Bitcoin Trading Strategy Based on Ichimoku Cloud

Overview

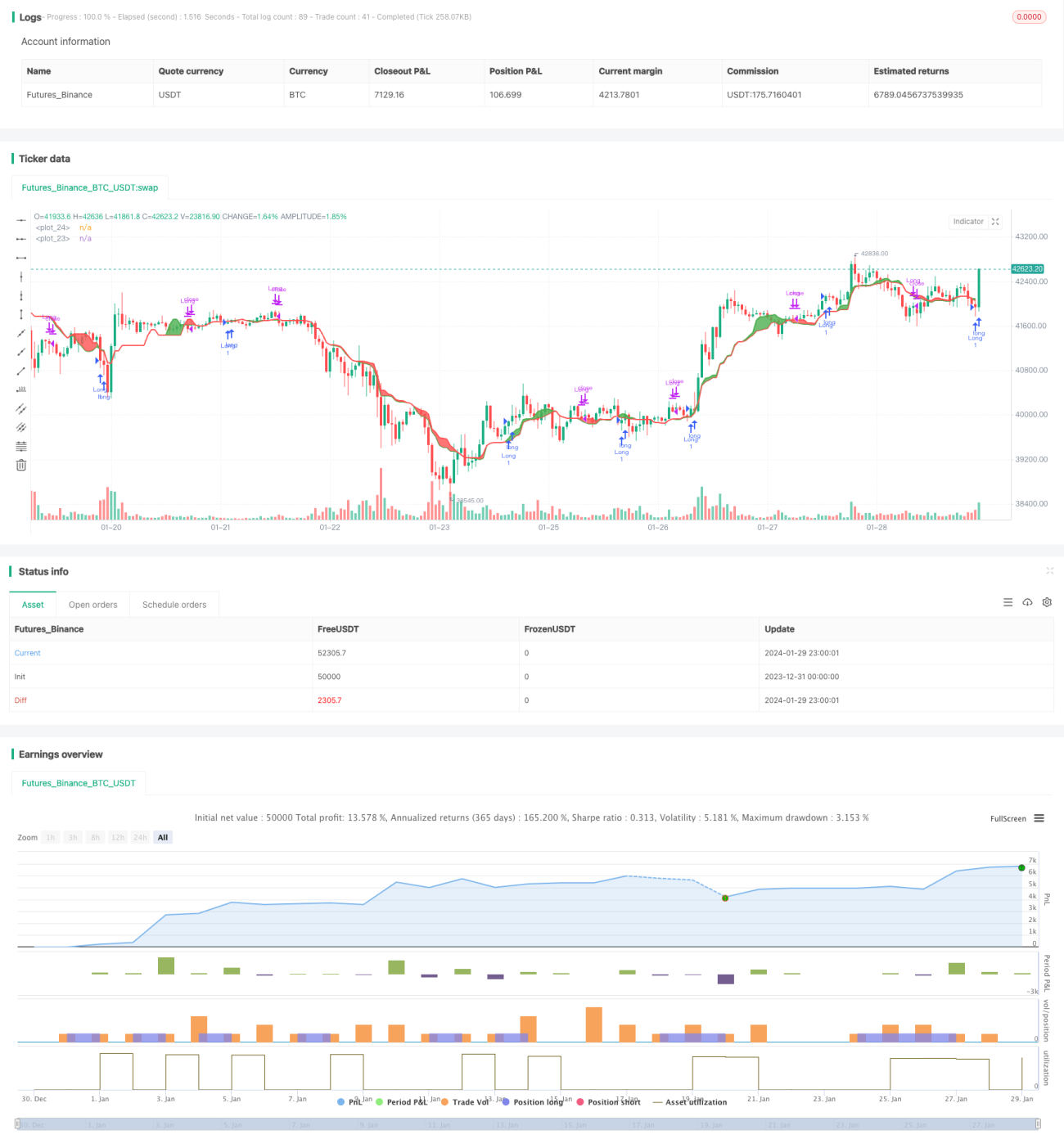

This strategy is a bitcoin trading strategy designed based on the Ichimoku cloud indicator. It generates trading signals when the short-term line crosses over the long-term line by calculating the equilibrium prices over different periods.

Strategy Logic

The strategy uses the Ichimoku cloud indicator. The specific formulas are:

Lmax = highest price over period_max

Smax = lowest price over period_max

Lmed = highest price over period_med

Smed = lowest price over period_med

Lmin = highest price over period_min

Smin = lowest price over period_min

HL1 = (Lmax + Smax + Lmed + Smed)/4

HL2 = (Lmed + Smed + Lmin + Smin)/4

It calculates the equilibrium prices for the long-term line HL1 and short-term line HL2. A long signal is generated when HL2 crosses over HL1. A close signal is generated when HL2 crosses below HL1.

Advantage Analysis

The advantages of this strategy include:

- Using Ichimoku cloud filters market noise and identifies trends effectively.

- Crossover of different period lines generates trading signals and reduces false signals.

- The logic is simple and easy to understand and implement.

- Customizable period parameters adapt to different market environments.

Risk Analysis

There are also some risks:

- Ichimoku cloud has lagging and may miss short-term signals.

- Crossover of long and short term lines can be vulnerable to arbitrage.

- Signals may become unreliable during high volatility.

These risks can be reduced by optimizing parameters or incorporating other indicators.

Optimization Directions

The strategy can be optimized in the following aspects:

- Optimize long and short term periods to adapt to market changes.

- Add stop loss to control losses.

- Incorporate other indicators like MACD to improve accuracy.

- Suspend trading at high volatility periods to avoid huge losses.

Conclusion

This strategy generates signals when short-term equilibrium line crosses over long-term line based on Ichimoku cloud. Compared to single indicators, it effectively filters out false signals. Further improvements on parameters and risk control can enhance its stability and profitability.

- 1