Donchian Trend Following Strategy

Overview

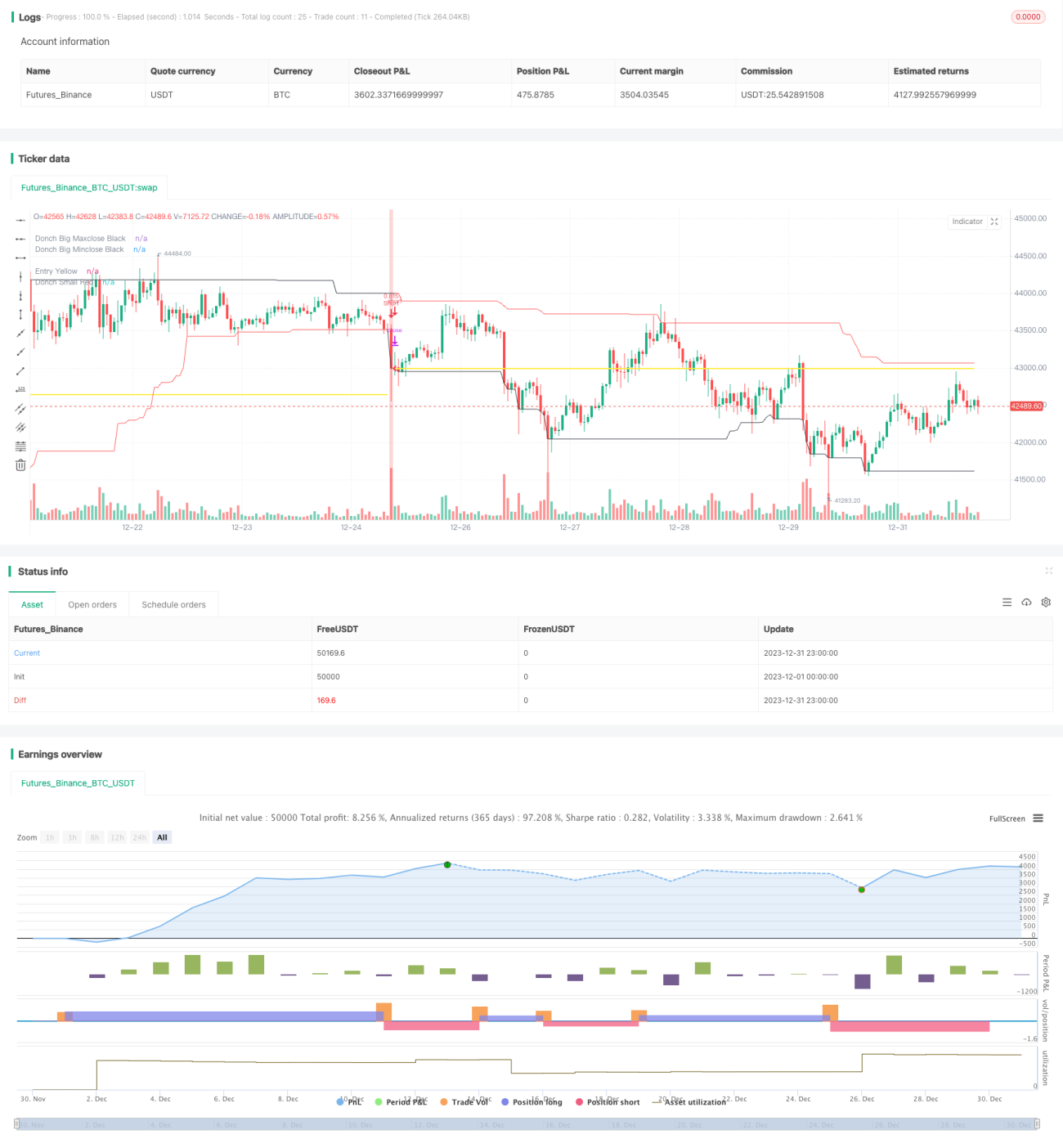

The Donchian Trend Following strategy is developed based on the Donchian Channel principle described in the article "Black Box Trend Following – Lifting the Veil". This strategy uses the Donchian Channel to determine the trend direction and establishes long or short positions when prices hit new highs or lows.

Strategy Logic

The strategy is based on the Donchian Channel indicator to judge the trend direction. The Donchian Channel consists of a longer period channel and a shorter period channel. When the price breaks through the longer period channel, it signals the start of a trend. When the price breaks through the shorter period channel, it signals the end of the trend.

Specifically, the longer period channel length is 50 days or 20 days, and the shorter period channel length is 50 days, 20 days or 10 days. If the price equals the highest price in 50 days, a long position is opened. If the price equals the lowest price in 50 days, a short position is opened. If the price equals the lowest price in 20 or 10 days, long positions are closed. If the price equals the highest price in 20 or 10 days, short positions are closed.

By combining two Donchian Channels of different periods, it can determine the direction to establish positions when a trend starts, and realize timely stop loss when the trend ends.

Advantage Analysis

The main advantages of this strategy are:

-

Strong ability to capture trends. It can track trends effectively by identifying the start and end of trends using Donchian Channel breakouts.

-

Proper risk control. It uses a moving stop loss to control single trade loss.

-

Flexible parameter adjustment. The combination of channel periods can be freely selected to adapt to different products and market environments.

-

Simple and clear trading logic. It is easy to understand and implement.

Risk Analysis

The risks of this strategy include:

-

Inability to adapt to range-bound markets. It will suffer consecutive small stop loss when the trend is unclear.

-

Breakout failure risk. Prices may pullback after breaching the channel, causing stop loss.

-

Period selection risk. Inappropriate channel period settings may lead to trading in noise.

-

Sharpe ratio decline risk. Increasing position size without adjusting stop loss may lead to declining Sharpe ratio.

The solutions are:

- Optimize parameters to select suitable channel period combinations.

- Adjust position size and stop loss properly to control risk.

- Use this strategy for products and markets with obvious trends.

Optimization Directions

The optimization directions for this strategy:

-

Adding filter conditions to avoid whipsaws, e.g. combining volume to judge true breakouts.

-

Optimizing channel period combination and position sizing to increase profit ratio. Adaptive stop loss can be introduced.

-

Trying breakpoint optimization to find optimal parameter sets.

-

Increasing machine learning algorithms for dynamic optimization and adjustment of parameters.

Conclusion

The Donchian Trend Following Strategy identifies the start and end of price trends using dual channels, and adopts trend following trading style with effective single trade loss control. This strategy has flexible parameter adjustment and easy implementation, making itself a very practical trend following strategy. But the insufficient profitability in range-bound markets and risks from parameter selection should be noted. Further optimizations can lead to better strategy performance.

- 1