Adaptive Botvenko Indicator Long Short Strategy

Overview

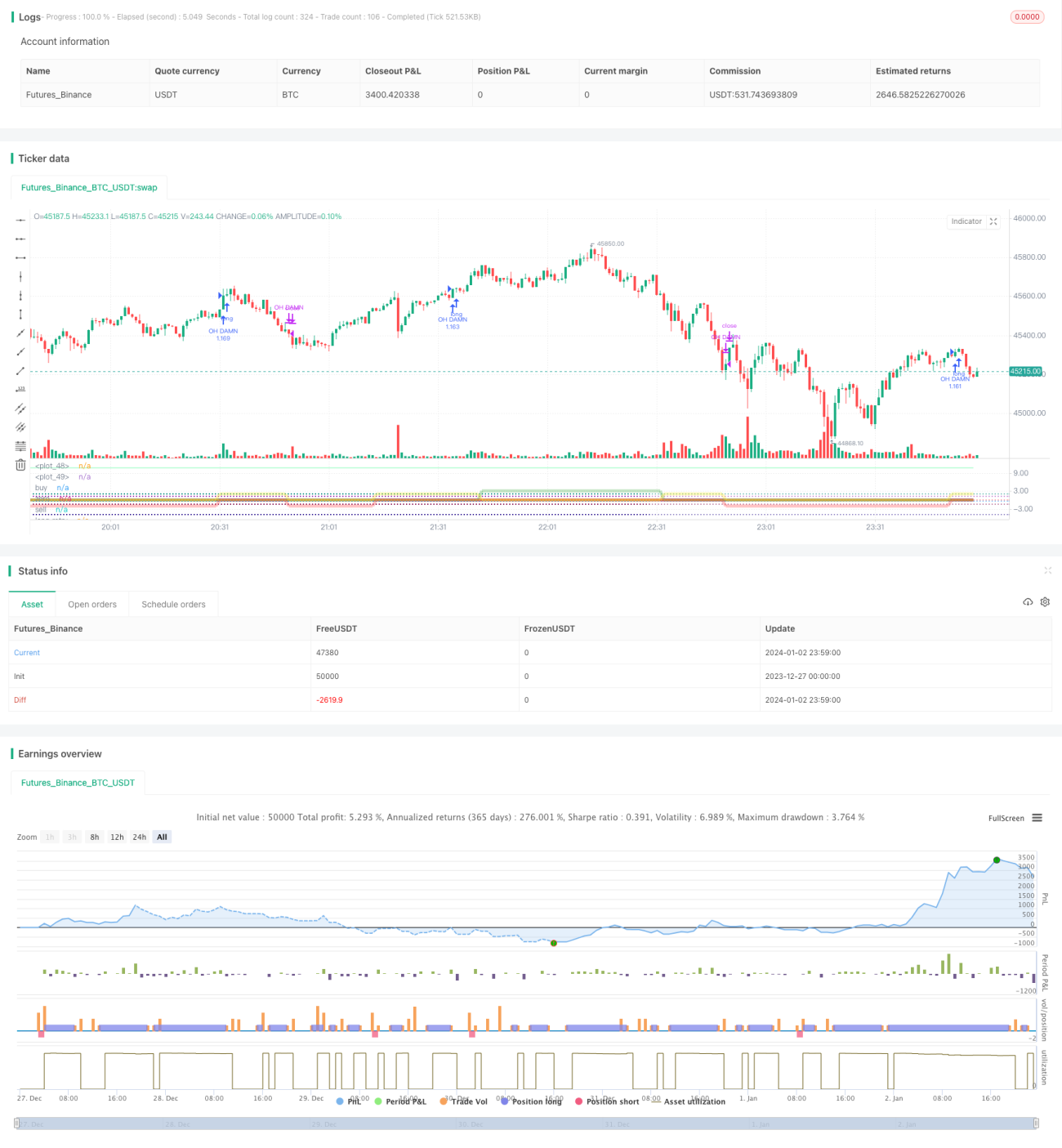

This strategy is developed based on the Botvenko indicator to automatically identify market trends and establish long/short positions. It integrates Botvenko indicator, moving averages and horizontal support lines to automatically recognize breakout signals and establish positions.

Strategy Principle

The core indicator of this strategy is the Botvenko indicator. By calculating the logarithmic difference between closing prices on different trading days, it judges the market trend and important support/resistance levels. It goes long when the indicator crosses above a certain level line and goes short when it crosses below.

In addition, the strategy integrates an "EMA Protection Belt" consisting of 21-day, 55-day and other moving averages. It determines whether the current state is a bull market, bear market or consolidation market based on the sorting relationship of these moving averages, and accordingly restricts short or long operations.

By identifying trading signals with Botvenko indicator and judging market stages with moving averages, inappropriate position establishment can be avoided when used in combination.

Advantage Analysis

The biggest advantage of this strategy is that it can automatically identify the long/short trends of the market. The Botvenko indicator is very sensitive to the difference between prices over two time periods and can quickly locate key support/resistance levels. At the same time, the sorting of moving averages can effectively judge whether it is currently better to be long or short.

This idea of combining fast indicators and trend indicators enables the strategy to quickly locate entry and exit points while preventing inappropriate buying and selling. This is the biggest advantage.

Risk Analysis

The risks of this strategy mainly come from two aspects. First, the Botvenko indicator itself is very sensitive to price changes, which may generate many unnecessary trading signals. Second, the sorting of moving averages can get messy during sideways moves, leading to messy position establishment.

To address the first risk, parameters of the Botvenko indicator can be adjusted to increase the calculation cycle and reduce unnecessary trades. For the second risk, more moving averages can be added to make trend judgement more accurate.

Optimization Directions

The main optimization directions are parameter tuning and adding filter conditions.

For the Botvenko indicator, different period parameters can be tried to find the optimal combination. For moving averages, more of them can be added to form a more complete trend judgment system. In addition, volatility indicators, trading volume indicators etc. can also be introduced to filter out false signals.

Through comprehensive adjustments of parameters and filter conditions, the stability and profitability of the strategy can be further enhanced.

Summary

The adaptive Botvenko long/short strategy successfully combines fast and trend indicators to automatically identify key market points and establish correct positions. Its advantages lie in fast location and prevention of inappropriate positions. Next step is to further improve stability and profitability through parameter and condition optimization.

- 1