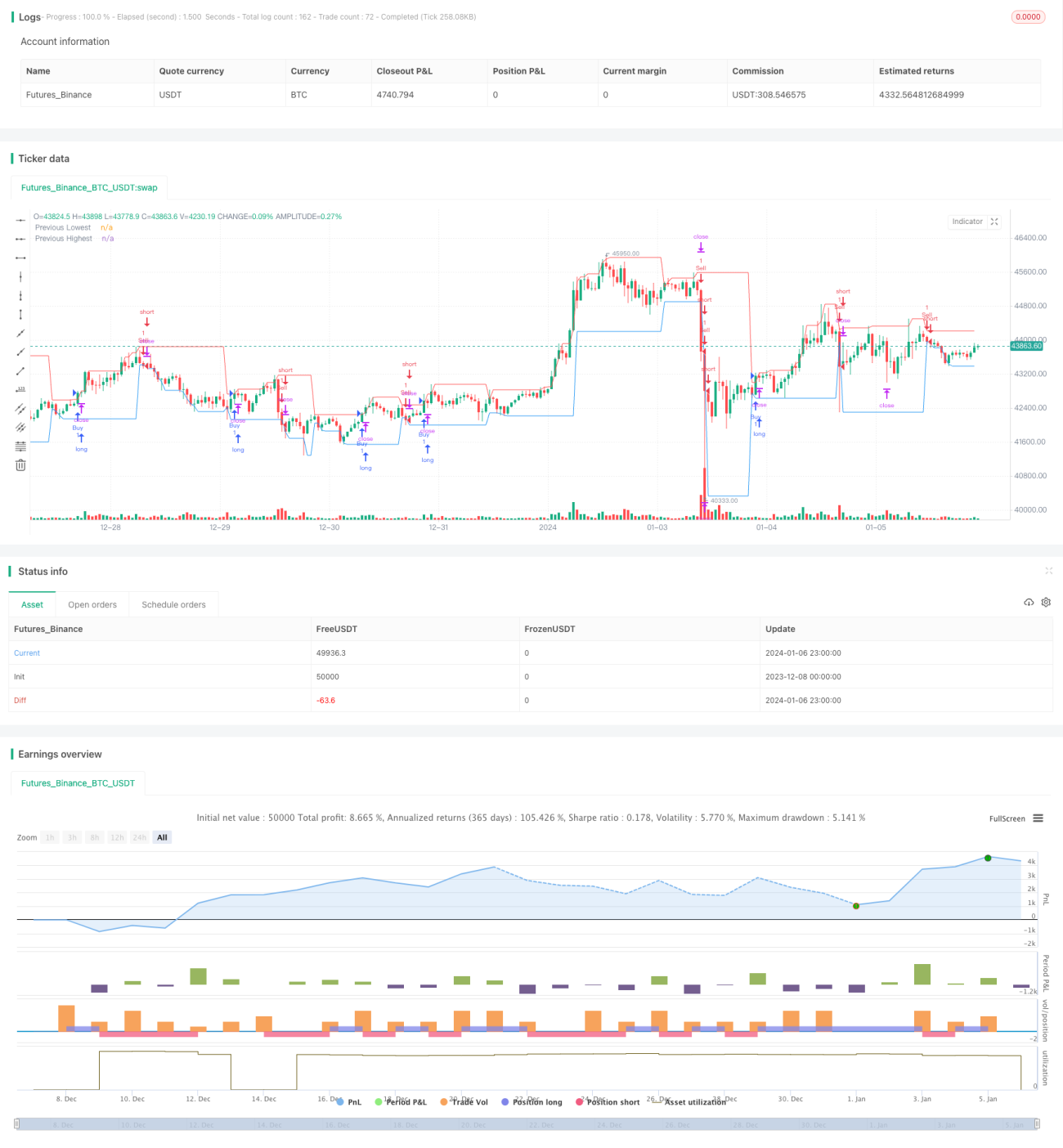

Buy/Sell on Candle Close Strategy

Overview

This strategy triggers buy/sell signals by comparing the closing prices of the current candle and previous candle.

Specifically, if the current candle closes above the highest price of the previous candle, a buy signal is triggered. If the current candle closes below the lowest price of the previous candle, a sell signal is triggered.

Strategy Logic

- Get historical highest and lowest prices of the specified timeframe (e.g. daily, hourly)

- Calculate stop loss and take profit distances

- Stop loss distance = Previous candle highest - Previous candle lowest

- Take profit distance = Stop loss distance * 3 (1:3 risk-reward ratio)

- Determine the relationship between current close and previous high/low

- If current close > previous candle highest, trigger buy signal

- If current close < previous candle lowest, trigger sell signal

- Set stop loss and take profit after entry

- After buying, set stop loss at previous candle lowest - stop loss distance, take profit at previous candle highest + take profit distance

- After selling, set stop loss at previous candle highest + stop loss distance, take profit at previous candle lowest - take profit distance

The above is the basic trading logic of this strategy.

Advantage Analysis

- Simple and clear strategy idea, easy to understand and implement

- Use candlestick information to determine trend direction

- Have stop loss and take profit mechanism to control risk

Risk Analysis

- Judgment based solely on one timeframe may generate more false signals

- Does not consider more factors like volume change, volatility etc.

- Stop loss and take profit settings could be inappropriate, too wide or too tight are both risky

Optimization Directions

- Combine more factors to confirm entry signal, like volume, moving average etc.

- Optimize stop loss and take profit algorithms to have more reasonable stop loss and sufficient take profit

- Parameter tuning may be needed for different products

- Longer timeframe can be tested

Summary

The strategy idea is simple and clear overall, using candlestick closing price to determine trend direction and also has stop loss/take profit to control risk, it can serve as a basic strategy for stocks and crypto trading. But with judgment solely based on one timeframe, it tends to generate false signals more easily. There is still much room for improvement by incorporating more factors and tuning parameters to enhance strategy performance.

- 1