概述

优化EMA黄金交叉策略是一种遵循EMA指标的简单且有效的量化交易策略。它利用不同周期的EMA均线之间的交叉作为买入和卖出信号,并结合风险管理原则进行仓位管理。

策略名称与原理

该策略的名称为优化EMA黄金交叉策略。其中的“优化”二字体现了该策略在基础EMA策略的基础上进行了参数和机制的优化;“EMA”代表其核心指标为指数移动平均线;“黄金交叉”则指其交易信号的产生源自不同EMA均线的黄金交叉。

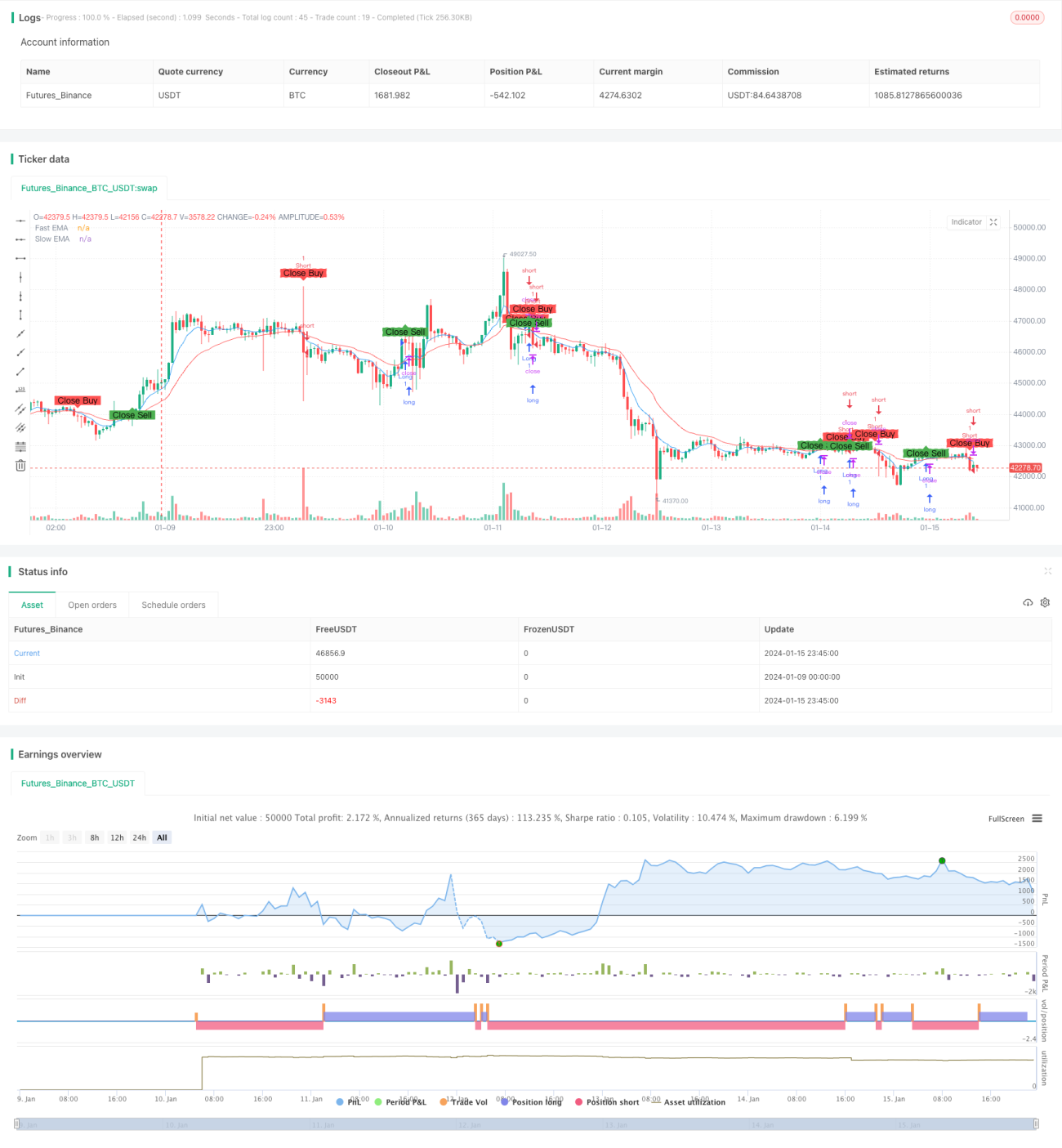

该策略的基本原理是:计算两组不同参数的EMA均线,当较短周期的EMA由下向上突破较长周期的EMA时产生买入信号;而当较短周期的EMA由上向下跌破较长周期的EMA时产生卖出信号。这里选取7周期和20周期EMA进行组合,形成快线和慢线。

代码中通过fastEMA = ema(close, fastLength)和slowEMA = ema(close, slowLength)来计算并绘制7日EMA和20日EMA。当快线上穿慢线时,即crossover(fastEMA, slowEMA)条件成立时产生买入信号;当快线下破慢线时,即crossunder(fastEMA, slowEMA)条件成立时产生卖出信号。

策略优势分析

优化EMA黄金交叉策略具有以下几点优势:

-

操作简单。仅基于EMA均线的黄金交叉形成交易信号,容易理解和实现,适合量化交易的自动化。

-

反转捕捉能力强。EMA作为一种趋势跟踪指标,当短期和长期EMA产生交叉时,常常意味着短期趋势和长期趋势的反转,这为捕捉反转提供了时机。

-

平滑去噪效果好。EMA本身具有平滑去噪的特性,有助滤除短期市场噪音,产生高质量交易信号。

-

参数优化设计。FAST EMA和SLOW EMA的周期经过优化选择,在捕捉反转和滤波噪音之间取得平衡,从而产生稳定信号。

-

仓位管理科学。根据ATR和风险回报比优化仓位管理,有效控制单笔交易风险,确保强劲资金管理。

策略风险分析

优化EMA黄金交叉策略也存在一些风险,主要体现在:

-

不适合趋势性市场。EMA交叉对趋势性较强的市场适应性较差,可能产生过多无效信号。

