Self-adaptive Quant Grid Trading Strategy

Overview

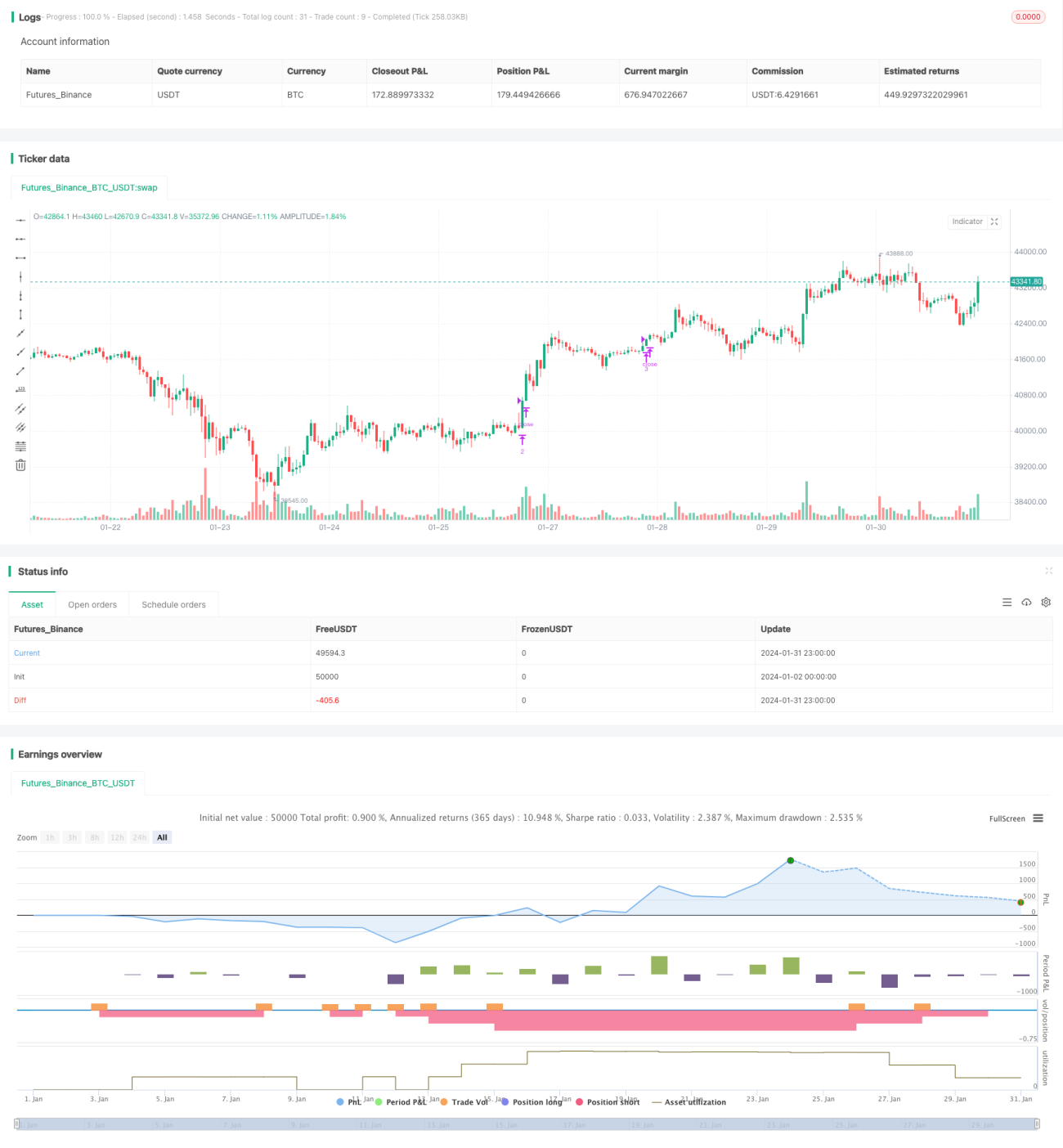

This strategy establishes a dynamic trading grid to achieve steady profits amid volatile markets. It automatically calculates grid spacing and upper/lower limit based on the preset number of grid lines. When the price breaks through each grid line, long/short positions will be built up in batches. Profits will be taken when the price hits the original grid lines again. The strategy supports both manual and automatic adjustment of grid parameters to adapt itself to changing market conditions.

Strategy Logic

-

Calculate grid boundaries and grid line price array based on input parameters.

-

When the price falls below a grid line without corresponding orders, long orders will be placed at the grid line price. When the price rises above the previous grid line (the first excluded) with existing position, the long orders of the previous line will be closed.

-

If auto adjustment is enabled, grid upper/lower limits, grid spacing and grid arrays will be recalculated periodically based on recent candlestick data.

Advantage Analysis

-

Realize steady profits amid volatile market. Long/short positions are built up and closed in batches at different price levels to achieve overall profit.

-

Support both manual and automatic parameter adjustment. Manual adjustment offers better control but requires intervention. Automatic adjustment reduces workload and adapts to changing market dynamics.

-

Max loss capped by limiting max number of grid lines. When price breaks all grid lines, risks are contained.

-

Tune grid spacing to adjust profit/loss per trade. Smaller spacing lowers exposure per trade.

Risk Analysis

-

Risk of being trapped in whipswa. Frequent price oscillation within grid range may lead to losses.

-

Require adequate initial capital. Insufficient funding cannot support enough grid lines.

-

Extreme grid numbers disadvantage profits. Too few grids fail to take full advantage of volatility while too many grids lead to minimal profits per trade. Extensive testing needed to determine optimal settings.

-

Auto adjustment risks price manipulation. Relies on recent candlesticks which can be affected by short-term price operations.

Optimization

-

Introduce stop loss logic such as trailing stop loss to futher restrict downside risk per direction.

-

Optimize grid parameters via machine learning. Test different parameters across market conditions and train ML models to obtain optimal, adaptive parameters.

-

Incorporate additional technical indicators. Assess current trend strength with indicators like MACD and RSI to guide grid quantity and parameter tuning.

-

Enhance risk control by setting maximum allowable drawdown percentage. Disable strategy when threshold is breached to prevent further losses.

Conclusion

This strategy fully utilizes the characteristics of volatile markets and achieves steady profits through dynamic grid trading framework that offers both parameter flexibility and ease of operation. With further enhancements in loss control and automatic parameter optimization, it can become an ideal model for creating durable profits from market fluctuations.

/*backtest

start: 2024-01-02 00:00:00

end: 2024-02-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("(IK) Grid Script", overlay=true, pyramiding=14, close_entries_rule="ANY", default_qty_type=strategy.cash, initial_capital=100.0, currency="USD", commission_type=strategy.commission.percent, commission_value=0.1)

i_autoBounds = input(group="Grid Bounds", title="Use Auto Bounds?", defval=true, type=input.bool) // calculate upper and lower bound of the grid automatically? This will theorhetically be less profitable, but will certainly require less attention

i_boundSrc = input(group="Grid Bounds", title="(Auto) Bound Source", defval="Hi & Low", options=["Hi & Low", "Average"]) // should bounds of the auto grid be calculated from recent High & Low, or from a Simple Moving Average- 1