Combo Strategy of Double Factors Reversal and Improved Price Volume Trend

Overview

This strategy combines double factors reversal and improved price volume trend sub-strategies to generate cumulative trading signals. The double factors reversal strategy is based on Ulf Jensen's idea on Page 183 of his book, generating signals when stock prices reverse over two days and the stochastic indicator conditions are met. The improved price volume trend strategy follows the joint research of price and trading volume to judge the direction and momentum of the market. The two strategies can validate each other, and combined use can improve stability.

Strategy Principles

The double factors reversal sub-strategy uses the two-day price reversal principle and the multiple judgment of the stochastic indicator. If the previous closing price is higher but the current closing price reverses downward, and the fast stochastic is below the slow stochastic while the fast stochastic is above 50, a short signal is generated. If the previous closing price is lower but the current closing price reverses upward, and the fast stochastic is above the slow stochastic while the fast stochastic is below 50, a long signal is generated.

The improved price volume trend strategy is based on the joint research of price and trading volume. The calculation formula is: PxVFactor = PriceFactor + Scale * CumPVT, where PriceFactor is the price factor, and CumPVT is the accumulated power indicator. Then calculate the Length-day simple moving average of PxVFactor and compare it with the current PxVFactor value to determine the market trend and momentum.

The combo strategy comprehensively considers the signals of the two sub-strategies. When the double factors reversal and the improved price volume trend are bullish or bearish, corresponding long and short signals are generated.

Advantage Analysis

- The double factors reversal strategy combines price reversal and stochastic indicator judgment, which can effectively identify short-term extremums and capture reversal opportunities.

- The improved price volume trend strategy incorporates the trading volume factor to judge the momentum and consolidation of the market.

- The two strategies verify each other to improve stability and avoid wrong signals.

- Using medium-term parameters of 9 or 14 days is suitable for intraday and short-term operations.

Risk and Optimization

- Reversal strategies carry the risk of being trapped, requiring stop loss to control risk.

- Volume price strategies may increase drawdowns if the market direction is incorrectly judged.

- It can be tested whether the weights of the PriceFactor and CumPVT factors are optimal for further optimization.

- Parameters of different days can be tested for the best return to drawdown ratio.

Conclusion

In conclusion, the combo strategy of double factors reversal and improved price volume trend combines the judgments of reversal and trend in two dimensions. The two can verify signals from each other to improve stability. Adding a trend indicator as an auxiliary judgment is necessary in reversal strategies where it’s easy to be trapped. And incorporating trading volume factors is also essential to determine market reversals and momentum. This strategy uses medium-term parameters suitable for intraday and short-term operations, with certain practical value.

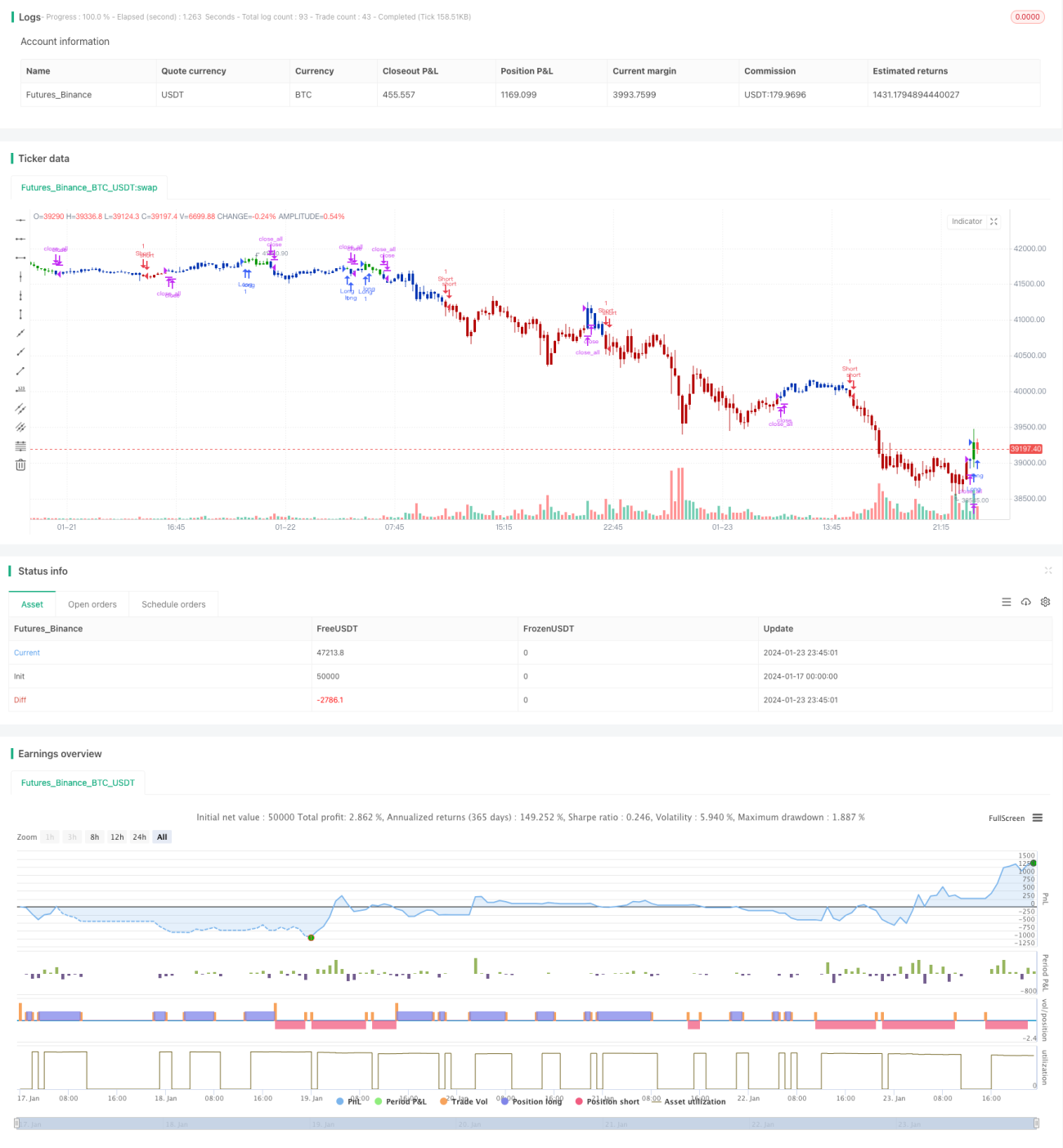

/*backtest

start: 2024-01-17 00:00:00

end: 2024-01-24 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 23/02/2021

// This is combo strategies for get a cumulative signal. - 1