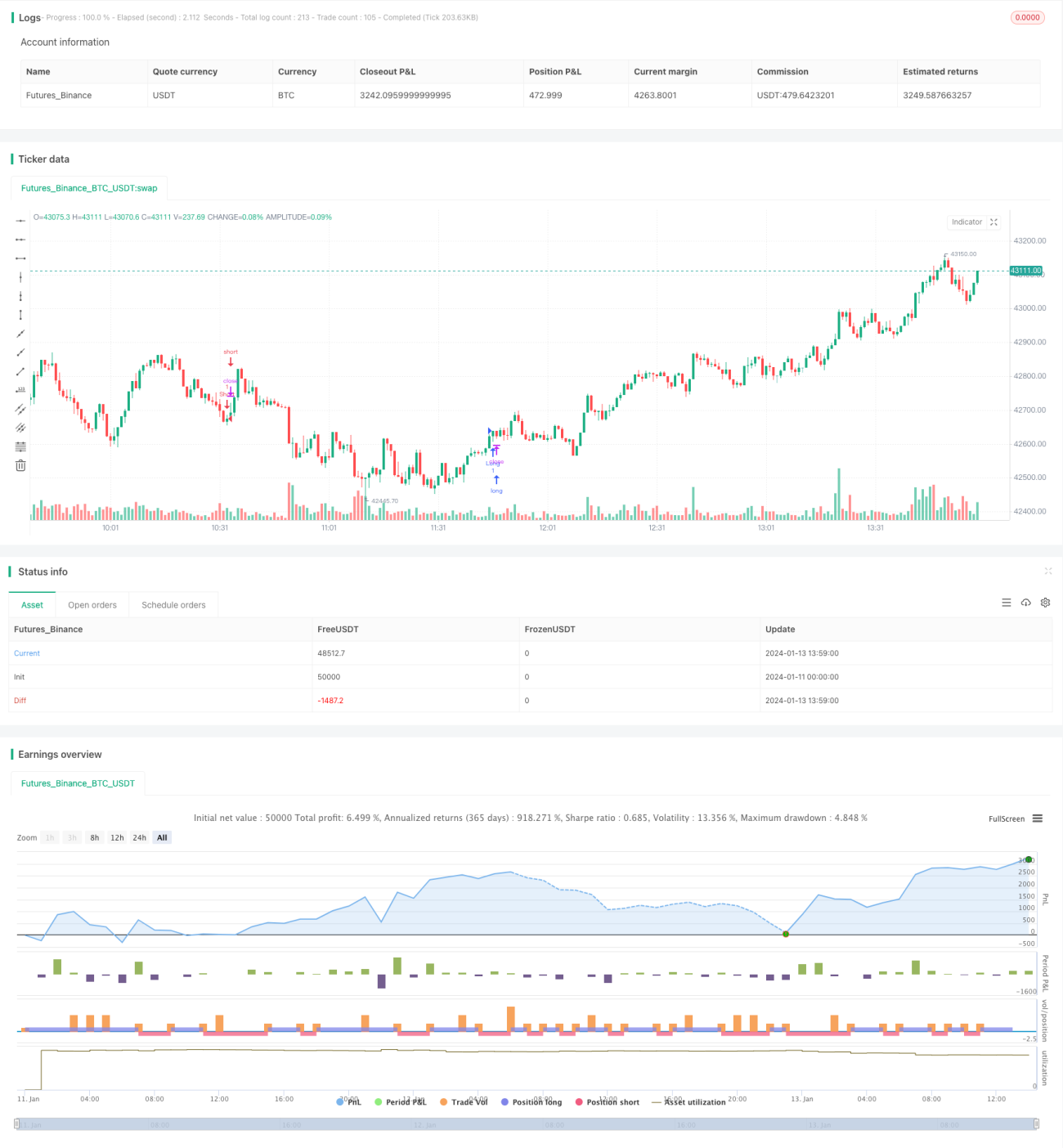

A Trend Strategy Optimization Based On Ichimoku Cloud Chart

Overview

This strategy combines Ichimoku cloud chart with various auxiliary indicators to track the trends. It mainly uses Ichimoku cloud to determine the trend direction and MACD, CMF, TSI and other indicators for filtering to improve the signal quality. This is a strong trend strategy based on comprehensive judgments of multiple factors.

Principles

This strategy mainly utilizes the transformation of Ichimoku cloud to judge the trend direction. It goes long when the Tenkan-sen crosses above the cloud and goes short when the Tenkan-sen crosses below. Meanwhile, it uses Chikou Span, MACD histogram, CMF and TSI for multi-layer filtering to ensure the signal quality.

Specifically, the long signal is triggered when:

- Tenkan-sen crosses above the cloud

- The cloud is wide and Tenkan-sen is above Kijun-sen

- Chikou Span is above the 0-line

- The closing price is above the cloud

- MACD histogram is above 0

- CMF is greater than 0.1

- TSI is above 0

The short signal is triggered when the above conditions are reversed. By such comprehensive criteria, most of the false signals can be filtered out and the major trends in the market are captured.

Advantages

The biggest advantage of this strategy is filtering out false signals and catching strong trends by combining multiple indicators. Specifically:

- Ichimoku cloud determines the major trend direction

- Auxiliary indicators further filter out signals and reduce risks

- Comprehensively considers multiple timeframes for more reliable signals

- Strict rules to trade only high quality setups and avoid choppy markets

- Trend following mechanism to maximize trend profits

Through such judgments, the strategy can effectively identify the mid-long term hot sectors and profit from trend trading.

Risks

The main risks of this strategy include:

- False breakout risk causing wrong signals

- Trend reversal risk leading to the loss of all profits

- Relatively low trading frequency missing opportunities

Solutions:

- Relax filtering criteria properly to increase trade frequency

- Add stop loss condition to limit loss size

- Optimize parameters to improve signal accuracy

Enhancement

The main optimization directions:

-

Parameter optimization through more backtests to find better parameter combination

-

Add stop loss mechanism to control risks

-

Add trailing stop loss to lock in profits

-

Test more indicators to find better filter combination

-

Add rules to distinguish real breakout

Conclusion

This strategy effectively combines Ichimoku cloud and multiple auxiliary indicators. Further improvements on parameter optimization, stop loss mechanism, indicator selection can enhance the stability and signal quality for higher steady returns. The strategy has strong practical value.

- 1