Multi-factor Quantitative Trading Strategy

Overview

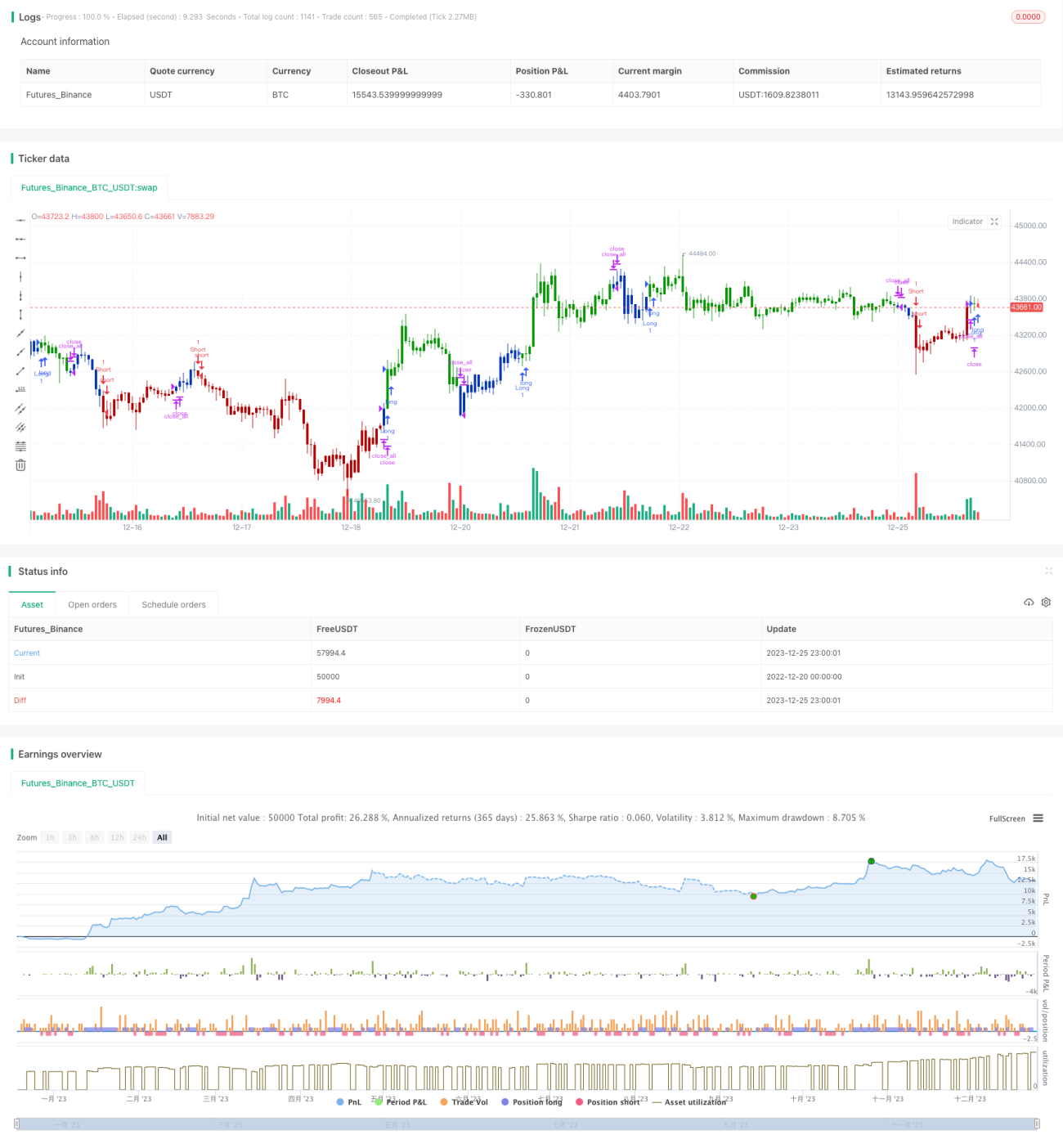

This strategy combines the 123 reversal strategy and psychological line strategy to form a multi-factor quantitative trading strategy. By comprehensively considering technical patterns, market psychology and other factors, the strategy can make more accurate judgments when determining market trends.

Principle

123 Reversal Strategy

The 123 reversal strategy judges that if the closing price of the day rises compared to the previous day, and the slow K line is below 50, go long; if it falls, and the fast K line is above 50, go short. The strategy takes advantage of the characteristics of short-term reversals to profit.

Psychological Line Strategy

The psychological line strategy counts the ratio of rises and falls over a certain cycle. If the rise is greater than 50%, it indicates that bulls control the market; if the rise is less than 50%, it indicates that bears control the market. Make judgments about market psychology based on the ratio of rises and falls.

This strategy combines the signals from the above two strategies. Open positions when the two strategies give signals in the same direction, and close positions when giving signals in different directions.

Advantages

The strategy combines multiple factors and can make more accurate judgments about market trends, avoiding misjudgments caused by a single technical indicator. At the same time, the combination of market psychology makes the strategy more resilient to cope with complex trend changes.

Risks and Solutions

The setting of parameters for each factor in the strategy will have a greater impact on strategy performance. Unreasonable parameter combinations may greatly reduce the effectiveness of the strategy. In addition, drastic changes in trends can also cause the strategy to fail. To reduce risks, we need to backtest various market conditions to find the optimal parameter settings; also control position sizing to ensure that a single loss will not be too large.

Optimization Directions

On the existing basis, we can continue to add other judgment factors such as volatility and volume to form a more three-dimensional strategy logic; or add machine learning algorithms to achieve automatic parameter adaptive optimization. These will be further optimization directions for this strategy.

Summary

This strategy comprehensively considers multiple factors such as technical patterns and market psychology. Validation between different factors ensures the validity of signals. At the same time, it leaves ample room for optimization and is expected to achieve superior performance. This is a high-quality quantitative strategy worth long-term tracking, accumulation and optimization.

/*backtest

start: 2022-12-20 00:00:00

end: 2023-12-26 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 30/04/2021

// This is combo strategies for get a cumulative signal. - 1