50. It goes short when the close price today is higher than the previous two days and the 9-day fast stochastic line is higher than 50. So it enters based on reversal points confirmation.

RAVI Indicator

This indicator generates signals by calculating the difference between fast and slow moving averages. Specifically, the difference between 7-day MA and 65-day MA. It goes long when the difference is greater than a threshold and goes short when lower than a threshold. So overbought and oversold areas can be identified when fast and slow MAs crossover.

Strategy Signals

A signal is generated when 123 Reversal and RAVI agree on the direction. The long signal is triggered when both indicators show 1 and the short signal is triggered when both show -1. This dual confirmation avoids wrong signals from a single indicator.

Pros Analysis

- Combining two indicators improves signal accuracy and avoids false signals

- 123 Reversal uses price data and RAVI uses moving average data to determine trends from multiple perspectives

- The parameters of RAVI are adjustable and can be optimized for different products and market environments

- The combination of reversal and trend allows catching both reversals and trends

Risks and Optimization

- Dual indicators combination can sometimes lead to conflicting signals. A price deviation parameter can be introduced to trigger signals when the price deviation between the two indicators is within a threshold

- 123 Reversal is a high frequency strategy. It should be combined with other low frequency strategies to lower trading frequency

- RAVI is good at catching medium to long term trends. Combining with short-term indicators can enhance risk management

Conclusion

The strategy considers both reversal and trend factors. Dual confirmation helps avoid false signals. Next steps could be introducing machine learning algorithms for adaptive parameter optimization. Or combining this strategy with other strategy types to achieve portfolio diversification while maintaining profits and reducing maximum drawdowns.

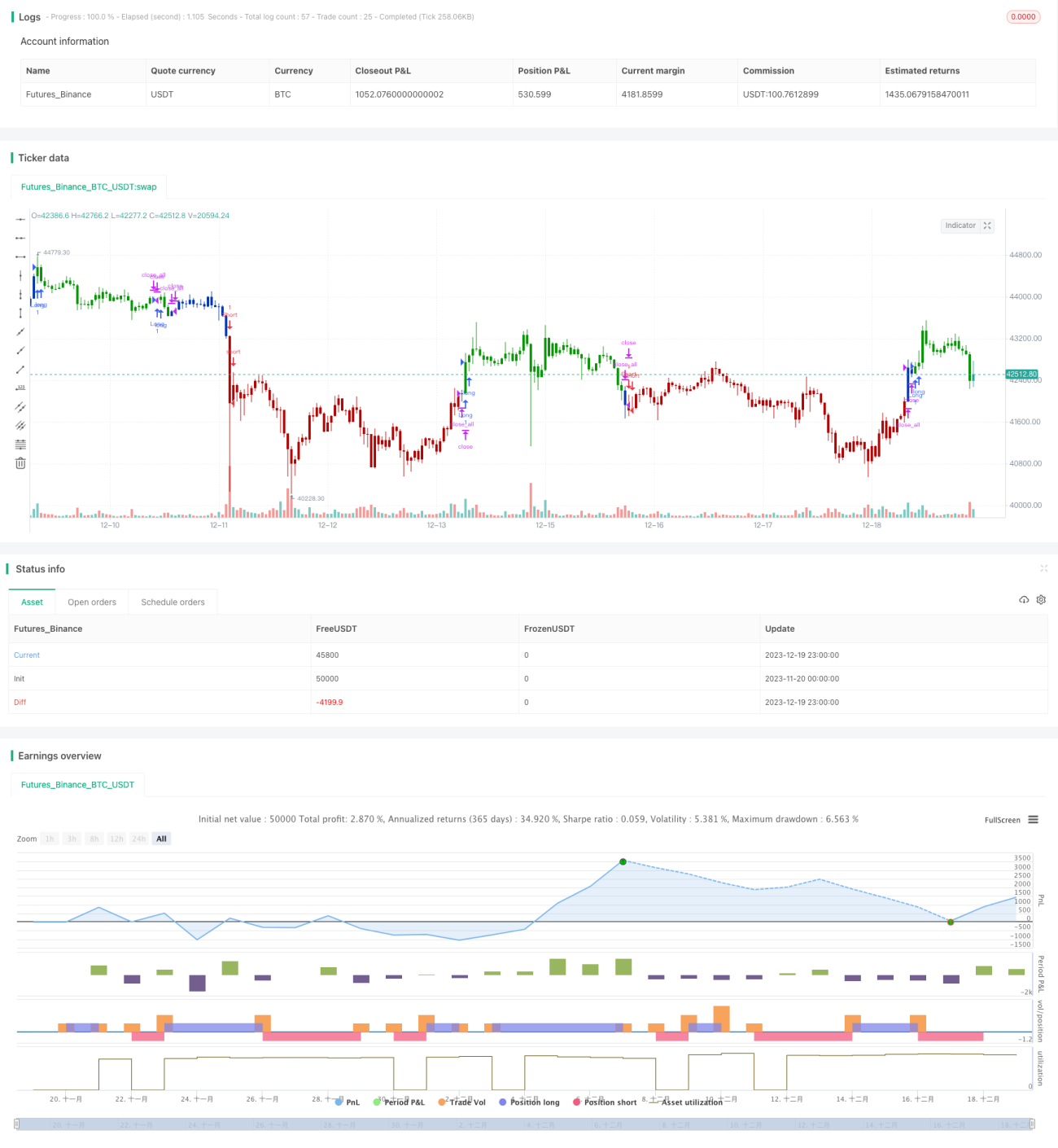

/*backtest

start: 2023-11-20 00:00:00

end: 2023-12-20 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 31/05/2021

// This is combo strategies for get a cumulative signal. - 1