Momentum Breakout Trading Strategy

Overview

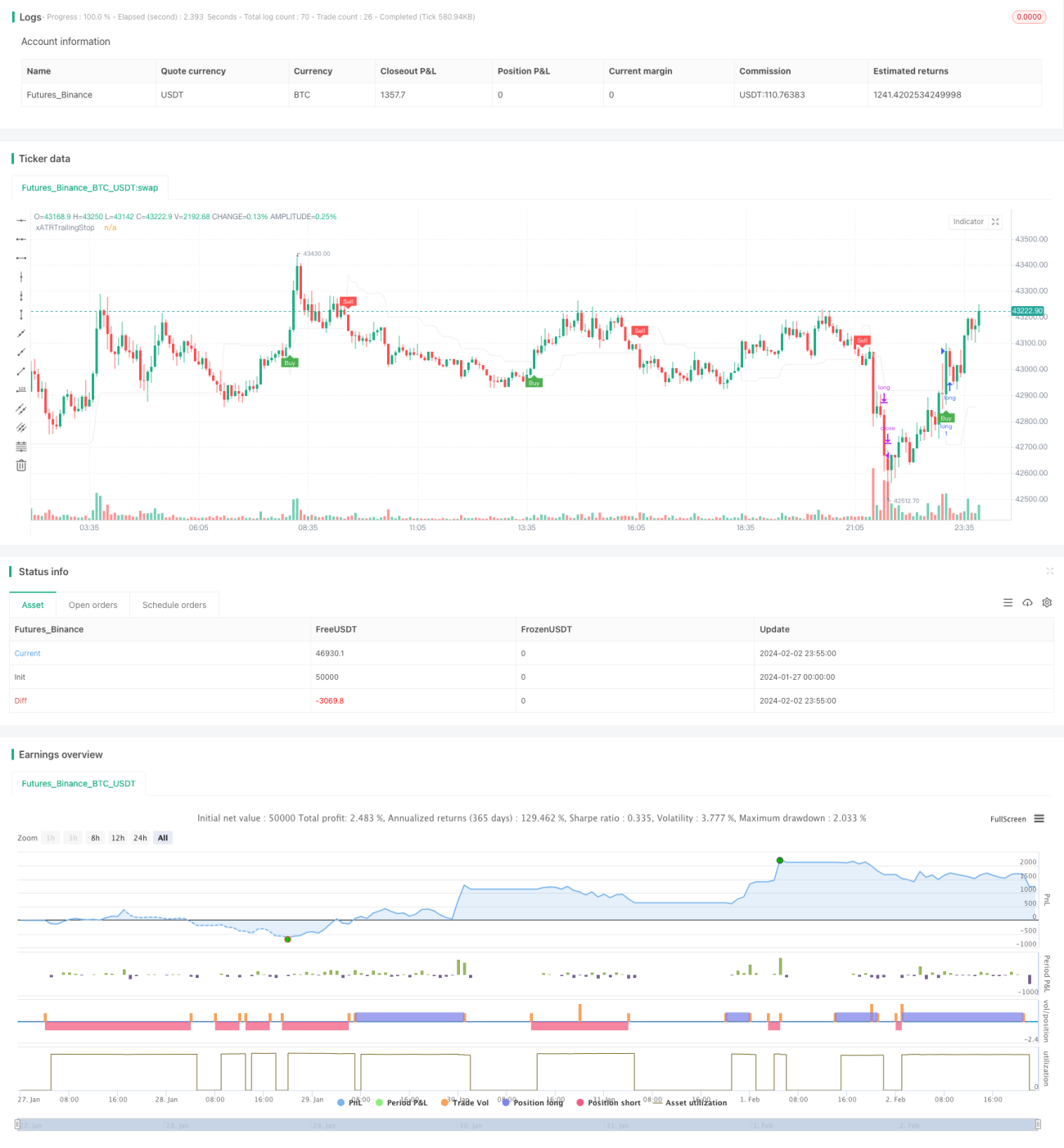

This is a momentum-based breakout trading strategy. It uses moving averages, ATR, RSI and other indicators to judge market trends and volatility, combined with strict stop loss/take profit settings for trading. The strategy mainly judges whether prices break through or fall below the moving averages plus the ATR range to generate trading signals.

Strategy Principle

The main points of this strategy are:

-

Use EMA to judge the price trend direction. Price crossing above EMA is bullish signal and crossing below is bearish signal.

-

ATR indicates market volatility. ATR multiplied by a coefficient serves as the stop loss range. This can effectively control single loss.

-

RSI indicates overbought/oversold status. Breakout trades signaled by stop loss price and EMA crossover must happen when RSI is not in overbought/oversold zone. This avoids false breakout.

-

Use previous period high/low points as take profit basis. Tracking take profit price can lock in more profits.

-

Strict stop loss/take profit rules. ATR-based stop loss controls risks and take profit locks in gains.

Entry signal triggers when price breaks out of EMA plus ATR stop loss range. For bullish signals, price needs to cross above the high point. For bearish signals, price needs to break below the low point.

Advantage Analysis

Advantages of this strategy:

-

Multiple indicators avoid false breaks and improve accuracy

-

ATR stop loss keeps losses at reasonable level

-

Dynamic take profit tracking maximizes profits

-

Strict rules facilitate risk control

-

Large optimization space for indicators and parameters to adapt to different markets

Risk Analysis

Risks of this strategy:

-

Profitability correlates with market volatility. Gains could be limited if trend is unclear or cycle is long.

-

Stop loss price may whipsaw before breaking out again. This leads to missing trends. Can relax stop loss price a bit.

3.There is potential for chasing in trending markets.

Optimization Directions

Optimization ideas:

-

Adjust MA, ATR parameters for different products and timeframes.

-

Add more indicators like MACD, KDJ for overbought/oversold.

-

Dynamically adjust ATR coefficient based on real-time ATR values for adaptive stops.

-

Establish combo systems with multiple timeframes. Different timeframe indicators can improve signal quality.

-

Utilize machine learning for parameters/indicators optimization to achieve best performance.

Summary

This strategy utilizes indicators for judgment and strict stop loss/take profit. It takes advantage of moving averages, ATR and RSI to determine market trends. With strict risk control, it can ride trends while managing risks. Further parameter and rules optimization can make it a long-term profitable trading system.

/*backtest

start: 2024-01-27 00:00:00

end: 2024-02-03 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title="UT Bot Strategy", overlay = true)

//CREDITS to HPotter for the orginal code. The guy trying to sell this as his own is a scammer lol.

// Inputs- 1