-

参数敏感性较高。FAST EMA和SLOW EMA的选择对策略效果影响显著,需要仔细测试优化。

-

信号延迟问题。EMA交叉信号本身存在一定滞后,可能错过最佳入场时点。

-

止损风险。现有代码中还未引入止损机制,存在较大回撤风险。

对应的解决方案是:

-

采用多因子模型,引入其它指标判断趋势;

-

充分回测寻找最优参数组合;

-

结合其它先行指标。如增量指标MACD的零轴交叉;

-

制定合理的止损策略。如ATR倍数止损或收市止损。

策略优化方向

优化EMA黄金交叉策略的优化方向主要集中在以下几个方面:

-

多市场适应性优化。引入市场状态判断,在趋势行情中关闭策略,减少无效信号。

-

参数寻优。通过遗传算法等寻找最优的参数组合,提高策略稳定性。

-

止损机制引入。设置合理的止损规则。如采用ATR动态止损、移动止损或收市止损。

-

回测周期优化。解析不同时间级别的数据,确定最优的策略执行周期。

-

仓位管理优化。优化仓位算法,在风险与收益之间寻找最佳平衡。

这些优化举措将有助于减少不必要信号,控制回撤风险,提高策略的稳定性和收益率。

总结

优化EMA黄金交叉策略是一个简单高效的量化策略。它利用EMA的优良特性形成交易信号,并在此基础上进行优化设计。该策略具有操作简便、反转捕捉能力强、参数优化、科学的仓位管理等优势;同时也存在一定的市场适应性风险和信号质量风险。未来的优化空间在于提升策略的稳定性和多市场适应性。通过不断优化实践,该策略有望成为可靠的量化解决方案。

/*backtest

start: 2024-01-09 00:00:00

end: 2024-01-16 00:00:00

period: 45m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © mayurtale972

//@version=4

strategy("Optimized EMA Crossover Strategy - 15-Min", overlay=true, shorttitle="EMA15")- 1