Momentum Moving Average Crossover Quant Strategy

Overview

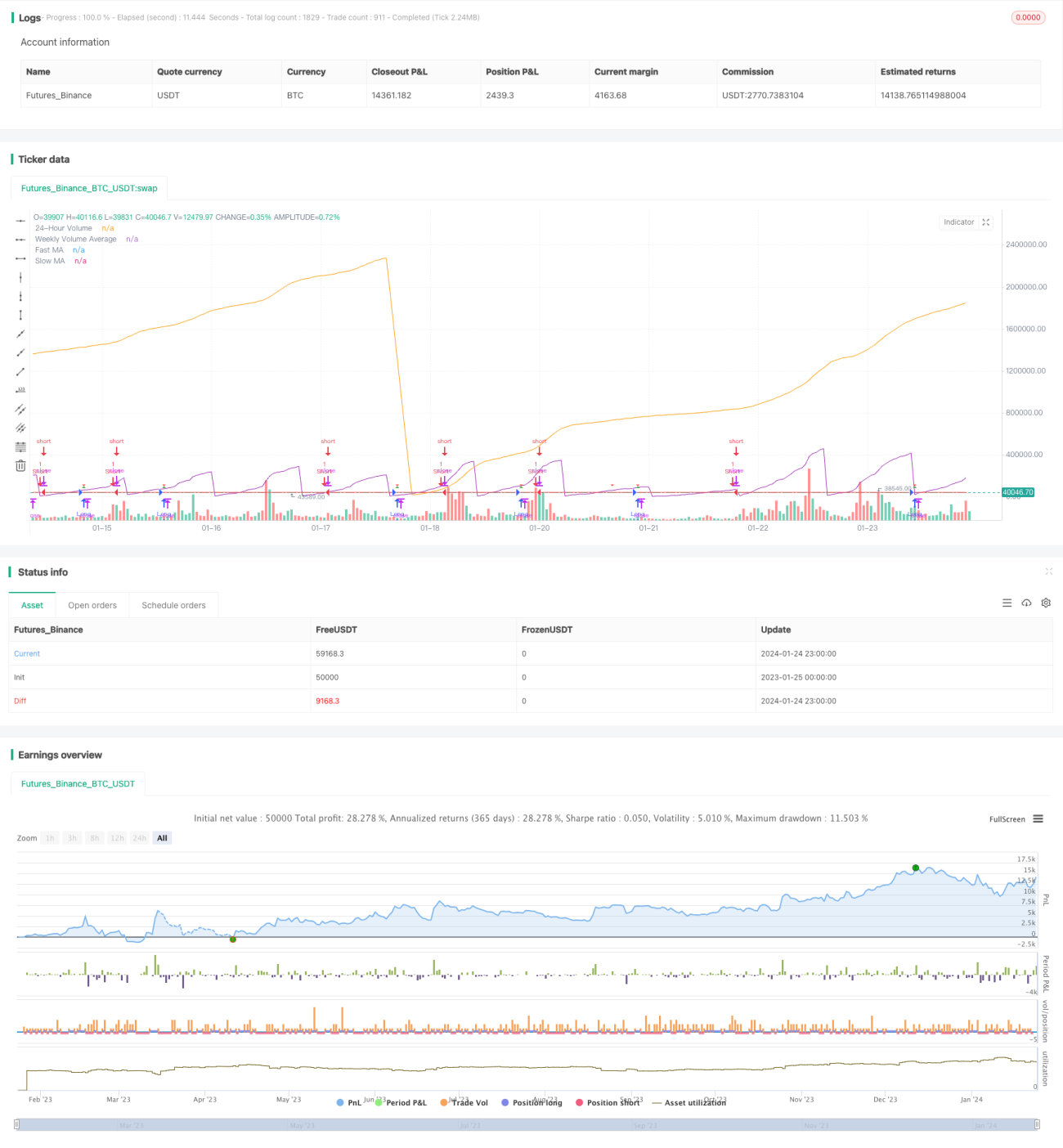

This strategy combines the moving average and trading volume indicators to design the long and short entry and exit rules, forming a complete quantitative trading strategy.

Strategy Principle

Key Indicators

- Moving Averages: Fast MA (Blue Line) and Slow MA (Red Line)

- Volume: 24-hour Volume (Purple) and 7-day Average Volume (Orange)

Strategy Conditions

Long Entry Conditions:

- Fast MA crosses above Slow MA

- 24-hour Volume below 50% of 7-day Average Volume

Short Entry Conditions:

Fast MA crosses below Slow MA

Entries and Exits

Long Entry: Go long when long conditions are met

Short Entry: Go short when short conditions are met

Take Profit and Stop Loss:

Displayed take profit and stop loss levels for long position

Advantage Analysis

- Combining price and volume avoid false breakout

- Clear entry and exit rules

- Take profit and stop loss to control risk

Risk Analysis

- Frequent trading with moving average strategy

- Unreliable volume data quality

- Overoptimization in parameter tuning

Improvements:

- Adjust MA parameters to reduce trading frequency

- Verify signals with more data sources

- Strict backtesting to prevent overoptimization

Optimization Directions

- Add other indicators to filter signals

- Dynamic take profit and stop loss

- Multiple timeframe analysis to improve stability

Summary

This strategy integrates MA and volume indicators to design a complete quant strategy with clear entry conditions, take profit/stop loss, easy to operate. Need to prevent frequent trading issue, monitor volume data quality and overoptimization. NEXT steps are multivariate optimization, dynamic TP/SL and multiple timeframe analysis.

- 1