The Quantitative Trading Strategy Based on Dynamic Moving Average Breakthrough Entry

Overview

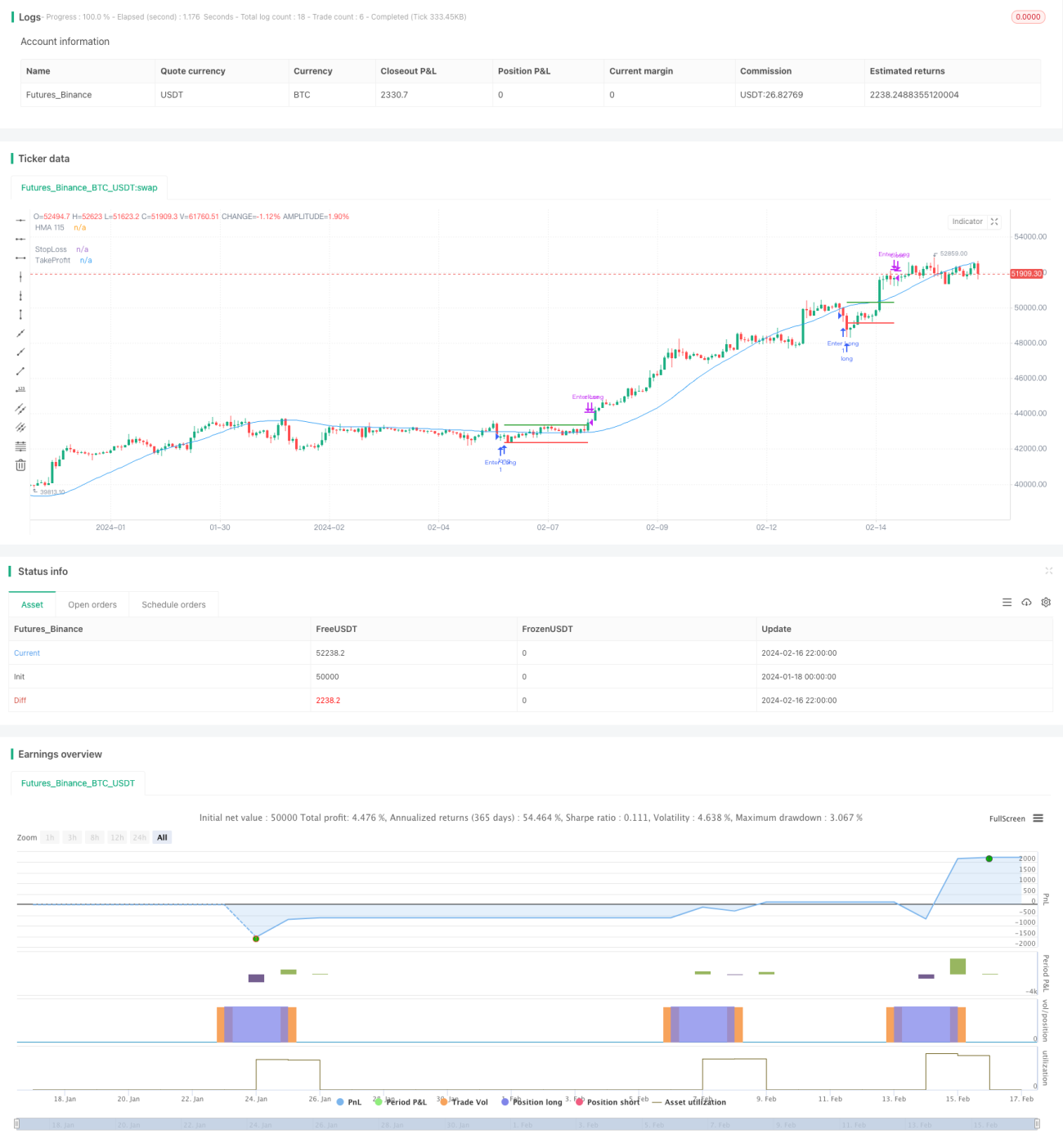

The name of this strategy is "The Quantitative Trading Strategy Based on Dynamic Moving Average Breakthrough Entry and Fixed Profit-taking/Stop-loss Exit". The main idea of this strategy is to open long positions when the closing price is below the 115-period Hull Dynamic Moving Average on every Monday, and unconditionally close positions on every Wednesday afterwards, with fixed ratios of profit-target and stop-loss set simultaneously.

