Multi-indicator Composite Trading Strategy

Overview

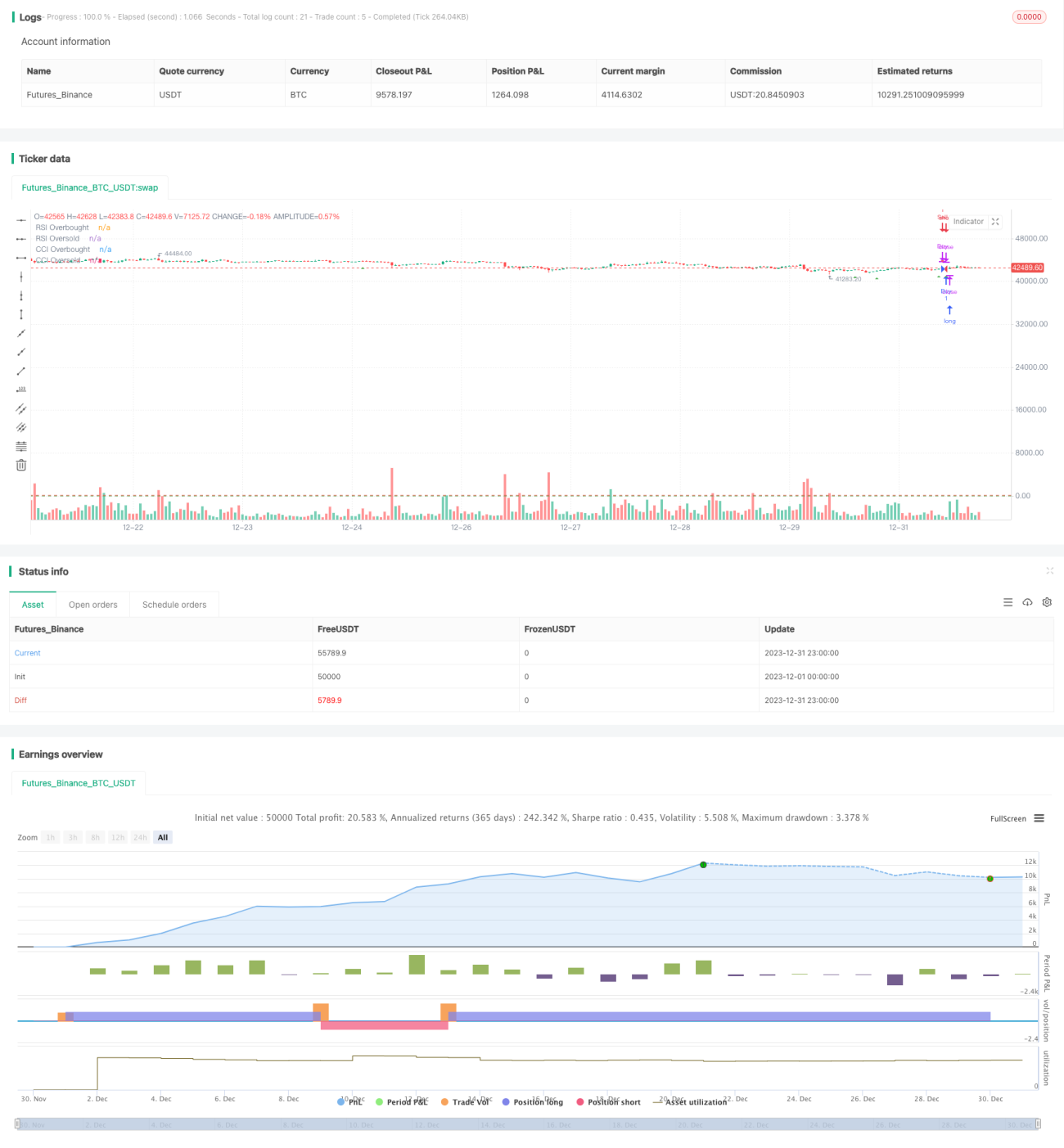

The multi-indicator composite trading strategy integrates four major indicators: moving average convergence divergence (MACD), relative strength index (RSI), commodity channel index (CCI) and stochastic relative strength index (StochRSI). It is a composite trading strategy that analyzes signals across these four indicators. By judging indicator signals across different timeframes, this strategy can more accurately identify market entry and exit points.

Strategy Logic

This strategy mainly makes judgments based on four indicators:

-

MACD: Calculates the difference between fast and slow moving averages to judge price momentum and trends. A buy signal is generated when the fast line crosses above the slow line.

-

RSI: Calculates the magnitude of price changes over a period of time. An RSI above 70 indicates overbought conditions and below 30 oversold. This strategy uses 70 and 30 as thresholds.

-

CCI: Measures price momentum by calculating the percentage deviation of price from its moving average. This strategy uses 100 and -100 as thresholds.

-

StochRSI: Combines Stochastics and RSI. A golden cross between the StochRSI %K and %D lines signals a buy, while a death cross signals a sell.

Only when all four indicators meet the criteria simultaneously will an actual buy or sell signal be generated.

Advantages

The key advantages of this multi-indicator strategy are:

-

Filters false signals by requiring agreement of all indicators, avoiding chasing tops or panic selling bottoms.

-

Captures primary trends across different dimensions by combining different indicator perspectives.

-

Large parameter optimization space to tune each indicator for overall optimal performance.

-

Weights can be adjusted based on bull or bear markets to focus on trend or mean reversion strategies.

Risks

The main risks are:

-

Indicators may generate concurrent false signals, triggering incorrect trades.

-

Prices can move violently enough for concurrent false signals across indicators.

-

Delayed buy signals as indicators align.

-

Difficult to optimize many parameters, possibly overfit.

Mitigations include parameter tuning, stop losses, and position sizing control.

Enhancement Opportunities

Enhancement opportunities:

-

Test combinations with more indicators like KD, Bollinger Bands to find optimal portfolio.

-

Optimize parameters for highest overall performance, maybe via machine learning.

-

Customize parameters for different stocks and sectors.

-

Add stop loss mechanisms in strategy code, like selling when price breaches support.

-

Select stocks with strong performance within sectors to improve portfolio returns.

Conclusion

This strategy integrates signals across four major indicators – MACD, RSI, CCI, and StochRSI. By setting strict entry and exit criteria based on multi-timeframe analysis, it can effectively identify market turning points. Refinements like parameter optimization, updating stock universe, and adding stops can further improve performance. Overall an effective quantitative trading strategy.

- 1