Adaptive Bollinger Bands Trend Tracking Strategy

1

Follow

1802

Followers

Overview

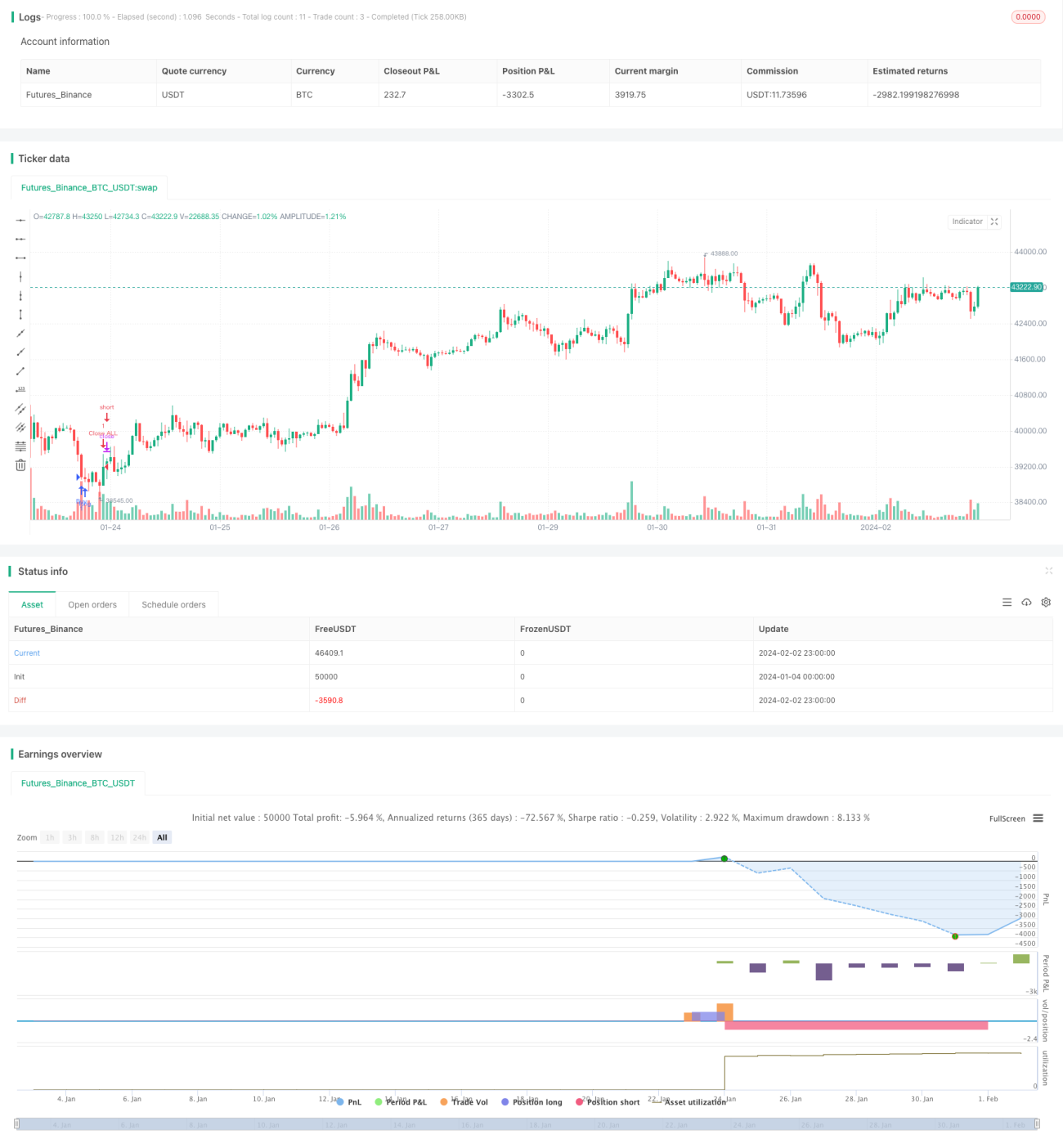

This strategy uses adaptive Bollinger Bands indicator to identify the trend direction and market orders to track the trend with stop loss for efficient trend trading.

Strategy Logic

- Calculate the middle, upper and lower bands of Bollinger based on a certain period

- Go long when the price breaks through the upper band and go short when breaks the lower band to track the trend

- Use market orders for fast entry

- Set stop loss and take profit for position management

Advantages

- Adaptive Bollinger Bands are sensitive to market volatility for fast judgement of trend reversal

- Market orders ensure fast entry with reduced slippage risk

- Automatic stop loss and take profit strictly control the risk and lock in profit

Risks

- Bollinger Bands has some lagging nature, cannot fully avoid false breakouts

- Market orders cannot control the execution price precisely

- Proper setting of stop loss and take profit levels is needed

Optimization Directions

- Adjust Bollinger parameters for better sensitivity in judging trends

- Add indicators like volume or MACD to filter false breakouts

- Optimize stop loss and take profit levels

Summary

This strategy makes full use of Bollinger Bands’ advantage in judging trend directions and combines fast-exit market orders for trend tracking from both sides, gaining excess returns under controlled risk. Further improvements like optimizing Bollinger parameters, adding filtering indicators and adjusting stop loss/take profit logic can lead to better strategy performance. With clear logic and easy implementation, it is an efficient and reliable trend tracking trading strategy.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1