Scalping Strategy with Volume and VWAP Confirmation

Overview

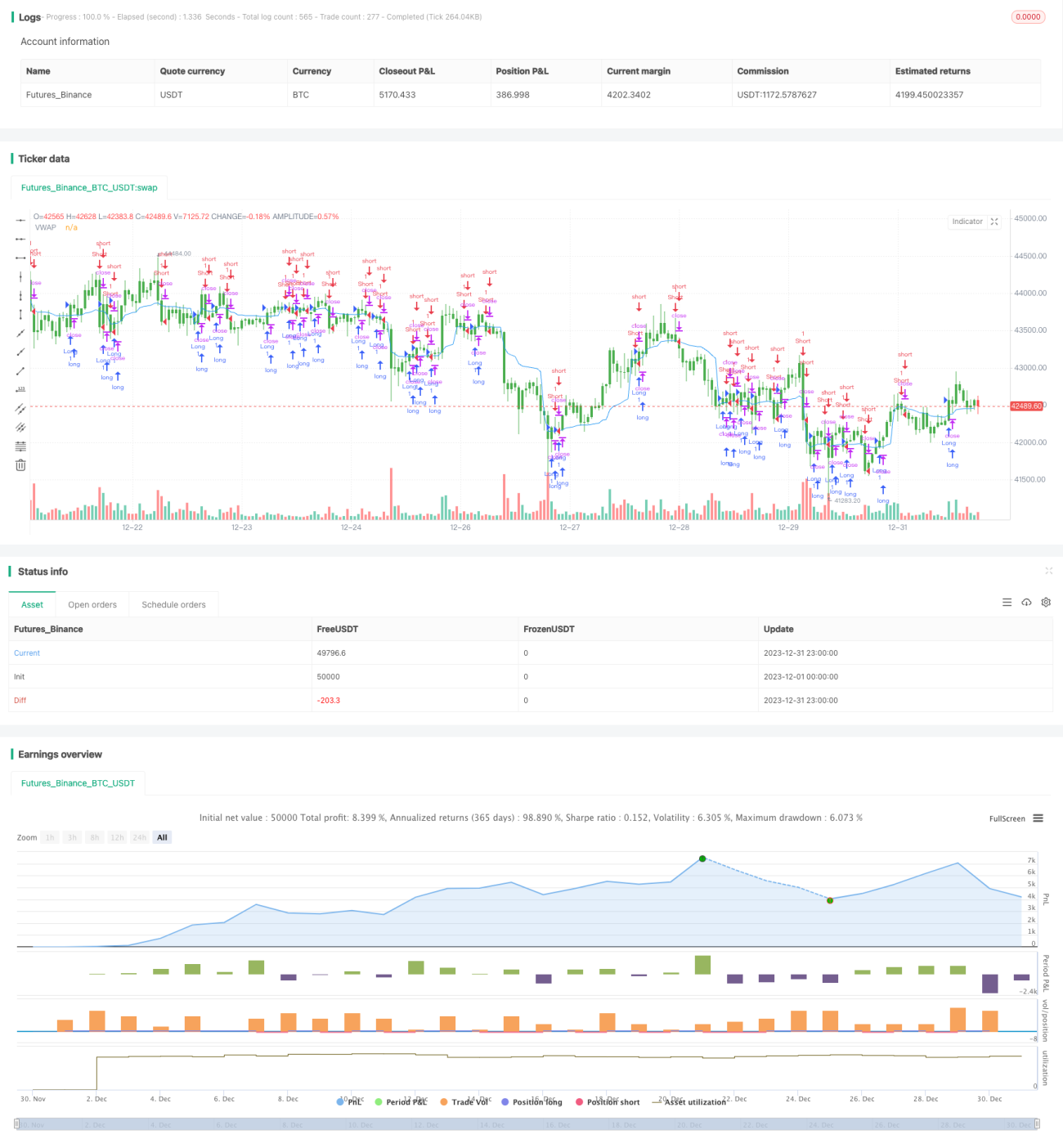

This is a scalping strategy that utilizes volume and Volume Weighted Average Price (VWAP) for confirmation. It combines these two important technical indicators to identify trends and locate higher probability entry points.

Strategy Logic

The strategy mainly relies on two indicators for decision making - volume and VWAP.

Firstly, it calculates the 20-period VWAP. VWAP represents the average price of the day, and is an important benchmark for assessing price reasonableness. If the price is higher than VWAP, it indicates stronger bullish forces, and vice versa for bearish forces.

Secondly, the strategy also checks if the volume of each candlestick bar exceeds the preset threshold of 100. Only when the trading volume is sufficiently active, a definite trend is considered to exist. This avoids incorrect trades when the market is dull and inactive.

Based on these two criteria, the entry and exit rules are formed:

Entry Conditions

- Long: Close > VWAP and Volume > 100

- Short: Close < VWAP and Volume > 100

Exit Conditions

- Long: Close < VWAP

- Short: Close > VWAP

As we can see, the strategy combines both the price indicator VWAP and volume, using dual confirmation to improve stability.

Advantages

The main advantages of this strategy include:

- Using VWAP to gauge price reasonableness, avoiding blind trend following

- Confirming signals with volume to make them more reliable

- High operation frequency, suitable for scalping, allowing higher profits

- Simple and clear logic, easy to understand and implement

- Considers both VWAP and volume for dual confirmation and higher win rate

Risks

There are also some risks to note:

- As a scalping strategy, high operation frequency leads to higher transaction costs and slippage

- VWAP signals may be incorrect when market trend is unclear

- Volume indicator less applicable for low liquidity stocks

- Difficult to universally optimize parameters like volume threshold

- Scalping requires close monitoring of the markets

To mitigate risks, high liquidity stocks with narrow price range and volatility are recommended. Fine tune parameters for different stocks. Also control position sizing to limit losses.

Optimization

Some ways to further optimize the strategy:

- Optimize VWAP parameter for individual stocks

- Set volume threshold based on average daily volume

- Add other filters when there are no positions to avoid false signals

- Incorporate stop loss for max loss control

- Adjust position sizing rules for higher profit ratio

Through parameter tuning, adding filters, stop loss etc, we can further improve the stability and profitability.

Conclusion

The strategy consolidates two major indicators, VWAP and volume, to pick stocks with price reasonableness and high volume confirmation. It has high operation frequency and strong trend capturing capability. At the same time, trading costs and stop losses should be managed. Further optimizations can lead to even better strategy performance.

- 1