Moving Stop Loss Strategy Based on Points Take Profit and Stop Loss

Overview

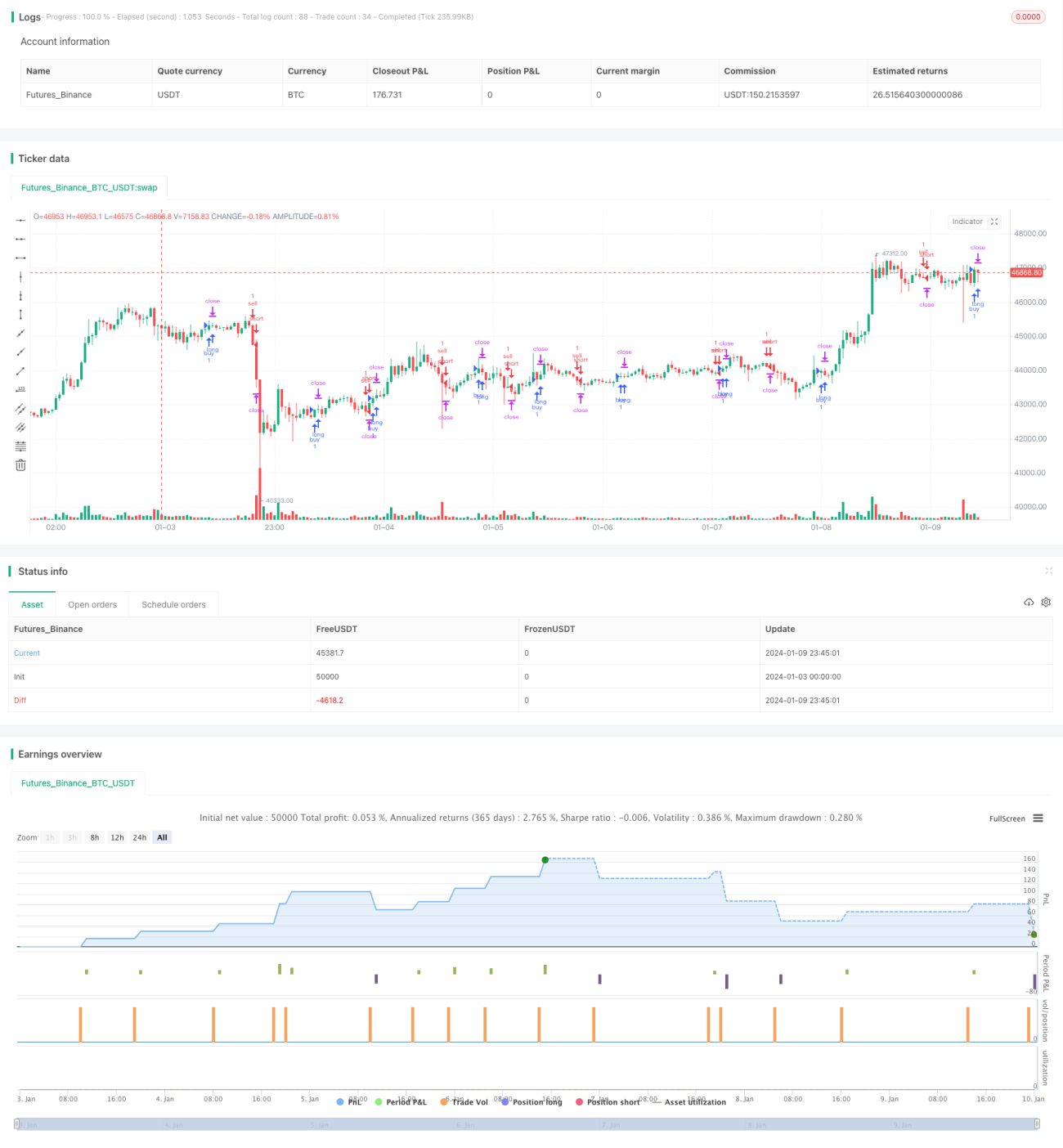

The core idea of this strategy is to use the crossover of EMA and WMA as entry signals, and incorporate take profit and stop loss based on points calculation for trading. Its biggest advantage is that it can very flexibly and precisely control risks by adjusting the number of points to control the amplitude of take profit and stop loss.

Strategy Principle

When EMA crosses WMA upwards, a long signal is generated. When EMA crosses WMA downwards, a short signal is generated. After entering positions, entry price will be calculated in real time, and stop loss and take profit will be set based on that. For example, set stop loss to 20 points and take profit to 100 points, then the specific stop loss price will be entry price minus 20 points * contract value, and take profit price will be entry price plus 100 points * contract value. This is how risk and profit are controlled.

At the same time, the strategy will also combine current market prices with historical stop loss to adjust the moving stop loss position and realize trailing stop loss.

Advantage Analysis

Compared with fixed points or percentage stop loss, the biggest advantage of this strategy is that it can very flexibly and precisely control risks. By adjusting the number of points, the amplitude of stop loss can be directly impacted. This applies very well to different varieties, and parameters can be fine tuned based on market fluctuation frequency and amplitude.

In addition, trailing stop loss is also a very practical function. It can track and adjust stop loss position based on real-time market changes, while ensuring risk control, and maximize possible profits.

Risk Analysis

The main risks of this strategy come from the EMA and WMA indicators themselves. When there is violent market movement, they often give out wrong signals, easily leading to stop loss. In this case, it is recommended to appropriately loosen the number of stop loss points, or consider replacing other indicator combinations.

Another risk point is that it is difficult to balance stop loss and take profit. Pursuing higher take profit often requires undertaking bigger risks, which can easily lead to stop loss when market turns. Therefore, the configuration of stop loss and take profit needs careful testing and evaluation.

Optimization Directions

This strategy can be optimized in the following aspects:

- Test different parameter combinations of EMA and WMA to find the optimal one;

- Try other indicators like MACD, KDJ etc. to replace or combine, and see if win rate can be improved;

- Evaluate risk reward of different points configurations for stop loss and take profit, and find the optimal setting;

- Study characteristics of different varieties, and adjust parameters to adapt to different markets;

- Incorporate machine learning algorithms to realize dynamic optimization of parameters.

Conclusion

The core idea of this strategy is simple and clear, using EMA and WMA as basis, and employing points based stop loss and take profit mechanism for risk control. The advantage of the strategy lies in precise and flexible risk control, which can be adjusted accordingly for different markets. Follow-up optimizations can be done in entry signals, parameter selection, stop loss mechanism etc., to make the strategy adapt better to the complex and ever-changing market environments.

/*backtest

start: 2024-01-03 00:00:00

end: 2024-01-10 00:00:00

period: 45m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// inspiration script from: @ahmad_naquib

// inspiration script link: https://www.tradingview.com/script/tGTV8MkY-Two-Take-Profits-and-Two-Stop-Loss/

// inspiration strategy script name: Two Take Profits and Two Stop Loss

- 1