Quantitative Dual Factor Reversal Inertia Trading Strategy

Overview

The Quantitative Dual Factor Reversal Inertia Trading Strategy is a quantitative trading strategy that combines price reversal signals and market inertia signals. The strategy first uses the Stochastic indicator to generate price reversal signals, then incorporates the market inertia signals from the Relative Volatility Index (RVI), and finally makes trading decisions driven by the dual factors.

Principles

The strategy consists of two main parts:

-

The price reversal part adopts the idea proposed by Ulf Jensen in his book, specifically: when the closing price rises continuously for 2 days and the 9-day Slow Stochastic is below 50, go long; when the closing price falls continuously for 2 days and the 9-day Fast Stochastic is above 50, go short.

-

The market inertia part uses the Relative Volatility Index (RVI). The value of this indicator fluctuates between 0 and 100. Above 50 indicates the long-term trend of the market is upward; below 50 indicates the long-term trend of the market is downward.

In summary, this strategy integrates price reversal signals and market inertia signals to finally determine the current market direction. Trading signals are generated when the signals from both parts align.

Advantage Analysis

The biggest advantage of this strategy is that it combines two major trading ideas – reversal and trend-following. Reversal signals can capture short-term corrections and provide trading opportunities. Inertia signals ensure opening positions only when long-term trends align to effectively filter out noise.

In addition, the dual-factor driven mechanism can improve signal quality. Optimizing the Stochastic parameters and smoothing the RVI also provide room for strategy optimization.

Risk Analysis

The main risks faced by this strategy include:

-

The risk that reversal signals are identified inaccurately. The reasonableness of parameters needs to be verified.

-

The risk that inertia signals generate incorrect signals. The RVI itself has a lag that requires adjusting the smoothing parameter.

-

The risk of missing trading opportunities due to poor alignment of timing of the dual-factor signals. The matching situation under different parameters needs testing.

In addition, reversal strategies face increased loss risks in trending markets. Strictly adhering to stop loss rules is necessary.

Optimization Directions

The strategy can be optimized in the following aspects:

-

Optimize the parameters of the Stochastic indicator to improve quality and timeliness of identifying reversal signals.

-

Optimize the smoothing parameter of the RVI indicator to increase the accuracy of inertia judgment.

-

Test different holding periods to determine the optimal holding cycle.

-

Incorporate stop loss mechanisms. Backtest different stop loss points to find the optimal stop loss position.

-

Consider incorporating other factor signals such as trading volume aberrations to form multi-factor driven strategies.

Summary

The Quantitative Dual Factor Reversal Inertia Trading Strategy comprehensively considers reversal and trend factors, using the Stochastic indicator and RVI indicator to generate trading signals. The strategy has advantages like dual-factor driven, capturing reversal opportunities, and signal filtering. It can be further improved through multi-faceted parameter optimization. Risk control through strict stop loss enforcement is also crucial. The strategy provides good ideas for quantitative trading.

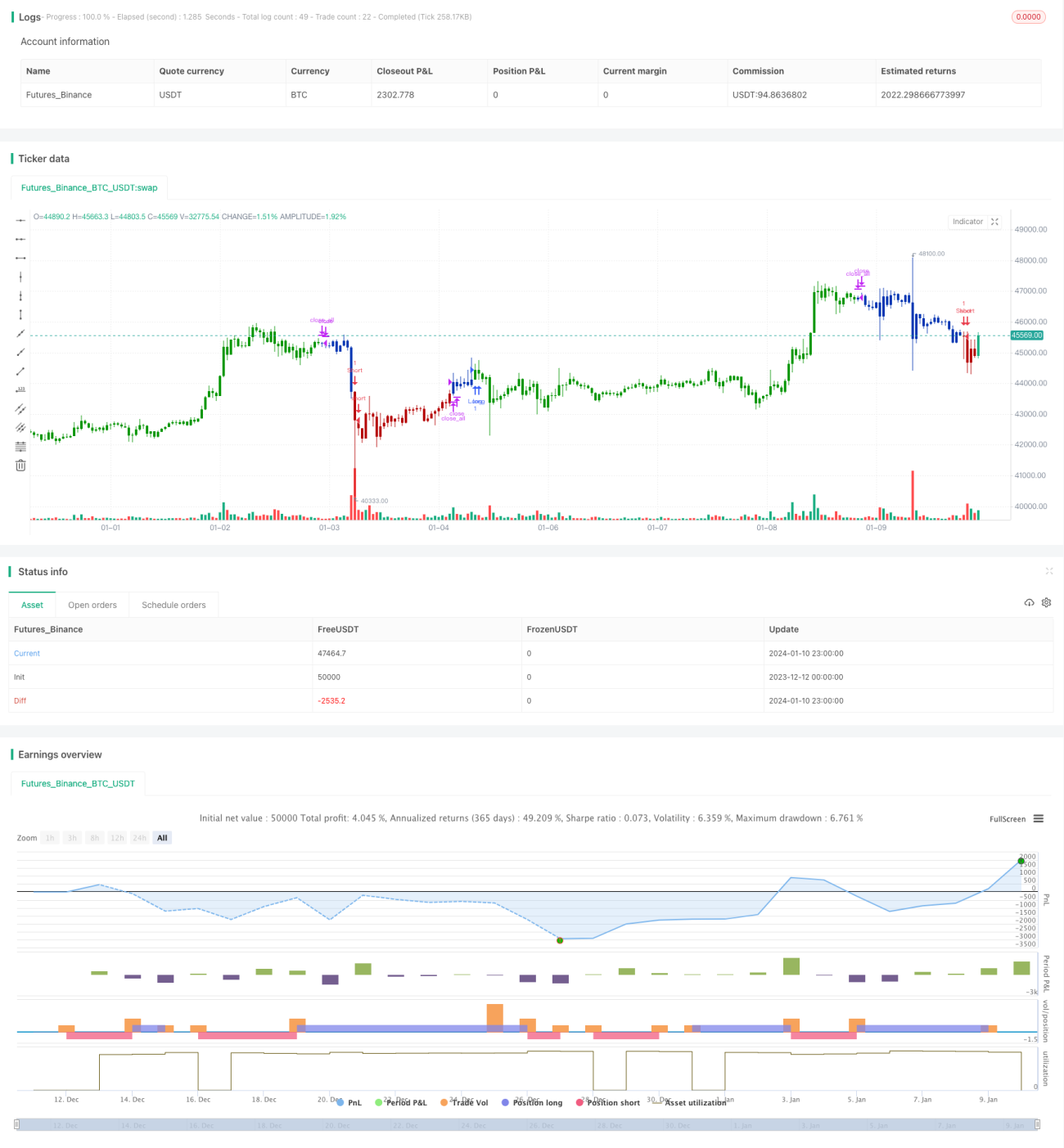

/*backtest

start: 2023-12-12 00:00:00

end: 2024-01-11 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 27/11/2020

// This is combo strategies for get a cumulative signal. - 1