Volatility Breakout Reversal Trading Strategy

Overview

The Volatility Breakout Reversal Trading Strategy is a reversal trading strategy that tracks price channels with adaptive moving stop profit and stop loss points. It establishes long or short positions when prices break out of the channels calculated based on volatility.

Strategy Logic

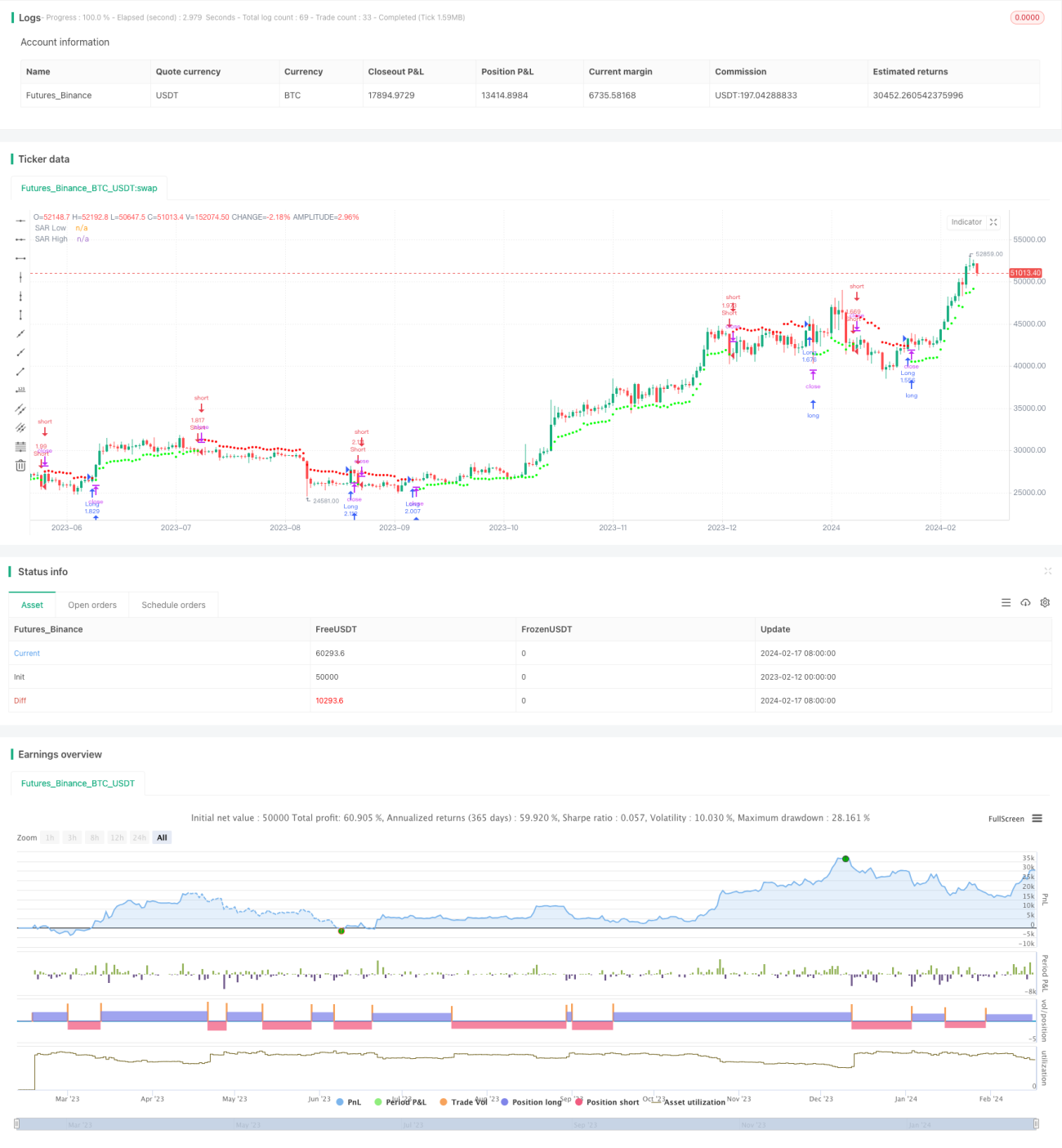

The strategy first uses Wilder's Average True Range (ATR) indicator to measure price volatility. It then calculates the Average Range Constant (ARC) based on the ATR values. The ARC represents half the width of the price channel. Next, the upper and lower bands of the channel are calculated as the stop profit and stop loss points, also known as the SAR points. When prices break above the upper band, a short position is opened. When prices break below the lower band, a long position is opened.

Specifically, the ATR over the last N bars is first computed. The ATR is then multiplied by a factor to obtain the ARC, which controls the width of the price channel. Adding the ARC to the highest closing price over N bars gives the upper band of the channel, or the high SAR. Subtracting the ARC from the lowest closing price gives the lower band, or the low SAR. If prices close above the upper band, a short position is taken. If prices close below the lower band, a long position is taken.

Advantages

- Uses volatility to calculate adaptive channels that track market changes

- Reversal trading suits trend reversal markets

- Moving stop profit and stop loss locks in profits and controls risk

Risks

- Reversal trading prone to being trapped, parameters need proper tuning

- Sharp volatility moves may prematurely close positions

- Improper parameters may cause over-trading

Solutions:

- Optimize ATR period and ARC factor for reasonable channel width

- Add trend filter for entry signals

- Increase ATR period to lower trade frequency

Enhancement Opportunities

- Optimize ATR period and ARC factor

- Add entry conditions like MACD

- Incorporate stop loss strategy

Conclusion

The Volatility Breakout Reversal Trading Strategy uses channels to track price changes and reverses positions when volatility spikes. It works well in range-bound markets with reversals, generating good returns if reversal points are accurately identified. Care should be taken to avoid stops being too wide and overfitting parameters.

- 1