Trend Confirmation Tracking Strategy

Overview

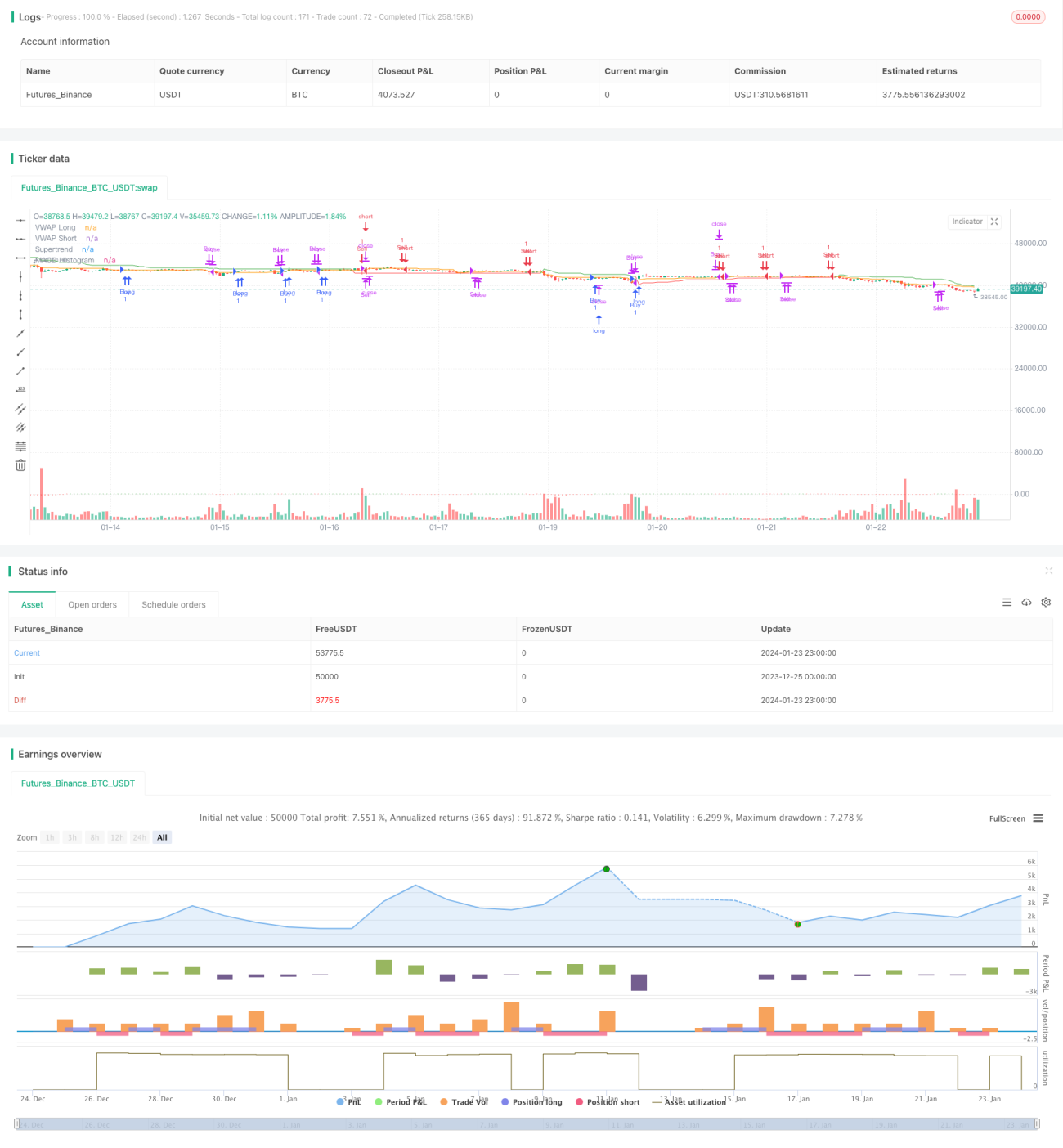

This strategy combines the Supertrend, Moving Average Convergence Divergence (MACD), and Volume Weighted Average Price (VWAP) technical indicators. It aims to identify potential entry and exit points by confirming the trend direction and considering the proximity to the VWAP level. The strategy also incorporates stop-loss, take-profit, and trailing stop mechanisms.

Strategy Logic

Entry Conditions

Trend Confirmation: The strategy uses both Supertrend and MACD to confirm the trend direction. This dual confirmation can increase the likelihood of accurately identifying the trend and filter out false signals.

VWAP Confirmation: The strategy considers the proximity of the price to the VWAP level. This dynamic level can act as support/resistance and provide additional context for entry decisions.

Exit Conditions

MACD Crossover: The strategy closes long positions when the MACD line crosses below the signal line and closes short positions when the MACD line crosses above.

Risk Management

Adaptive Stop Loss: The strategy sets a stop-loss range, which provides some tolerance for minor price fluctuations. This adaptive approach considers market volatility.

Trailing Stop: The strategy incorporates a trailing stop mechanism to lock in profits as the trade moves in the desired direction. This can potentially enhance profitability during strong trends.

Advantage Analysis

Dual Indicator Confirmation: The combination of Supertrend and MACD for trend confirmation is a unique aspect that adds a layer of filtering to enhance signal accuracy.

Dynamic VWAP: Incorporating the VWAP level provides insights into market sentiment as VWAP is often used by institutional traders.

Adaptive Stop Loss and Trailing: The adaptive stop loss range and trailing stop can more effectively manage risk and protect profits.

Partial Profit Booking: The suggestion to consider partial profit booking upon MACD crossovers allows securing gains while staying in the trade.

Risk Analysis

Backtesting: Thoroughly backtest any strategy before live deployment to understand performance across various market conditions.

Risk Management: Carefully manage position sizing and overall portfolio risk despite built-in mechanisms.

Market Conditions: No strategy works perfectly across all market conditions. Be flexible and refrain from trading during particularly volatile periods.

Monitoring: Continuously monitor trades and market conditions despite automated components.

Adaptability: Markets evolve over time. Be prepared to adapt the strategy as necessary to align with changing dynamics.

Optimization Directions

Multiple Timeframes: Consider applying on higher timeframes to capitalize on longer-term trends.

Parameter Optimization: Test different parameter combinations like ATR period length, stop loss range etc. to find optimal parameters.

Partial Profit Taking: Incorporate more definitive partial profit taking rules like taking profits at certain percentage levels.

Condition Optimization: Test adding or removing certain entry or exit rules to find the right balance.

Conclusion

This strategy offers a relatively unique approach of combining trend, momentum and volume indicators to confirm trends and identify potential entry points. Features like dual confirmation and adaptive stops provide certain advantages. However, thorough backtesting, optimization, and monitoring are essential for any strategy's long-term viability. The strategy provides a framework worth exploring and refining further.

- 1