EMA Breakthrough Trap Strategy

Overview

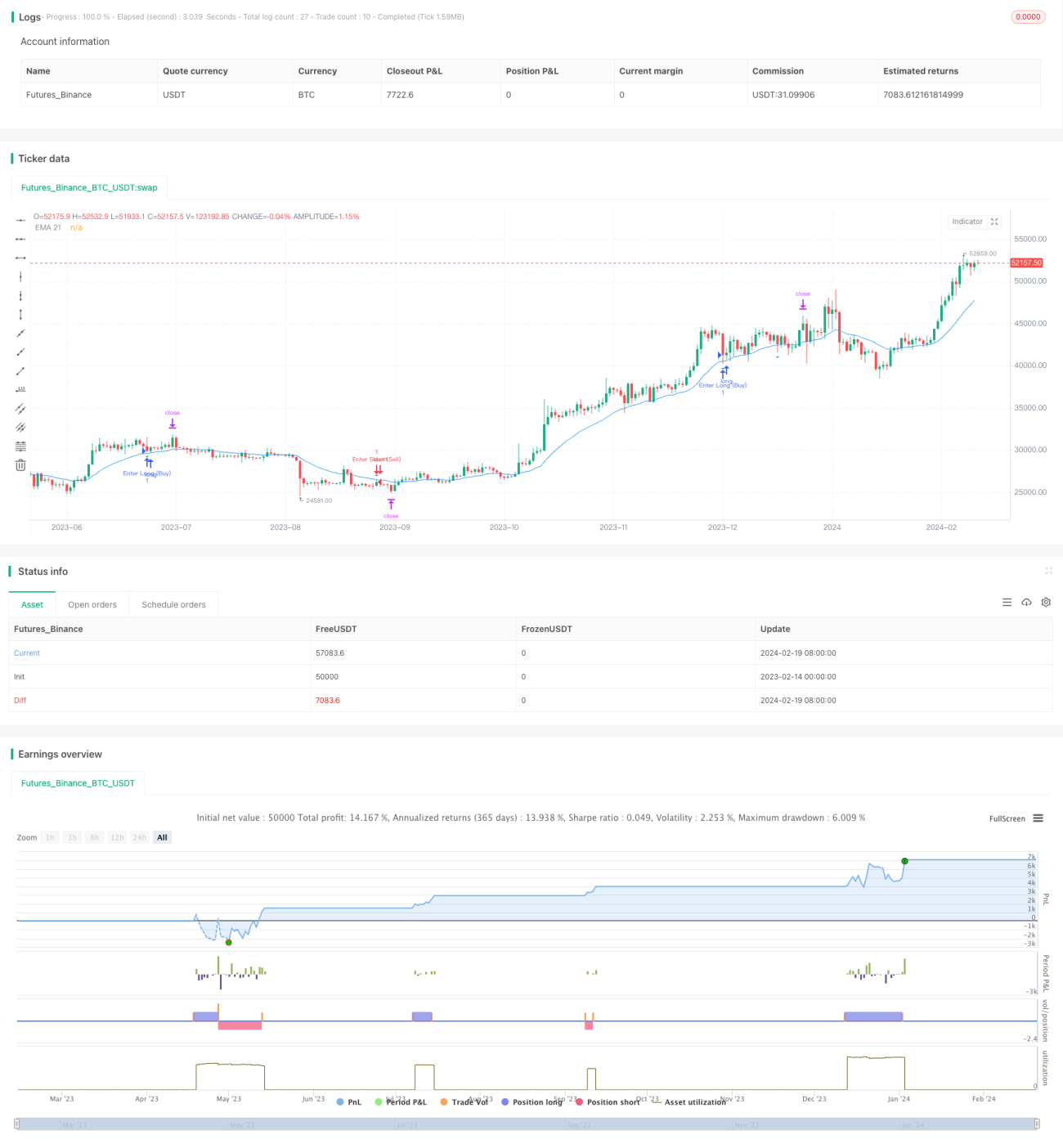

The EMA Breakthrough Trap Strategy is a versatile trading tool suitable for multiple timeframes including 1-minute and 1-hour charts. It utilizes the 21-day EMA to identify significant market trends, complemented by ATR-based identification of potential bull and bear traps. Notably, it achieves an impressive profitability rate averaging around 85% across different frames and peaking at 88% in optimal conditions.

Strategy Logic

The strategy first calculates the 21-day Exponential Moving Average (EMA) to judge the overall trend and direction. Then it calculates the recent N days' highest and lowest prices (N is an adjustable parameter). If the closing price is higher than the previous day's highest price, and the subsequent low point has fallen below the highest price multiplied by the ATR indicator, while the closing price has fallen below the 21-day line, a bull trap signal is determined. The judgment logic for bear trap signals is similar.

Once a trap signal is identified, set the stop loss and take profit based on 80% of the distance between the recent highest and lowest prices, and take the reverse position. For example, after identifying a bull trap signal, take a short position and set the take profit and stop loss; after identifying a bear trap signal, take a long position and set the take profit and stop loss.

Advantage Analysis

- Uses EMA to judge trends, high reliability

- Leverages ATR indicator to identify traps accurately

- High profitability up to 85%

- Applicable to multiple timeframes

- Adjustable parameters provide optimization space

Risk Analysis

- EMA judgement may fail during major trend changes

- Inappropriate ATR parameter setting may miss traps

- Unreasonable stop loss/take profit placement may reduce profits or increase losses

- High trading costs and slippage impacts for high frequency trading

Risks can be reduced by optimizing EMA parameters, adjusting ATR coefficients, dynamic trailing stop loss etc.

Optimization Directions

- Optimize ATR parameters and EMA periods to improve identification accuracy

- Add dynamic stop loss mechanism

- Incorporate other indicators to confirm signals

- Test applicability across more timeframes

Conclusion

The EMA Breakthrough Trap Strategy integrates the advantages of trend judgment and trap identification. With low drawdowns and high profitability, it is suitable for various trading styles and is a highly efficient recommended strategy. Further enhancements in stability and profitability space can be achieved through parameter and mechanism optimization.

- 1