Principles

This strategy is mainly designed based on the indicator signals of Hull Moving Average and periodic trading rules.

Firstly, during the trading session on every Monday, long positions will be opened if the closing price is below the 115-period Hull Moving Average. Compared to common moving averages, Hull Moving Average responds faster to price changes and identifies trends more sensitively. Therefore, the indicator signals can improve the accuracy of market entry.

Secondly, positions will be closed unconditionally during the trading sessions on every Wednesday. This periodic operation approach can avoid being impacted by contingent events and reduce the probability of drawdowns. Meanwhile, fixed ratios of stop-loss and profit-target are set to control the risk and reward of every trade.

Finally, as each trade holding period is relatively short with higher trading frequency, it can adjust positions to some extent and decrease single trade risk.

Advantage Analysis

This strategy has the following advantages:

-

Using Hull Moving Average as the entry signal indicator improves the accuracy of timing market entry and captures trend opportunities.

-

The periodic exit method can avoid risks from irrational behaviors and reduce drawdown probability.

-

The fixed profit-target and stop-loss points can control risk-reward ratio of each trade effectively.

-

High trading frequency is beneficial to adjust positions and decrease single trade risk.

-

The trading rules are simple and easy to understand and implement, which is suitable for algorithmic quantitative trading.

Risk Analysis

This strategy also has some risks:

-

Prolonged consolidation in the market may lead to higher probability of being trapped after entry.

-

The fixed profit-target and stop-loss points lack flexibility and may exit position too early or too late.

-

Periodic exit may lead to huge losses if contingent events happen.

-

Frequent trading increases cost and slippage influence.

-

Improper parameter settings (like period numbers) may affect strategy performance.

Some optimization measures can be considered to reduce the above risks:

-

Judge market condition before entry to avoid entering consolidation phases.

-

Set dynamic or multiple fixed ratios for profit-taking and stop-loss.

-

Suspend trading around significant events to avoid extreme volatility.

-

Lower trading frequency appropriately to reduce cost and slippage.

-

Optimize parameter settings and do robustness test to make the strategy more stable.

Optimization Directions

This strategy can be further optimized in the following aspects:

-

Use machine learning models to optimize parameters of moving average dynamically for more accurate signals.

-

Try combining multiple indicators to design more complex entry and exit rules.

-

Design adaptive profit-taking and stop-loss mechanisms according to different periods and market environments.

-

Incorporate risk management models for better capital management.

-

Design rights adjustment module to handle events like stock splits smoothly.

-

Add real trading verification module to test strategy's performance in live markets.

By organically combining machine learning, indicator portfolio, adaptive profit-taking/stop-loss, risk management and other methods, this strategy can achieve stronger stability and profitability. Meanwhile, adding real trading verification mechanisms is also important for further perfecting the strategy. These are the main optimization directions for this strategy.

Conclusion

This strategy is designed based on the ideas of Hull Dynamic Moving Average indicator signal entry and fixed cycle exit. It has advantages like accurate signals and low drawdown probability, while controlling single trade's profit-taking and stop-loss. But problems like being trapped and improper profit-taking/stop-loss settings also exist. Future optimization directions include introducing machine learning and more complex multi-indicator combinations for entry, designing adaptive profit-taking/stop-loss mechanisms, adding rights adjustment and real trading verification modules, etc. By comprehensively adopting these measures, the stability and profitability of this strategy will be enhanced.

- 1