Dual-direction Trend Tracking Renko Trading Strategy

Overview

This strategy is a dual-direction trend tracking Renko trading strategy based on the improved Supertrend indicator. The strategy mainly tracks price trends and generates trading signals at trend reversal points, adopting a trend tracking trading approach.

Strategy Logic

The core indicator of this strategy is the improved Supertrend. Supertrend is a technical indicator that tracks price trends. This strategy modifies it in two main aspects:

-

Add a Factor parameter to adjust the sensitivity of Supertrend to control the trading frequency.

-

Add a Trend variable that changes its value when the price breaks through the upper or lower rail, generating trading signals.

When Trend is 1, it indicates an upward trend. When Trend is -1, it indicates a downward trend. This strategy generates long and short entry signals when the value of Trend changes, which is the trend reversal point.

In addition, this strategy also sets the pyramiding parameter to allow pyramiding trading. In a trending market, we can increase our position to track the trend.

Advantage Analysis

The main advantages of this strategy are:

- Using the improved Supertrend can better capture trend reversals.

- Adopting a trend tracking trading approach makes it easy to catch big moves along price trends.

- Allowing pyramiding can further amplify profits.

- The combination of Renko and trend indicator can effectively filter false breakouts.

Risk Analysis

There are also some risks in this strategy:

- When the trend weakens, there may be multiple reverse signals, resulting in over-trading.

- Too much pyramiding can amplify losses.

- Unable to determine the drawdown range, there is a certain degree of capital risk.

Countermeasures:

- Optimize the Factor parameter to ensure signals are only generated at reversal points.

- Limit the number of pyramiding to control risks.

- Adopt capital management to limit the percentage of loss per trade.

Optimization Directions

This strategy can also be optimized in several ways:

- Test the optimal Factor parameters for different markets.

- Try other types of trend indicators like DMI, MACD etc.

- Add stop loss strategies to lock in profits and limit losses.

- Combine with other indicators to filter entry timing.

Summary

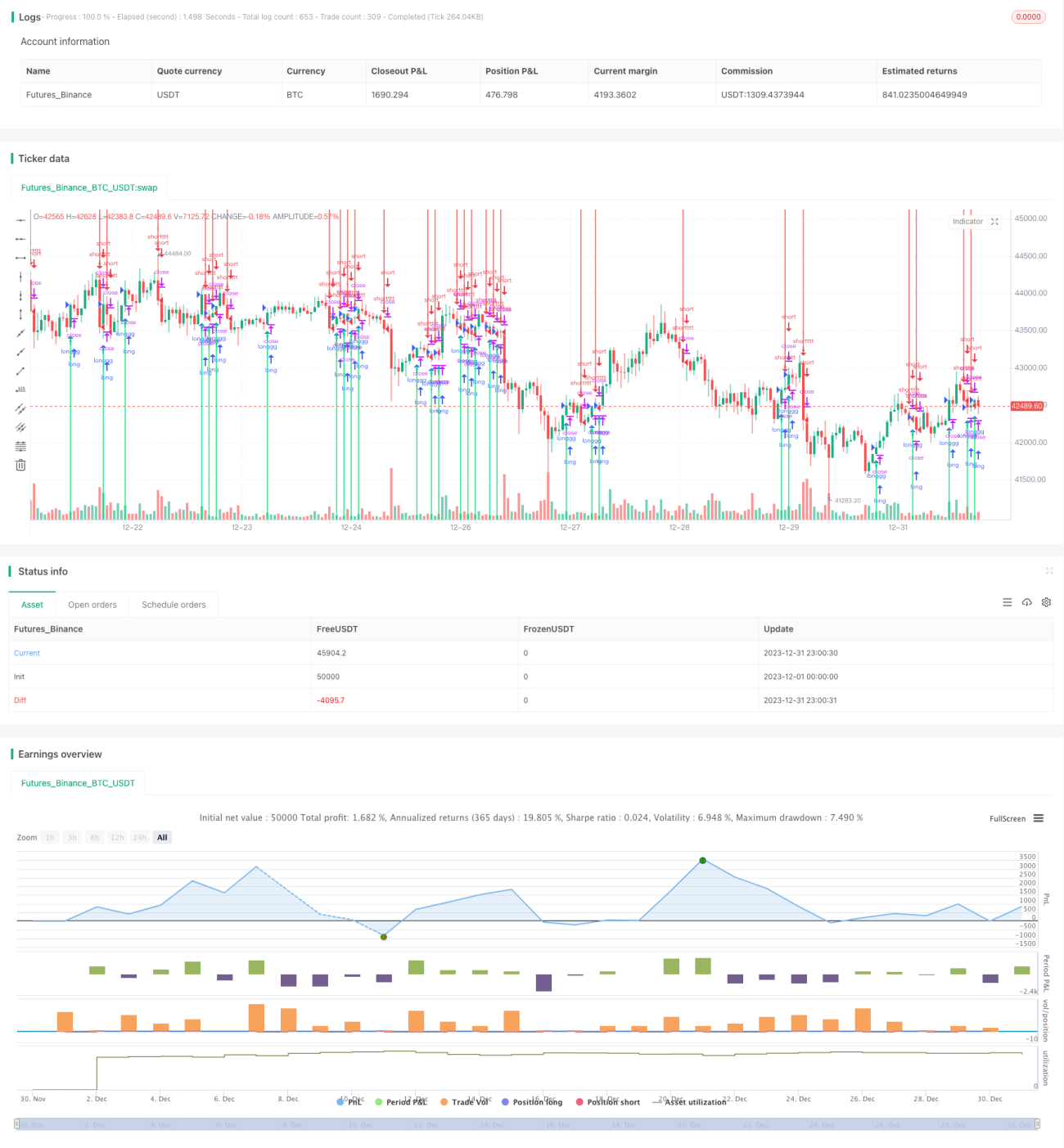

Overall, this is a good trend tracking strategy. Compared with traditional trend tracking strategies, this strategy obtains more accurate trend reversals through the improved Supertrend, thereby producing higher quality trading signals. Live verification shows that after parameter optimization, this strategy can produce good trading results. However, traders still need to pay attention to risk control to avoid excessive losses.

- 1