Dual Moving Average Reversal Strategy

Overview

The Dual Moving Average Reversal Strategy is a quantitative trading strategy that utilizes dual moving averages to identify short-term and long-term trends. The strategy combines the 10-day simple moving average (SMA) and the 200-day SMA to capitalize on short-term pullbacks within an underlying long-term uptrend. It also features trend-following and risk management mechanisms.

Strategy Logic

The Dual Moving Average Reversal Strategy is based on the following assumptions:

-

The 200-day SMA identifies the prevailing long-term trend of the market. When the price is above the 200-day line, it signals that the market is in a long-term uptrend.

-

The 10-day SMA pinpoints short-term pullbacks in price. When the price falls below the 10-day line, it indicates a temporary pullback has occurred.

-

In an ongoing bull market uptrend, any short-term pullback can be viewed as a buying opportunity to efficiently catch the upside rebound.

Based on the above assumptions, the trade signals are generated as follows:

-

When the closing price crosses above the 200-day SMA and simultaneously crosses below the 10-day SMA, it triggers a buy signal as it shows the long-term trend remains positive but a short-term pullback has occurred.

-

If the price recrosses above the 10-day SMA when in a long position, the short-term trend has reversed so the position will be closed immediately. Also, if the market falls substantially leading to a stop loss breach, the position will close.

-

Whenever there is a major downturn (exceeding a predefined threshold), it presents an opportunity to buy the dip as a contrarian signal.

With this design, the strategy aims to efficiently capitalize on upside snapbacks during sustained uptrends while controlling risk using stop losses.

Advantages

The Dual Moving Average Reversal Strategy has these key advantages:

- The strategy logic is straightforward and easily understandable.

- The dual moving average filters effectively identify short and long-term trends.

- It offers good time efficiency by capitalizing on short-term reversals.

- The built-in stop loss mechanism tightly controls risk on individual positions.

- Flexible parametrization makes this strategy widely applicable for indexes and stocks.

Risks

While being generally effective, the strategy has these limitations:

- Whipsaws and false signals may occur if the market is range-bound. The strategy should be deactivated during extended consolidations.

- Reliance solely on moving averages has signal accuracy limitations. More indicators could augment performance.

- The fixed stop loss methodology lacks flexibility. Other stop loss techniques could be tested.

- Optimal parameters need to be calibrated for different markets. Suboptimal settings reduce reliability.

Enhancement Opportunities

Further improvements for this strategy include:

- Testing other moving average lengths to find the optimal combination.

- Adding supporting indicators to generate more reliable signals e.g. volume, volatility metrics.

- Exploring other stop loss techniques like trailing stop loss, time-based stop loss.

- Building adaptive capabilities into entry rules and stop loss parameters enabling adjustment to changing market dynamics.

- Incorporating machine learning algorithms to further optimize parameters leveraging more historical data.

Conclusion

In summary, the Dual Moving Average Reversal Strategy is a highly practical approach. It enables profitable pullback fading during sustained uptrends using moving average analysis paired with stop losses. It also offers market regime detection capabilities and risk control. With continual enhancement, the strategy offers strong potential to deliver differentiated performance.

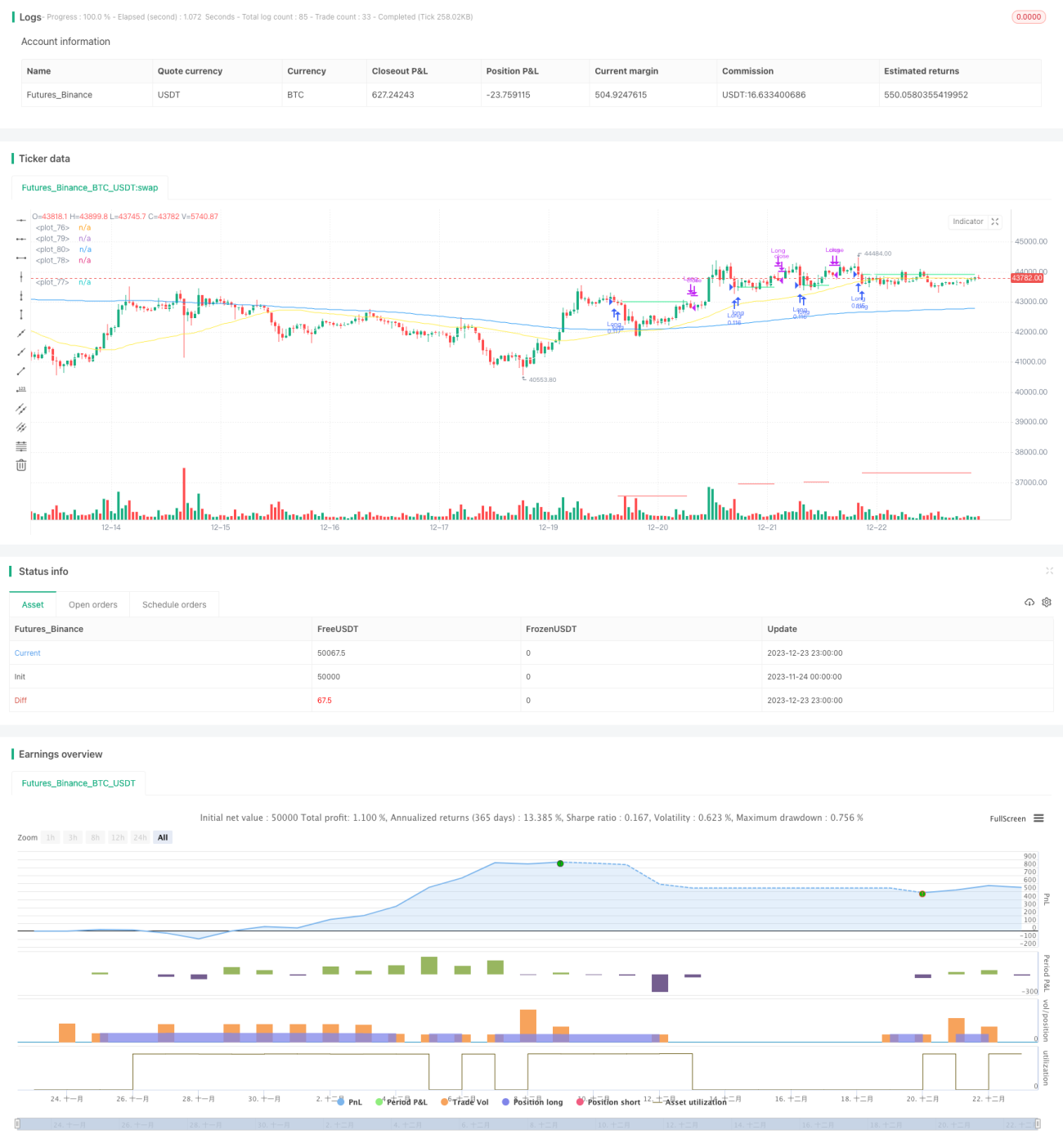

/*backtest

start: 2023-11-24 00:00:00

end: 2023-12-24 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Gold_D_Roger

//note: spreading 1 statement over multiple lines needs 1 apce + 1 tab | multi line function is 1 tab

//Recommended tickers: SPY (D), QQQ (D) and big indexes, AAPL (4H)- 1