Trend Following Channel Breakout Strategy with Moving Average and Trailing Stop

Overview

This is a breakout strategy based on price Channel, combined with moving average indicators and trailing stop/take profit for entry and exit. It uses moving average of high/low prices to construct the price Channel, and enter long/short when price breaks out of the Channel, with fixed stop loss or trailing stop to control risks.

Strategy Logic

The strategy calculates moving averages of high/low prices to form a price Channel. Specifically, it computes length 10 SMA of high/low prices to plot the upper and lower band of the Channel. When price breaks out above the lower band into the upper band, it enters long. When price breaks down from the upper band into the lower band, it enters short.

After entry, the strategy uses either fixed stop loss or trailing stop for exit. The trailing stop consists of two parameters: fixed take profit level, and activating offset. When price reaches the activating offset, the take profit level starts to trail the price. This allows locking in profits while keeping some open space.

The strategy also combines time range filter, only running backtest within specified historical timeframe, to test performance across different market stages.

Advantage Analysis

The strategy exploits price Channel and trend following with trailing stop, which allows it to capture mid-to-long term trend directions. Compared to simple moving average strategies, it avoids ineffective trades due to price fluctuations. With trailing stops, it can dynamically trail prices to lock in profits.

Overall, the strategy has clear logic, minimal indicators and parameters, easy to backtest, suitable for mid-to-long term trend trading, and can profit from strong trends.

Risk Analysis

The strategy tends to get stopped out easily during ranging, choppy markets, unable to sustain profits. Also during extreme moves, price may break out the stop loss aggressively leading to large losses.

The parameter tuning is quite subjective, requiring adjustments across different market stages. The fixed take profit and activating offset fails to adapt to varying market volatility.

Enhancement Opportunities

Other indicators such as volume, Bollinger Bands can be incorporated to filter entry signals, avoiding traps. Or dynamic stops can be used based on ATR or price volatility.

Exit rules may be upgraded to trailing stop or Chandelier Exit. Partial profit targets can be considered when price re-enters Channel. Optimizing entry filters and exit rules can greatly improve stability of the strategy.

Conclusion

In summary, this is a quantitative strategy based on price Channel, trend following, stop loss/profit taking management. It has clear logic flow, simple parameter structure, easy to understand and backtest. It is suitable to learn algorithmic trading concepts. The strategy can be enhanced in various aspects to improve stability and profitability. The core idea is to capture trend direction, and manage risks via stop loss and take profit. It can be applied to various products over different timeframes.

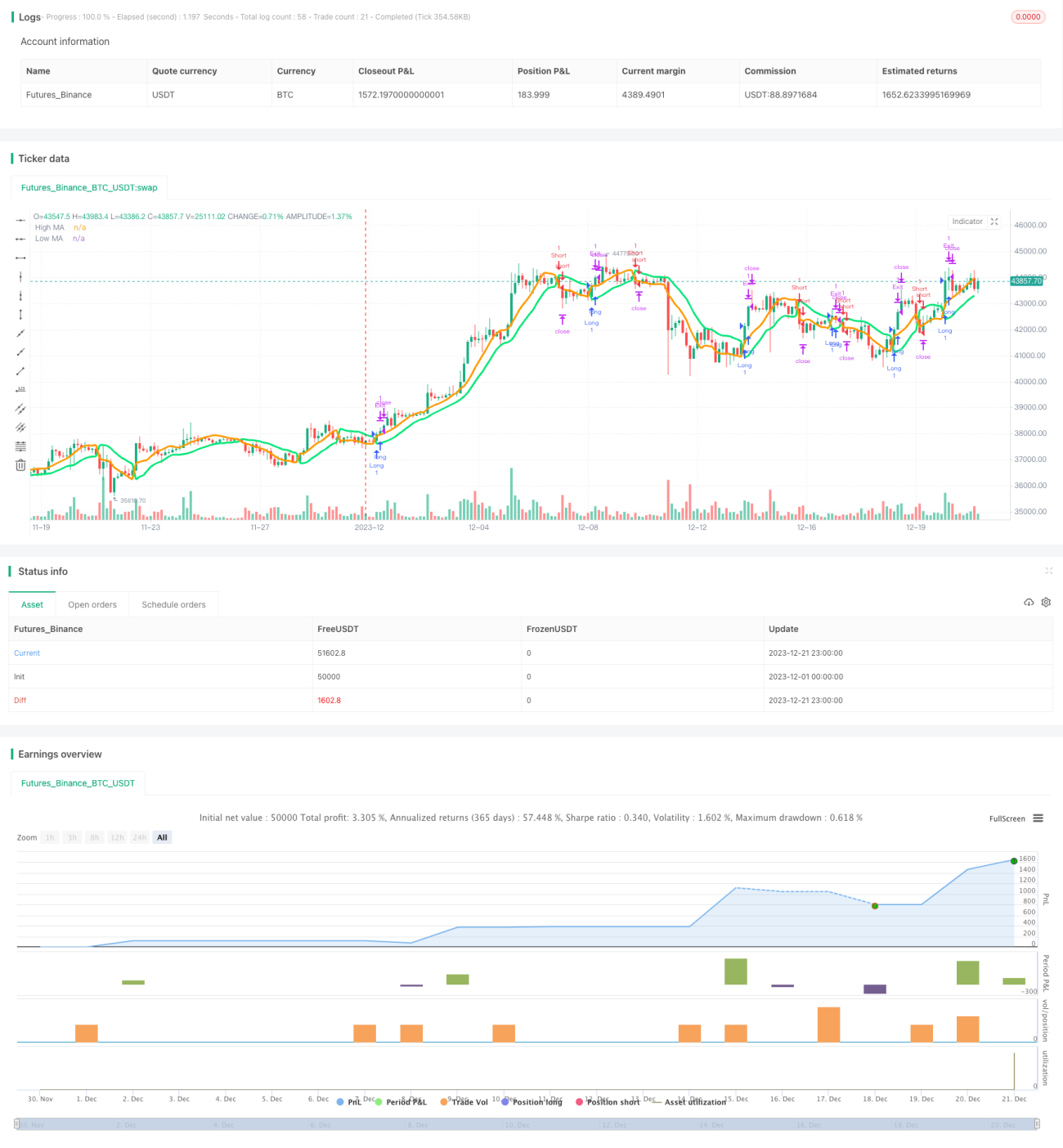

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-21 23:59:59

period: 3h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("Generalized SSL Backtest w/ TSSL", shorttitle="GSSL Backtest", overlay=true )

// Generalized SSL:

// This is the very first time the SSL indicator, whose acronym I ignore, is on Tradingview. - 1