Multi-Timeframe Moving Average Crossover Optimization Strategy

1

Follow

1802

Followers

Overview

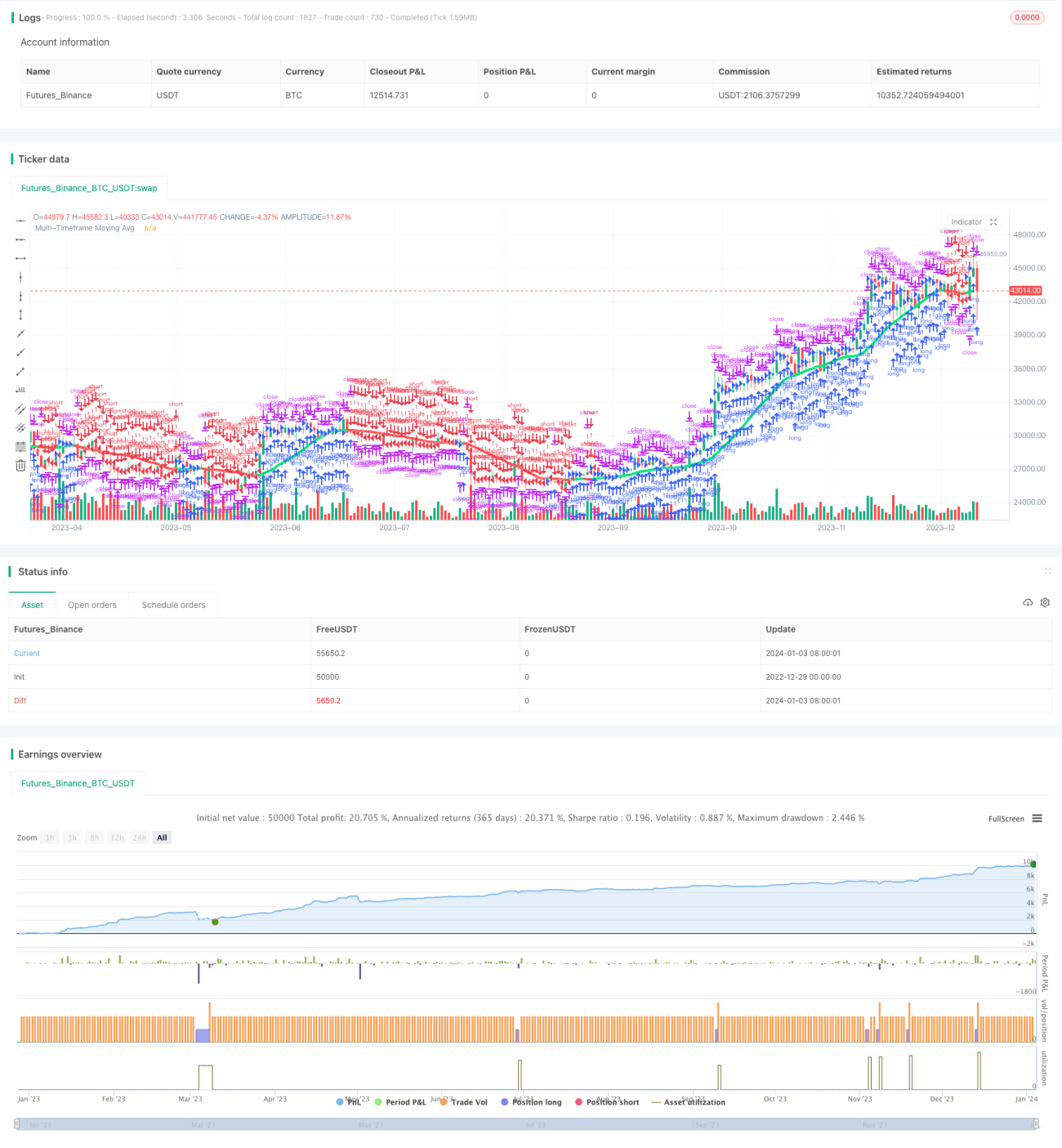

This strategy is based on the famous CM_Ultimate_MA_MTF indicator and rewritten into a trading strategy. It can plot moving averages across multiple timeframes and generate crossover signals between MAs of different periods. The strategy also incorporates a trailing stop loss mechanism.

Strategy Logic

- Plot MA lines of different types on the main chart timeframe and higher timeframes based on user configuration.

- Go long when faster MA crosses above slower MA; go short when faster MA crosses below slower MA.

- Add trailing stop loss to further control risks.

Advantage Analysis

- MA crossovers across timeframes can improve signal quality and reduce false signals.

- Combination of different MA types utilizes strengths of individual indicators for better stability.

- Trailing stop loss helps to limit losses in a timely manner.

Risk Analysis

- Lagging nature of MA may miss short-term opportunities.

- Poor optimization of MA periods may generate excessive false signals.

- Improper stop loss placement may cause unnecessary exit.

Optimization Directions

- Test combinations of MA parameters to find optimum setup.

- Add other indicators for signal filtration and quality improvement.

- Optimize stop loss strategy to suit market profile.

Conclusion

The strategy integrates multi-timeframe analysis and trailing stop approaches of moving averages to improve signal quality and risk control. Further enhancement can be achieved through parameter tuning and adding complementary indicators.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1