Robust Trend Continuation Strategy

Overview

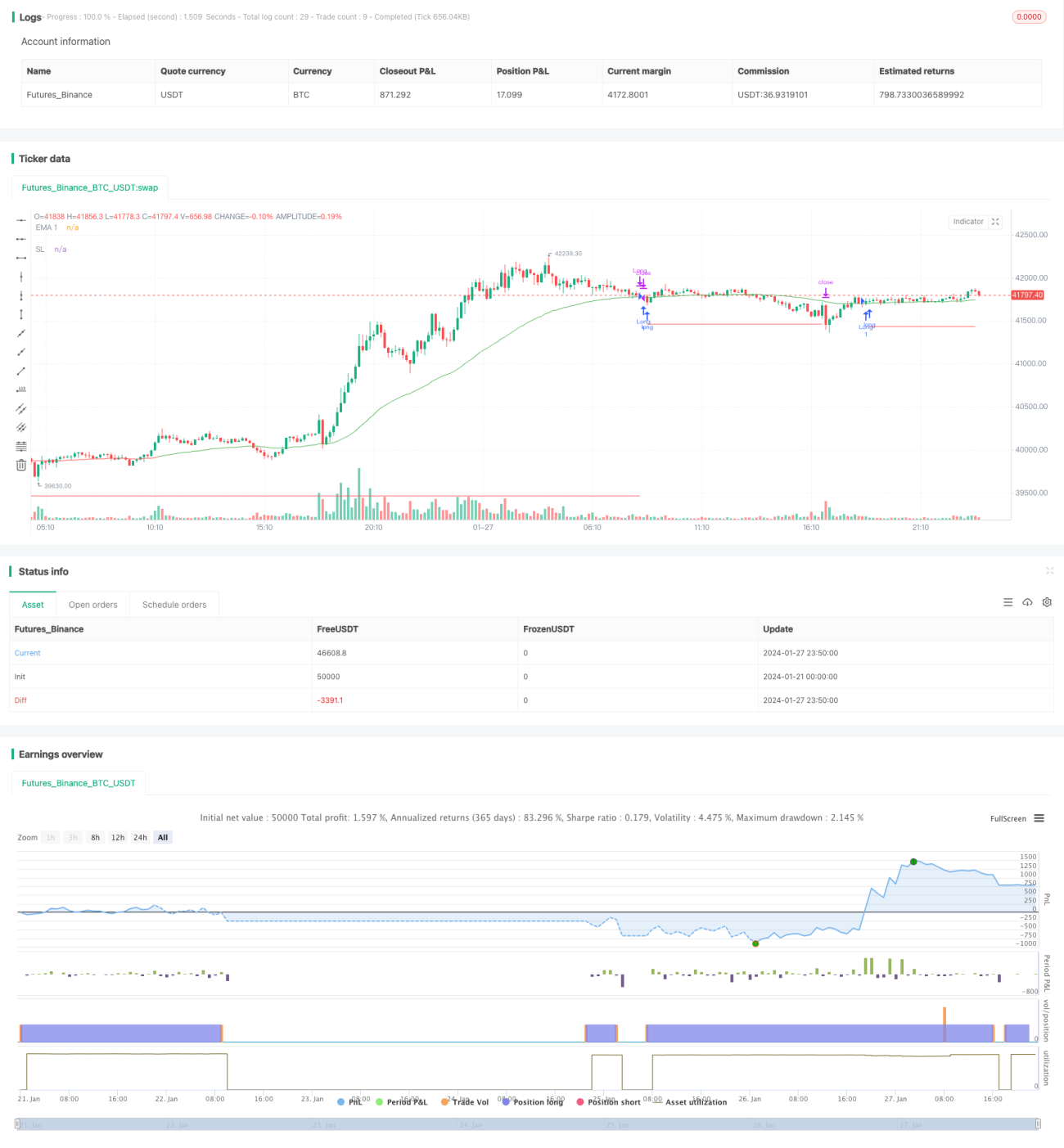

This strategy is based on moving averages. It goes long after a short-term correction in an upward trend. It belongs to the trend following strategy.

Strategy Principle

This strategy uses 3 EMA lines with different periods. The EMA1 line with shorter period is used to judge the short-term trend. The EMA2 and EMA3 lines with longer periods are used to determine the mid-long term trend, where EMA3 has the longest period. When the short-term EMA1 line goes up, it indicates that it is in a short-term upward trend. If EMA2 is above EMA3, it means the mid-long term is also in upward trend, so this is a good timing for long entry. Specifically, the trading signal is generated when the price crosses above the EMA1 line. To further verify the stability of the trend, it requires that EMA2 and EMA3 are pointing up and the last bar is also rising in the signal generation bar, which helps filter out wrong signals from short-term corrections.

The stop loss line and take profit line are set to lock in profits and losses. Specifically, the stop loss line moves according to the ATR value, and the take profit line also moves based on the ATR value.

Advantage Analysis

The biggest advantage of this strategy is that it can effectively capture the mid-long term upward trend, while also taking into account the short-term correction, which makes its holding time and profit space considerable.

In addition, the setting of stop loss and take profit also makes its risk controllable.

Risk Analysis

The biggest risk of this strategy is that it cannot determine the trend reversal point. If the mid-long term trend reverses while the short term is still rising, it will generate a wrong long signal to enter the market, which may cause greater loss.

In addition, unnecessary trading losses may also occur in range-bound markets.

Optimization Directions

Consider adjusting the cycle parameters of EMA based on the characteristics of specific trading varieties to better match the mid-long cycle of the variety.

Combining with other indicators to determine the end of short-term adjustments can avoid wrong entry.

Consider adjusting the stop loss coefficient based on the ATR value, appropriately relaxing the stop loss distance when ATR is large.

Conclusion

In general, this strategy is a mid-long term trend following strategy that performs well. It determines the trend direction through moving averages, entry timing through pullback signals, and locks in profits and losses through stop loss and take profit settings. But there is also a certain risk of blind trend following. Traders need to make their own judgment on the market to decide whether to enter.

- 1