Stochastic RSI Momentum Oscillation Trading Strategy

Overview

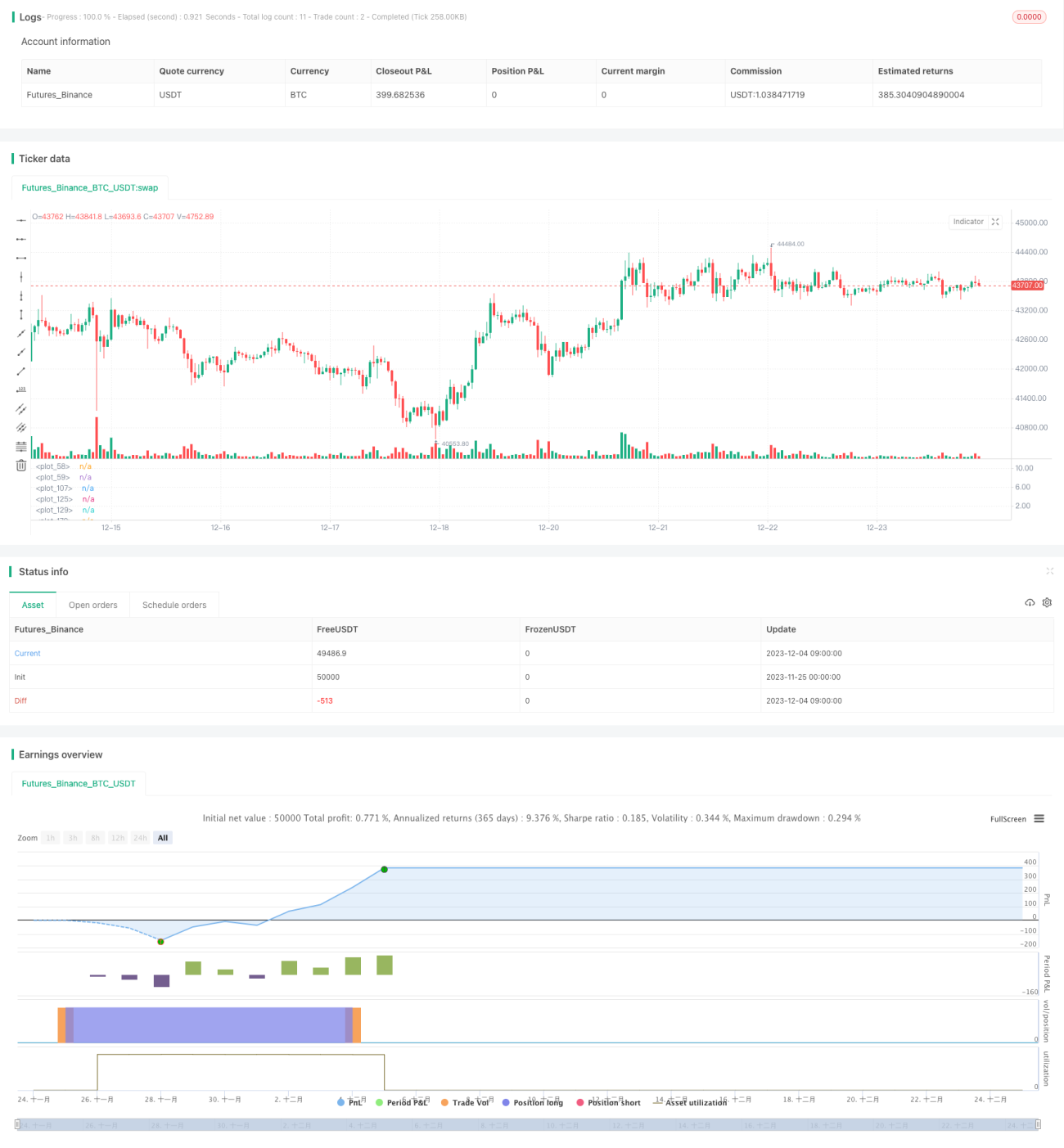

This article mainly explains a momentum oscillation trading strategy based on the Stochastic RSI indicator. The strategy adopts shorter cycle technical indicators (such as 30 minutes) to make trading decisions based on whether the Stochastic RSI enters the overbought/oversold region. Compared with other momentum strategies, this strategy combines the advantages of both RSI and Stochastic indicators to more accurately capture short-term market oscillations.

Strategy Principle

The core indicator of the strategy is Stochastic RSI. The calculation formula of Stochastic RSI is:

Stochastic RSI = (RSI - RSI Low) / (RSI High - RSI Low) * 100

Where RSI is calculated using the lengthRSI parameter (default 12), and Stochastic RSI is calculated using the lengthStoch parameter (default 12).

When Stochastic RSI is higher than the purple filled area, it is the overbought area, then go short; when Stochastic RSI is lower than the purple filled area, it is the oversold area, then go long.

In addition, the strategy also sets the moving average filter condition. Only when the fast EMA is higher than the slow EMA can you open a long position; only when the fast EMA is lower than the slow EMA can you open a short position. This avoids counter-trend trading.

Advantages of the Strategy

Compared with a single RSI strategy, this strategy combines the Stochastic indicator to more clearly identify overbought/oversold areas, thereby improving the reliability of signals.

Compared with a single Stochastic strategy, this strategy uses RSI as the input data source of Stochastic, which can filter out some noise and make the signal more reliable.

The moving average filter condition is set to effectively avoid counter-trend positions building, thereby reducing unnecessary losses.

The position holding time delay is set to avoid being stopped out by false breakouts.

Risks of the Strategy

The strategy mainly uses short-cycle indicators, so it is only suitable for short-term operations and may not perform well in the long run.

The Stochastic RSI indicator itself has a certain lag and may miss signals after drastic price changes in the short term.

In oscillating markets, Stochastic RSI may produce multiple penetrations of overbought/oversold areas, which may lead to overtrading and increased transaction costs.

Optimization Directions

-

Different parameter combinations can be tested to further optimize the length, K and D values of Stochastic RSI.

-

Different RSI length parameters can be tested to find a more appropriate RSI cycle.

-

Try combining with other indicators to further improve signal accuracy, such as MACD, Bollinger Bands, etc.

-

Test different position holding delay parameters to find a more appropriate exit timing.

Conclusion

This article details the construction principles, advantages, risks and optimization ideas of a momentum strategy based on the Stochastic RSI indicator. Compared with single indicator strategies, this strategy utilizes the strengths of both RSI and Stochastic to more clearly and reliably identify short-term overbought/oversold phenomena in the market for reversal trading. Further performance improvements can be expected through parameter optimization and indicator combinations.

/*backtest

start: 2023-11-25 00:00:00

end: 2023-12-25 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Drun30 (Federico Magnani)

//@version=4- 1