Reversal Dual Moving Average Crossover Strategy

Overview: This strategy is based on the classic trading strategy of moving average crossover. It uses dual moving averages, including Simple Moving Average (SMA), Exponential Moving Average (EMA), Variable Weighted Moving Average (VWMA) and Hull Moving Average (HMA).

Principle: The core logic of the strategy is the dual moving average crossover. By calculating two moving averages with different parameters, a buy signal is generated when the fast moving average crosses over the slow one, and a sell signal is generated when the fast moving average crosses below the slow one. The moving average crossover represents the turning point of the short-term and long-term trends of prices.

Advantage Analysis: The main advantages of the dual moving average crossover strategy are simplicity and ease of operation. With only one signal, the most basic trend judgment can be obtained without too many parameter selections and adjustments, which is very suitable for novice traders. In addition, different types of moving averages are tested to optimize different combinations.

Risk Analysis: The main risk of this strategy is that common moving average crossover strategies will have a lot of false signals, resulting in multiple small profits and flat positions, which affects the overall return. In addition, the fixed fast and slow moving average length settings may fail in certain cycles.

Optimization Directions: 1) Test different periods to determine the optimal combination of moving average crosses; 2) Consider introducing a second set of moving average parameters and RSI indicators to assist in judgment to reduce false signals; 3) Introduce condition judgment based on the incremental change of the MA indicator instead of simple crossover to obtain a more reliable crossover judgment.

Summary: This strategy adopts the framework of the traditional moving average crossover strategy to test dual moving averages to find the optimal combination of moving average periods. At the same time, it adds stop-loss judgments based on the ROC and price of the moving average. Overall it is a simple and easy-to-use dual moving average strategy that conforms to quantitative trading logic. In addition, the rich optimization ideas also provide room for the further development of this strategy.

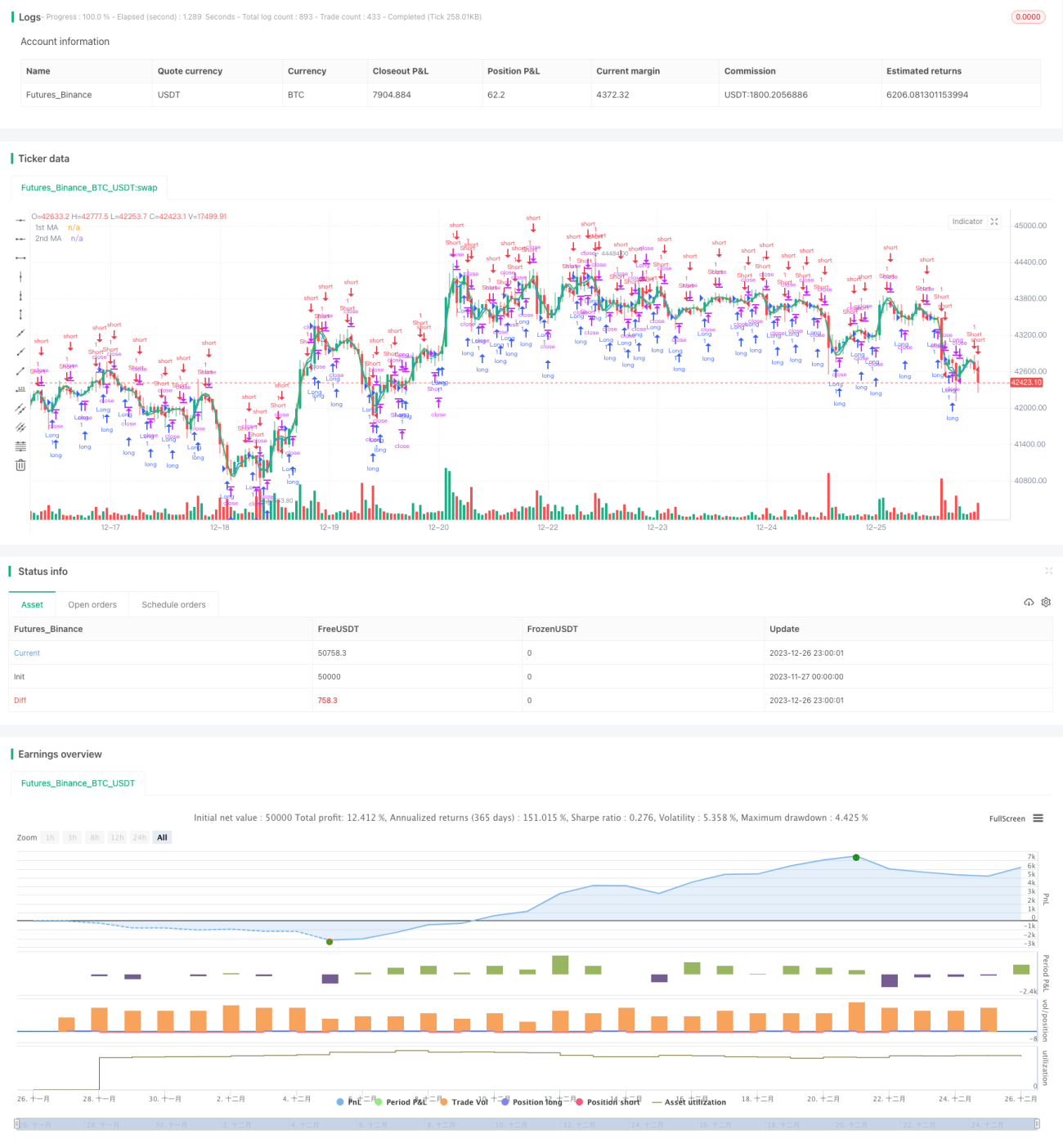

/*backtest

start: 2023-11-27 00:00:00

end: 2023-12-27 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

//study(title="MA Crossover Strategy", overlay = true)

strategy("MA Crossover Strategy with MA Turning Point Exits", overlay=true)

src = input(close, title="Source")- 1