EMA and MACD Based BTC Trading Strategy

Overview

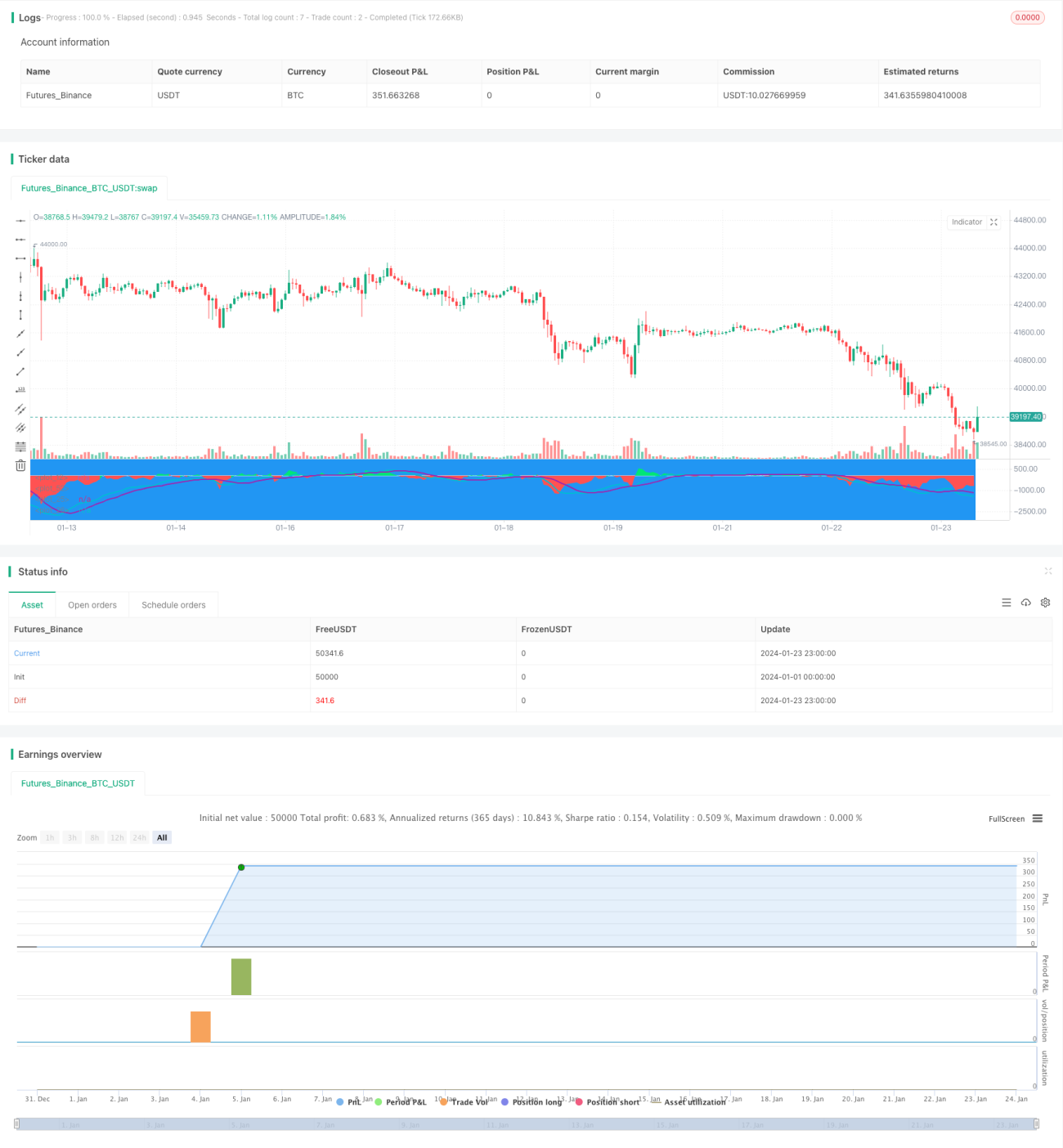

This strategy is a composite strategy based on EMA difference and MACD indicator for short-term BTC trading. It combines the signals from EMA and MACD to generate buy and sell signals under certain conditions.

Strategy Logic

It generates buy signals when the difference is negative and below a threshold and MACD has a bearish crossover. It generates sell signals when the difference is positive and above a threshold and MACD has a bullish crossover.

By combining the signals from both EMA difference and MACD, some fake signals can be filtered out and the reliability of signals is improved.

Advantage Analysis

- Uses composite indicators, more reliable signals

- Adopts short-term parameters, suitable for short-term trading

- Has stop loss and take profit settings to control risks

Risk Analysis

- Stop loss may be broken during huge market swings

- Parameters need to be optimized for different market environments

- Effects need to be tested on different coins and exchanges

Optimization Directions

- Optimize EMA and MACD parameters to fit BTC volatility

- Add position sizing and pyramiding strategies to improve capital efficiency

- Add stop loss methods like trailing stop loss to reduce risks

- Test effects on different exchanges and coins

Conclusion

This strategy integrates the strengths of both EMA and MACD indicators and uses composite signals to effectively filter out false signals. With optimized parameters and position strategies, stable returns can be achieved. But risks like stop loss being hit need attention and further testing and improvement is required.

- 1