Bottom Fishing Strategy

Overview

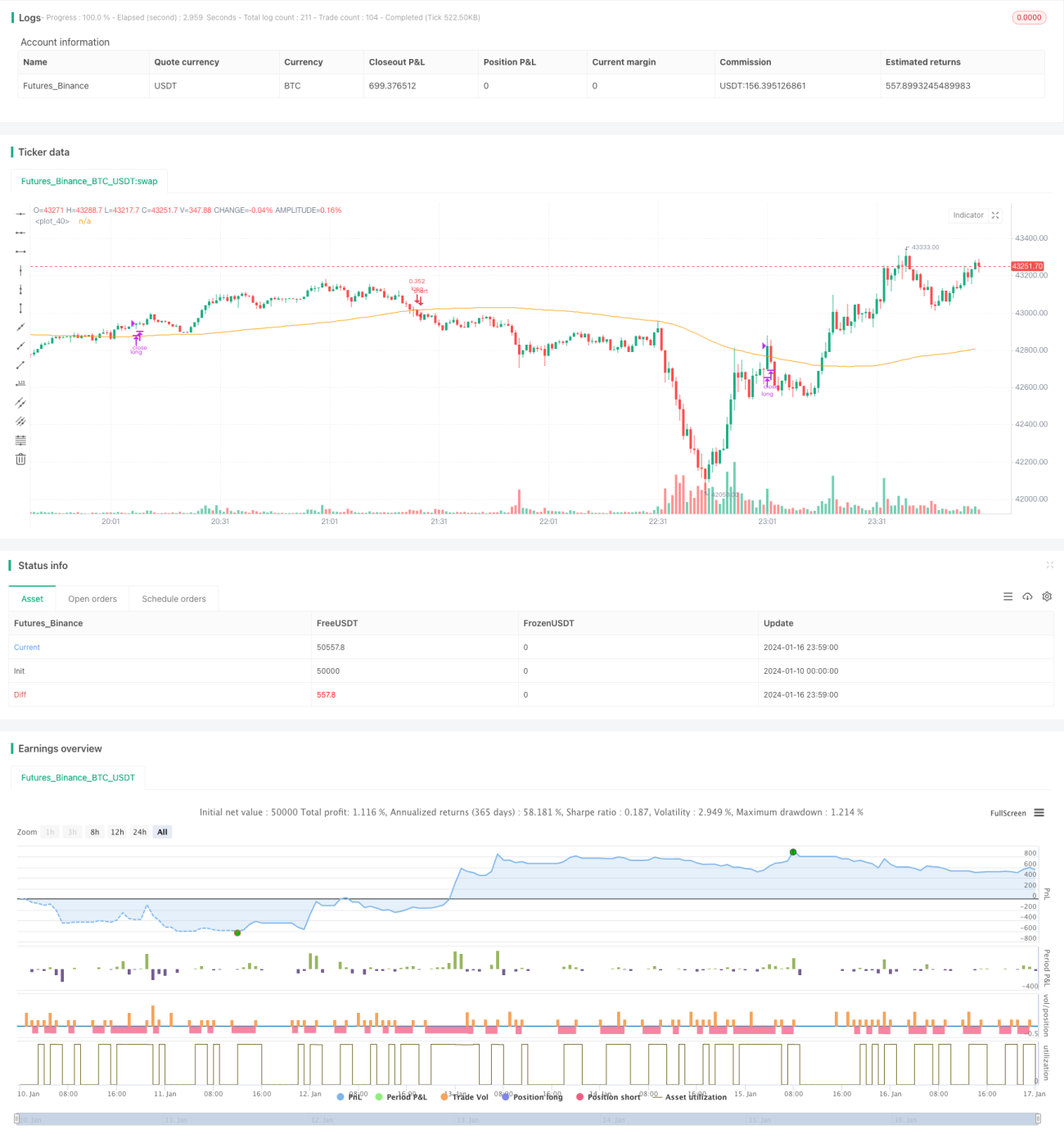

The bottom fishing strategy is a typical low buying and high selling strategy. It utilizes the RSI indicator to identify oversold points and issues a buy signal when the price drops to a certain extent, in order to accumulate tokens at a lower price. When the price rebounds, it realizes profits by setting the RSI exit threshold. This strategy is suitable for medium and long term holding. It can effectively filter out false breakouts in volatile markets and optimize the cost basis of holdings.

Strategy Logic

This strategy mainly relies on the RSI indicator to identify oversold conditions. The normal range of the RSI indicator is from 0 to 100. When the RSI indicator falls below the set entry threshold of 35, a buy signal is issued. When the RSI indicator rises back above the set exit threshold of 65, a sell signal is issued. This allows timely entry and exit at trend reversal points to implement low buying and high selling.

In addition, a 100-period simple moving average is also introduced in the strategy to form a combined condition with the RSI indicator. Only when the price drops below the moving average while the RSI enters the oversold zone will the buy signal be triggered. This can help filter out false breakouts to some extent and reduce unnecessary trades.

Advantages of the Strategy

-

Effectively identify oversold and overbought points with RSI for entry at reversal points, obtaining better cost basis

-

Filter out false signals by combining with moving average, avoiding buying at the peak

-

Suitable for medium to long term holding, able to discover potential uptrends

Risks and Solutions

-

There is a certain lag, possibly missing out fast reversal opportunities

- Shorten RSI calculation period appropriately to speed up indicator reaction

-

More break-even or losing closes may occur in ranging markets

- Adjust moving average period or remove moving average

- Relax RSI entry and exit parameters appropriately

Optimization Directions

-

Test parameters optimization on different coins and time frames

-

Try combining other indicators such as MACD, Bollinger Bands etc.

-

Dynamically adjust RSI parameters or moving average parameters

-

Optimize position sizing strategies

Summary

The bottom fishing strategy is an overall robust and practical low buying and high selling strategy. By double filtering with RSI and moving average, it can effectively curb false signals and obtain lower cost basis with optimized parameters. At the same time, appropriately optimizing indicator parameters and adjusting position strategies may lead to higher capital usage efficiency.

- 1