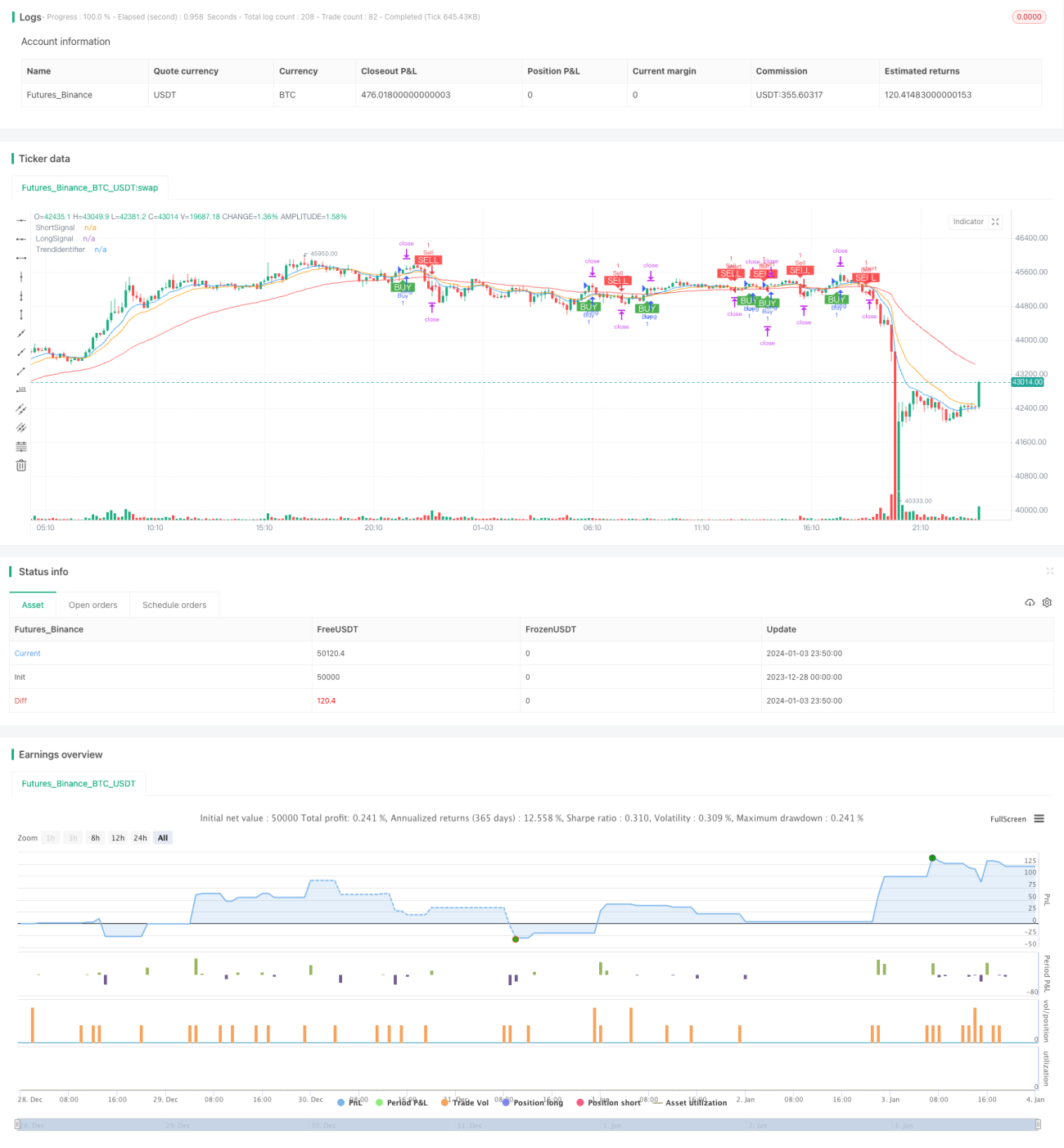

概述

本策略名为“基于EMA均线交叉的短期量化交易策略”。该策略运用9日线、15日线与50日线的EMA均线交叉原理,在1分钟到5分钟的短期时间周期内进行交易,以捕捉短期价格趋势,实现快速进入和退出。

策略原理

该策略使用9日EMA均线、15日EMA均线和50日EMA均线。9日EMA均线和15日EMA均线的交叉用于生成买入和卖出信号。当9日EMA均线上穿15日EMA均线时,产生买入信号;当9日EMA均线下穿15日EMA均线时,产生卖出信号。50日EMA均线用于判断整体趋势方向,只有在价格高于50日EMA均线时才会产生买入信号,只有在价格低于50日EMA均线时才会产生卖出信号。

通过快速EMA均线的交叉以及长期EMA均线的支持,可以捕捉短期价格移动的同时避免逆势操作。 Tak两个短周期均线交叉可确保及时捕捉近期价格变动; 长周期均线可有效过滤震荡局面,避免头痛医头、脚痛医脚。

策略优势

-

捕捉短期价格趋势:通过两个快速EMA均线的交叉,可以快速捕捉短期价格的变动,实现快进快出。

-

过滤震荡:通过长EMA均线判断整体趋势方向,有效防止逆势操作,避免不必要的止损。

-

参数可调:用户可以根据自己的需要调整EMA均线的周期参数,适应不同的市场环境。

-

易于入门:相对简单的均线交叉思路,容易理解使用。

策略风险

-

过于灵敏:两个短周期EMA均线过于灵敏,可能产生大量的错误信号。

-

忽略长期趋势:长EMA均线无法完全过滤震荡,依然存在一定概率的逆势操作风险。

-

参数依赖:优化的参数组合依赖于历史数据,无法保证对未来数据同样适用。

-

止损位置不佳:固定的止损点难以把握,可能过于宽松或过于激进。

策略优化方向

-

加入 stochastic指标 过滤信号,使用KDJ指标的超买超卖信号辅助EMA均线交叉信号。

-

增加自适应止损机制,根据市场波动程度智能调整止损点。

-

增加参数优化模块,通过遗传算法不断迭代寻找最优参数组合。

-

加入机器学习模型判断趋势和信号准确性,提高策略的稳定性。

总结

本策略通过两个快速EMA均线的交叉产生交易信号,并用一个长周期EMA均线判断整体趋势,目标捕捉短期价格移动。这种短线策略易于理解使用,但也存在一定弊端,如产生过多错误信号、忽略长期趋势等。这些问题都需要通过添加辅助指标、自适应机制和参数优化等方式加以改进,使策略在实盘中更稳定可靠。

- 1