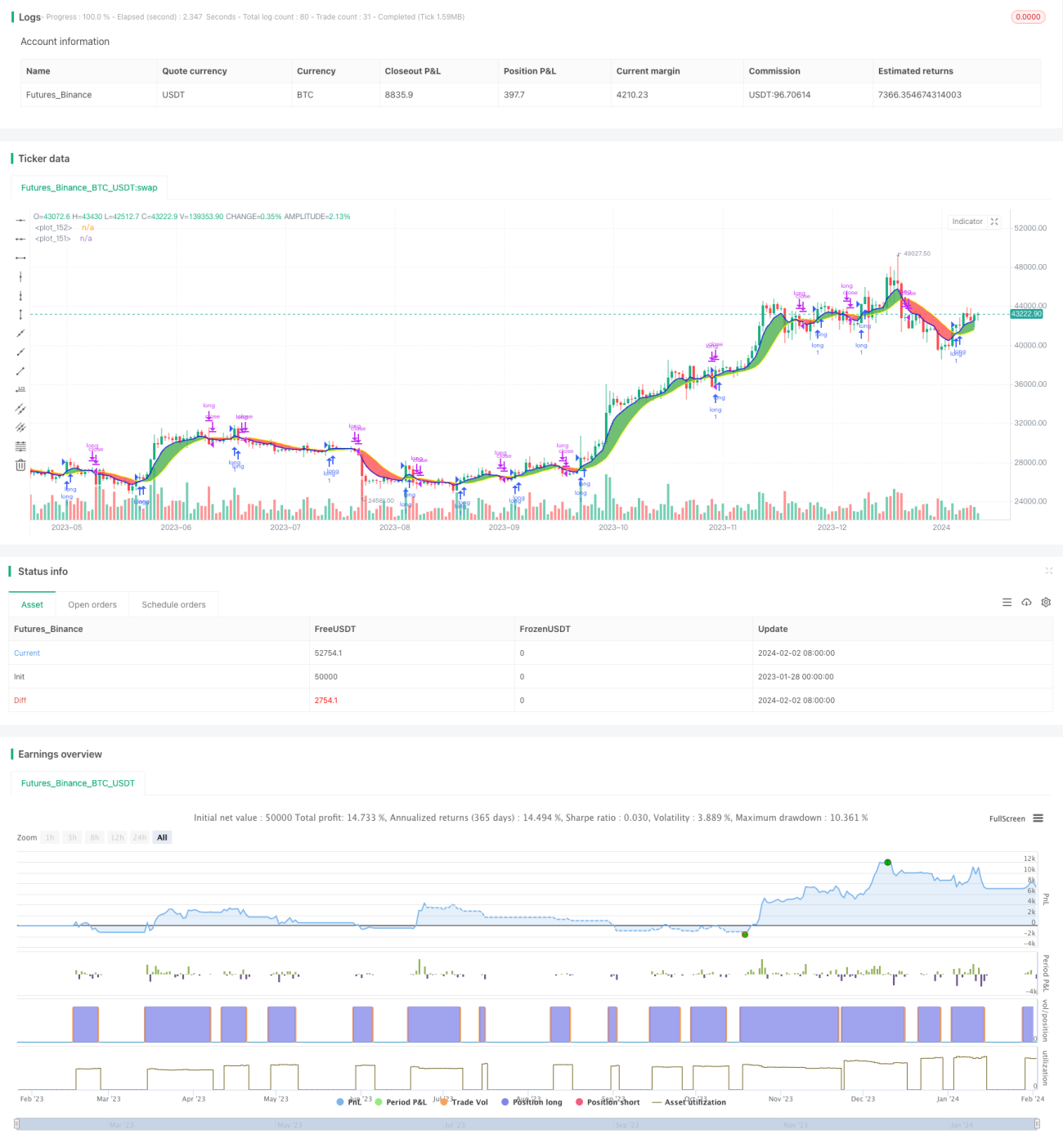

Dual Moving Average Cross Timeframe Trading Strategy

Overview

This strategy generates buy and sell signals by calculating two different types of moving averages across two different timeframes. It is a very good sandbox strategy to experiment with different moving averages and timeframe combinations.

Strategy Logic

This strategy uses two moving averages, a fast moving average and a slow moving average. The timeframe of the fast moving average should be greater than or equal to the chart timeframe. When the fast moving average crosses above the slow moving average, a buy signal is generated. When the fast moving average crosses below the slow moving average, a sell signal is generated.

Users can choose from various types of moving averages like SMA, EMA, KAMA etc, and the timeframes can be different. This allows experimenting with different combinations to find the optimal parameters.

Advantage Analysis

The biggest advantage of this strategy is that it allows easy adjustment of parameters to experiment with different combinations to find the best parameter settings.

Users can freely choose the type, length, timeframe of the two moving averages. The system calculates and displays results in real time. This is much easier than testing strategies with different parameter combinations.

Also, the built-in stop loss/take profit functionality helps to reduce risk and increase profitability.

Risk Analysis

The biggest risk of this strategy is that improper parameter settings may result in too frequent trading signals, thus increasing trading costs and slippage losses.

Also, dual moving averages themselves tend to give false signals. If parameters are not chosen correctly, buy/sell signals may not be reliable.

These risks can be reduced by optimizing parameters and combining with other indicators.

Optimization Directions

Consider adding other indicators like RSI to filter buy/sell signals on top of the dual moving averages. This can help reduce false signals.

Parameters of moving averages can also be optimized via training to find the best combinations. Machine learning methods may also be used to dynamically optimize the parameters.

Conclusion

This is an excellent sandbox for experimenting with dual moving averages. Its biggest advantage is fast iteration of different parameter combinations to find the best trading strategy. Of course there are also risks of improper parameter settings, which can be reduced by adding filtering indicators. Further optimizations of this strategy can potentially lead to even better trading performance.

/*backtest

start: 2023-01-28 00:00:00

end: 2024-02-03 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License https://creativecommons.org/licenses/by-sa/4.0/

// © dman103

// A moving averages SandBox strategy where you can experiment using two different moving averages (like KAMA, ALMA, HMA, JMA, VAMA and more) on different time frames to generate BUY and SELL signals, when they cross.

// Great sandbox for experimenting with different moving averages and different time frames.- 1