Hull Filter Moving Average Strategy

Overview

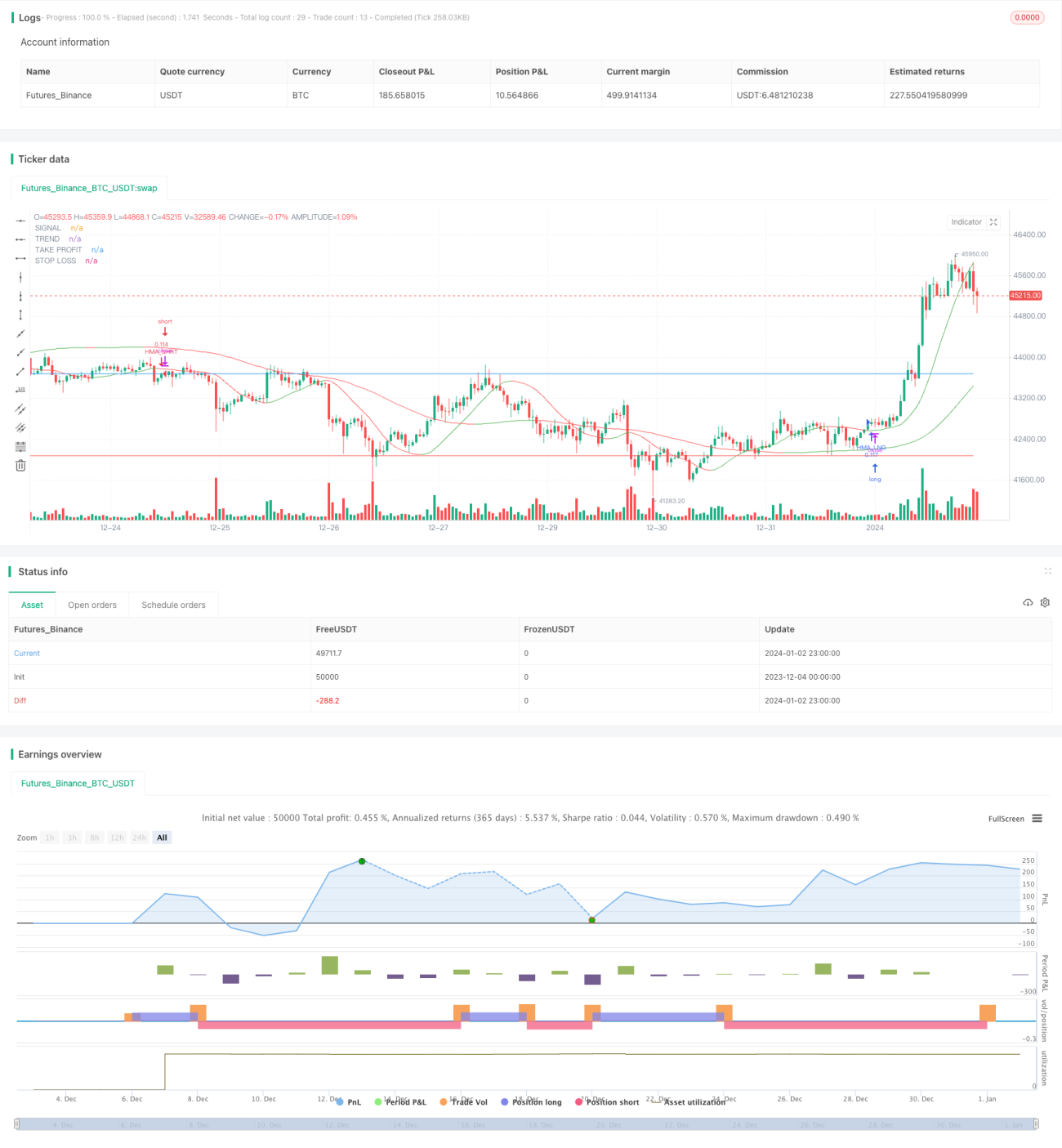

This strategy uses short-term and long-term Hull moving averages to generate and filter trading signals. The short-term Hull moving average is used to generate signals, while the long-term Hull moving average is used for filtering signals. Trades are only taken when the short-term Hull moving average changes direction and the long-term Hull moving average is moving in the same overall direction.

The strategy also uses the ATR indicator to dynamically set stop loss and take profit levels when entering trades.

Strategy Logic

The short-term Hull moving average captures short-term price trends and turning points. When it changes direction, it signals a shift in the short-term price trend.

The long-term Hull moving average determines the overall price trend. For example, when it is rising, prices are in an overall upward trend.

Trades are only taken when the short-term Hull moving average turns direction, and its new direction aligns with the direction of the long-term Hull moving average. This filters out signals that go against the overall trend and may just be short-term market noise.

After entering positions, stop loss and take profit levels are set based on the ATR indicator value. The ATR reflects market volatility and risk levels. The stop loss is placed below price lows while take profit targets price highs, with ranges tied to the current ATR reading.

Advantage Analysis

Combining short-term signals and long-term filters effectively identifies mid-term trends and turning points, avoiding false signals from market noise.

Dynamic stop loss and take profit based on ATR sets reasonable ranges based on current volatility, balancing profit taking and loss prevention.

The Hull moving average has flexibility and accuracy advantages over standard moving averages, with better trend tracking.

Risk Analysis

The strategy relies on crosses between the Hull moving averages to generate signals. False crosses can result in bad trades, requiring analysis of overall market structure.

In ranging, choppy markets with price oscillating in a trading range, signal errors and unnecessary trades may pile up. This can be avoided by filtering signals with wider conditions during such markets.

Stop loss and take profit reliance on ATR means inaccurate volatility reads will result in bad placement. Other volatility measures can augment ATR to correct this.

Optimization

Additional short-term indicators like RSI can improve signal accuracy through convergence.

The filter logic between the Hull moving averages can be enhanced to have more strict entry requirements, avoiding false signals.

Parameter tuning research can uncover stability and profitability improvements from changes to moving average lengths, ATR periods, etc.

Summary

This strategy combines short-term signal generation, long-term signal filtering, and ATR-based stop loss/take profit in a robust mid-term trend following framework. It capably identifies mid-term inflection points while filtering out short-term noise. With parametric optimizations and added filters, it can achieve even better performance.

/*backtest

start: 2023-12-04 00:00:00

end: 2024-01-03 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Hull Filtered Strategy", overlay=true, pyramiding=0, default_qty_type= strategy.percent_of_equity, default_qty_value = 10, calc_on_order_fills=false, slippage=0,commission_type=strategy.commission.percent,commission_value=0)

// Parameters for Hull Moving Averages- 1