Reversal Breakout Bandpass Combo Strategy

Overview

This is a combo strategy driven by two factors - reversal and bandpass, which achieves multi-factor overlay and adapts to different market conditions.

Strategy Logic

The strategy consists of two sub-strategies:

-

123 Reversal Strategy: When the close price drops for two consecutive days, if today's close breaks through the lowest price in the previous two days, and the fast line of 9-day Stochastic oscillator crosses above the slow line, go long. When the close price rises for two consecutive days, if today's close drops below the highest price in the previous two days, and the fast line crosses below the slow line, go short.

-

Bandpass Filter: Calculate a bandpass indicator over a certain period, go long when it is above a threshold, and go short when below.

The combined signal is: take long position if both strategies give long signals, take short position if both give short signals, otherwise clear all positions.

Advantages

- Driven by dual factors, adapts to various market conditions, profitable across regimes

- 123 reversal captures reversal opportunities in range-bound markets

- Bandpass filter tracks trends in trending markets

- Combined signal verifies and avoids erroneous trades

Risks

- Improper parameters may cause over-trading

- Multiple losses may occur in choppy markets

- Transaction costs need to be monitored

Enhancement

- Tune bandpass filter parameters to optimize bandpass calculation

- Adjust 123 reversal parameters to optimize long/short reversal identification

- Add stop loss to control losses for single trades

Summary

This strategy integrates reversal and trend factors to achieve multi-factor driven quantitative trading. The dual-factor verification reduces the probability of erroneous trades, making the strategy perform well across various markets. Further improvements on parameter tuning and stop loss will enhance the strategy's stability and profitability.

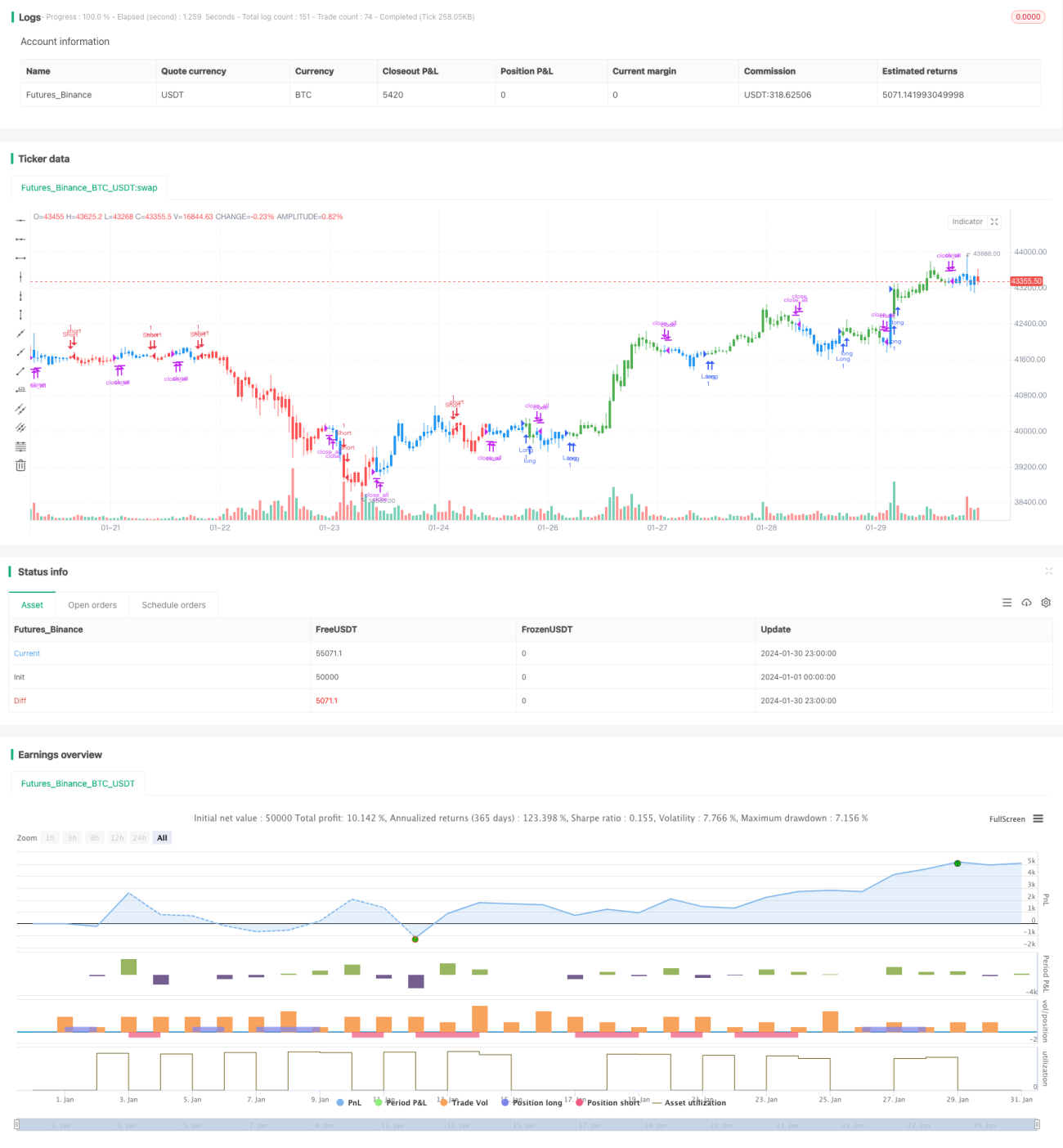

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 21/05/2019

// This is combo strategies for get - 1