Bull Market Tracking System

Overview

The Bull Market Tracking System is a mechanical trading system based on trend tracking. It uses trend indicators on the 4-hour chart to filter trading signals, while entry decisions are made based on indicators from the 15-minute chart. The main indicators include RSI, Stochastics, and MACD. The advantage of this system is that the combination of multiple timeframes can effectively filter out false signals, while the shorter timeframe indicators can pinpoint more precise entry timing. However, there are also some risks with this system, such as overtrading and false breakout issues.

Principles

The core logic of this system is to combine indicators from different timeframes to identify trend direction and entry timing. Specifically, the RSI, Stochastics, and EMA on the 4-hour chart need to align to determine the overall trend direction. This can effectively filter out most of the noise. At the same time, the RSI, Stochastics, MACD and EMA on the 15-minute chart also need to agree on either bullish or bearish bias to determine the precise entry timing. This allows us to find good entry and exit points. Only when the judgments on both the 4-hour and 15-minute timeframes meet the criteria will the system generate trading signals.

Advantages

- Multiple timeframe combinations can effectively filter out false signals and identify major trends

- 15-minute detailed indicators can capture relatively precise entry timing

- The combination of indicators including RSI, Stochastics, MACD and other mainstream technical indicators is easy to understand and optimize

- Strict risk management methods are adopted such as take profit, stop loss, trailing stop loss etc. to effectively control the risk of individual trades

Risks

- Overtrading risk. The system is quite sensitive to short-term timeframes, which may generate a lot of trading signals, leading to overtrading

- False breakout risk. Short-term indicator judgments may be wrong, resulting in false breakout signals

- Indicator failure risk. Technical indicators themselves have certain limitations and may fail in extreme market conditions

Accordingly, the system can be optimized from the following aspects:

- Adjust indicator parameters to make them more suitable for different market environments

- Increase filter conditions to reduce trading frequency and prevent overtrading

- Optimize stop profit and stop loss strategies to better fit market fluctuation ranges

- Test different combinations of indicators to find the optimal solution

Summary

Overall, the Bull Market Tracking System is a very practical trend following mechanical trading system. It uses a combination of multi-timeframe indicators to identify market trends and key entry timing. With reasonable parameter settings and continuous optimization testing, the system can adapt to most market environments and achieve steady profits. However, we also need to be aware of some of the potential risks, and take proactive measures to prevent and mitigate these risks.

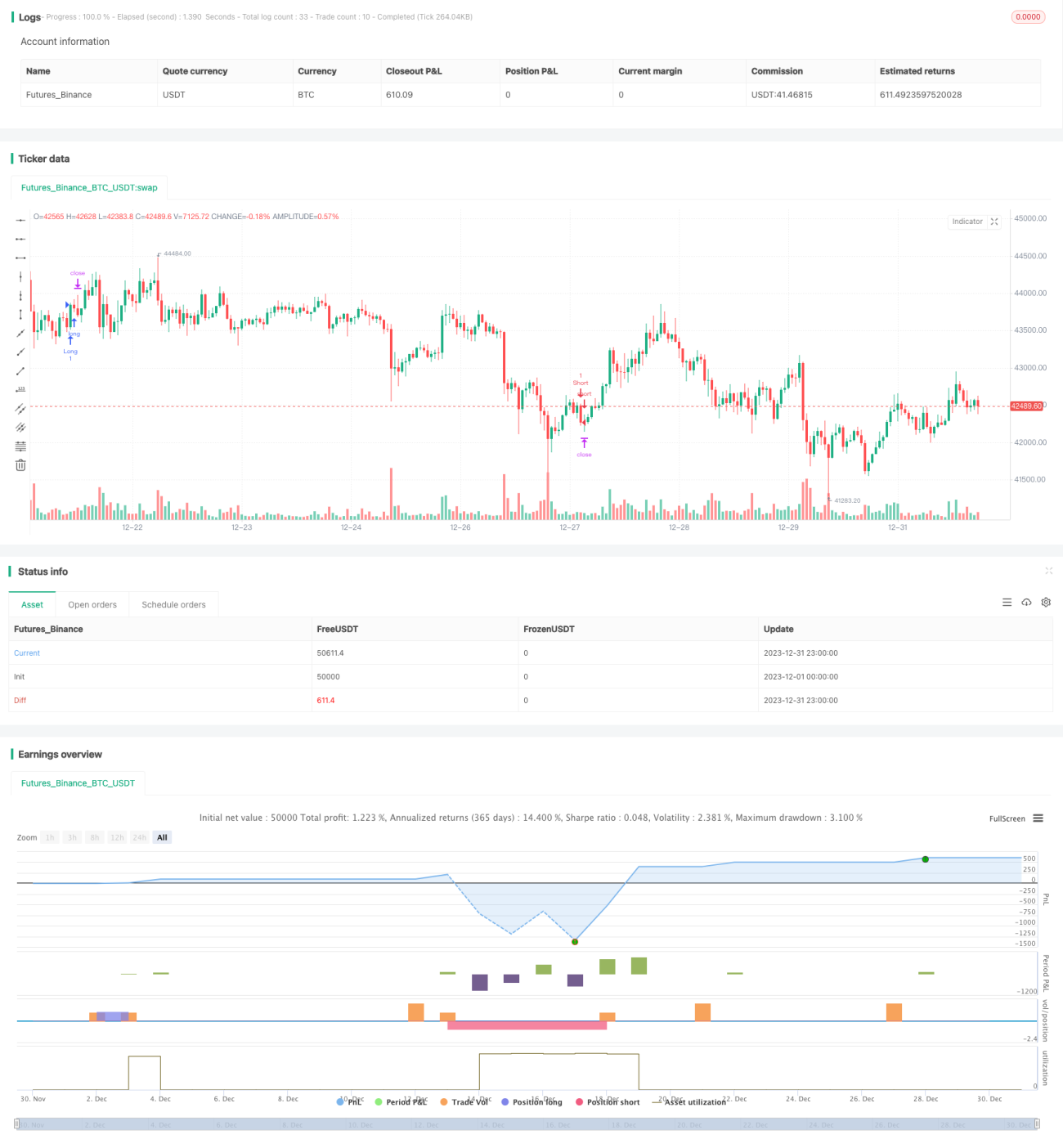

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Cowabunga System from babypips.com", overlay=true)

// 4 Hour Stochastics

length4 = input(162, minval=1, title="4h StochLength"), smoothK4 = input(48, minval=1, title="4h StochK"), smoothD4 = input(48, minval=1, title="4h StochD")- 1