Trend Following Strategy Based on Moving Average

Overview

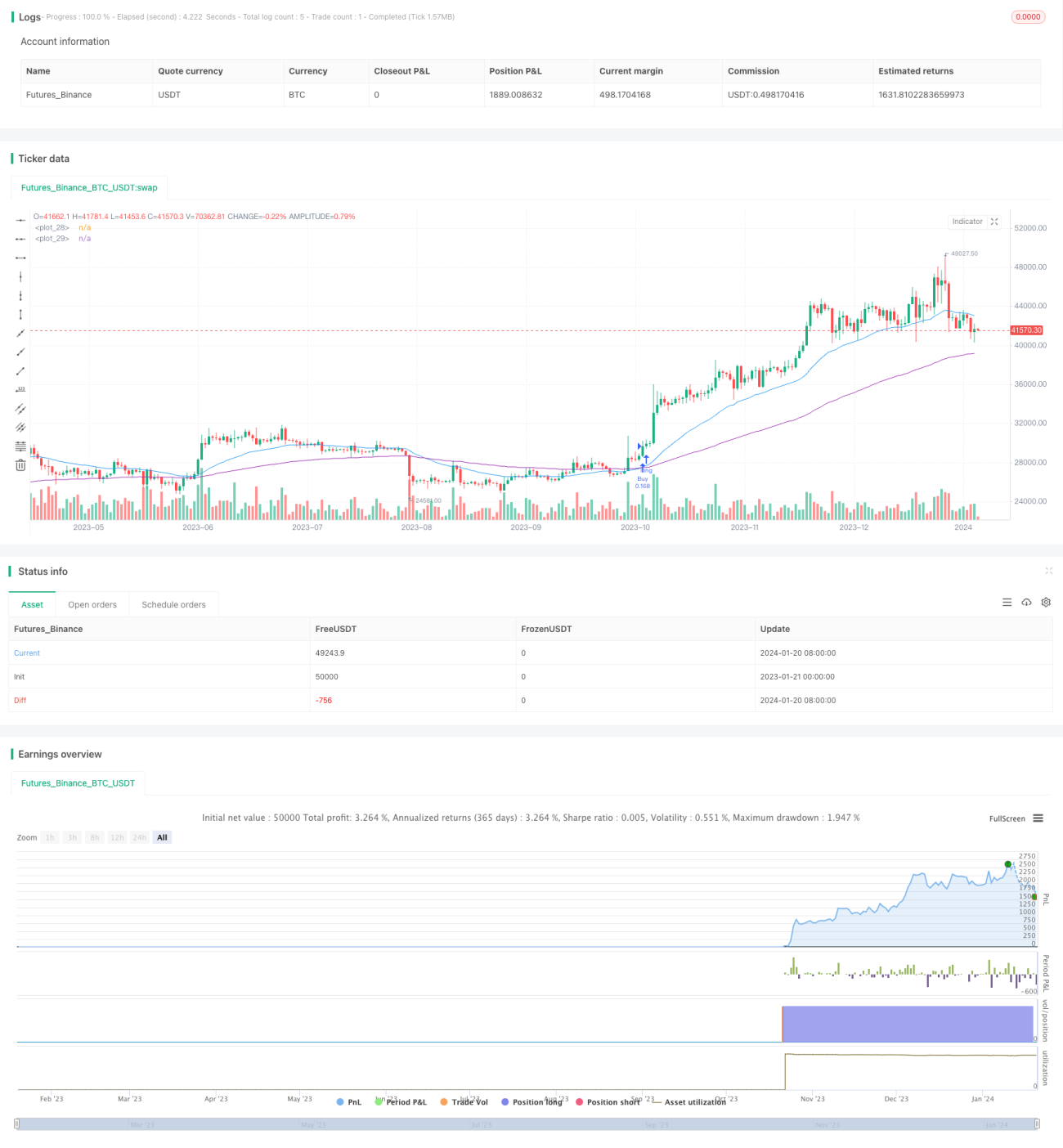

This strategy uses fast and slow moving averages to identify and follow trends. It generates buy signals when the fast line crosses over the slow line and sell signals when the fast line crosses below the slow line. This strategy is suitable for tracking medium- and long-term trends and filtering out market noise effectively.

Strategy Logic

This strategy utilizes two Exponential Moving Averages (EMAs) with different periods as the basis for trade decisions. The fast EMA has a period set to 30 to capture short-term price fluctuations. The slow EMA has a period set to 100 to gauge the direction of the mid- to long-term trend.

When the fast EMA crosses the slow EMA from below, it indicates the market is entering an upward trend and generates a buy signal. When the fast EMA crosses below the slow EMA from above, it flags the start of a downward trend and produces a sell signal.

Advantage Analysis

The advantages of this strategy include:

- Uses moving averages as the basis to filter out short-term market noise and follow trends.

- Adopts a dual-EMA approach to clearly determine trend directionality.

- Allows parameter optimization where fast and slow EMA periods can be customized.

- Capable of tracking mid- to long-term trends and short-term adjustments.

- Simple and clear logic, easy to understand and implement, suitable for beginners.

Risk Analysis

Some risks also exist:

- Prone to false signals when prices move sideways. Can be mitigated by EMA parameter tuning.

- Ineffective in dealing with extreme price swings. Can set stop loss to control risk.

- Lagging inherent in MA systems, may miss price reversal points. Can optimize with other indicators.

Optimization Directions

Some optimization directions:

- Optimize EMA periods to improve profitability.

- Add other indicators like trading volume to avoid false breakouts.

- Add stop loss strategies to limit downside on single trades.

- Incorporate trend strength indicators to avoid trend reversal whipsaws.

- Introduce parameter optimization for wider adaptability.

Conclusion

This strategy builds a trading system based on double EMA crossovers, using fast and slow EMA relationships to determine market trend. Signal generation is simple and clear. It filters some noise and goes along with trends, suitable for medium- to long-term trend trading. There is room for improving universality and efficiency via multi-indicator optimization and risk control.

/*backtest

start: 2023-01-21 00:00:00

end: 2024-01-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy("EMA Strategy v2", shorttitle = "EMA Strategy v2", overlay=true, pyramiding = 3,default_qty_type = strategy.percent_of_equity, default_qty_value = 10)

- 1