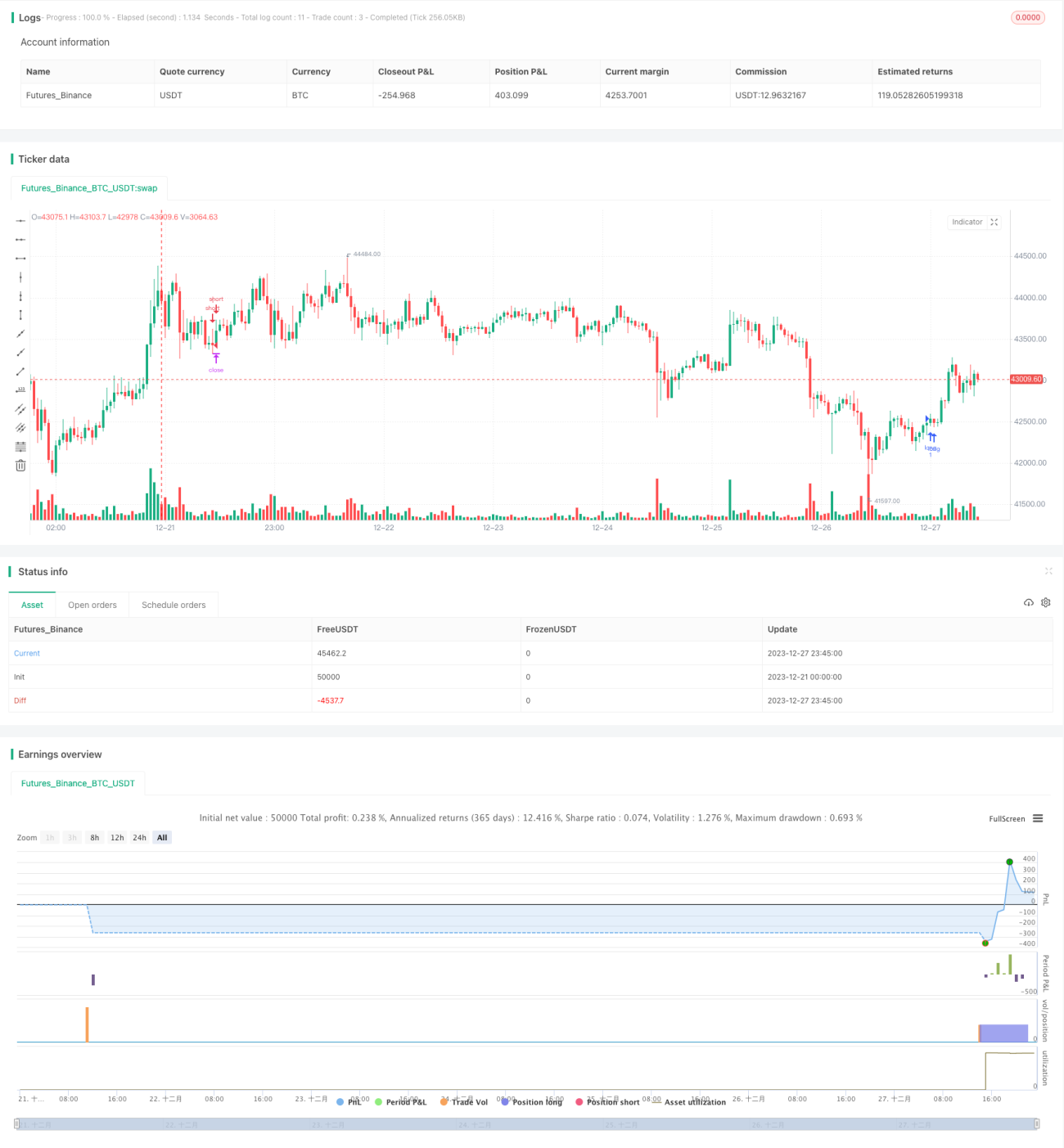

High/Low Cryptocurrency Strategy Based on Multiple Indicators

Overview

This strategy is a high/low level strategy suitable for cryptocurrency markets. It integrates MACD, PSAR, ATR, Elliott Wave and other multiple indicators for trading at higher timeframes like 1 hour, 4 hours or 1 day. The advantage of this strategy lies in the high risk reward ratio with average profit factor ranging from 1.5 to 2.5.

Strategy Logic

The trading signals of this strategy come from the price high/low levels and composite judgments of multiple indicators. The specific logic is:

-

Judge if there is a high/low level range formed by successive higher highs or lower lows on the price chart.

-

Check the histogram level of MACD.

-

Check PSAR indicator for trend direction.

-

Check trend direction based on ATR and MA.

-

Confirm trend direction with Elliott Wave indicator.

If all the 5 conditions point to the same direction, long or short signals are generated.

Advantages

-

High risk reward ratio up to 1:30.

-

High average profit factor, usually between 1.5-2.5.

-

Combination of multiple indicators helps filter false breakouts effectively.

Risks

-

Relatively low win rate around 10%-20%.

-

Potential drawdown and whipsaw risks exist.

-

Indicator performance could be impacted by market regimes.

-

Need decent psychological endurance.

Corresponding Measures:

-

Increase capital to balance the win rate.

-

Set strict stop loss for each trade.

-

Adjust parameters based on different markets.

-

Strengthen psychology and control position sizing.

Optimization Directions

-

Test parameters based on different cryptos and markets.

-

Add stop loss and take profit to optimize money management.

-

Increase win rate with machine learning methods.

-

Add social sentiment filter for trading signals.

-

Consider confirmation across multiple timeframes.

Conclusion

In conclusion, this is an aggressive high risk high return cryptocurrency trading strategy. Its advantage lies in the high risk reward ratio and profit factor. The main risks come from the relatively low win rate which requires strong psychology. The future optimization directions could be parameter tuning, money management, increasing win rate and so on. Overall this strategy has practical value for cryptocurrency traders seeking high profits.

- 1