Super Trend Daily Reversal Strategy

Overview

The Super Trend Daily Reversal Strategy is a quantitative trading strategy that uses the Super Trend indicator to determine market trends, combines price breakthrough and average true range to calculate stop loss, and uses the price change rate indicator to filter Super Trend signals. This strategy is suitable for daily and higher time frames and can be used in markets like cryptocurrencies and stocks.

Strategy Logic

The core indicator of this strategy is the Super Trend indicator. The Super Trend indicator is based on Average True Range (ATR) and can more clearly determine the direction of market trends. A breakdown of the Super Trend upper rail is a short signal, and a breakdown of the lower rail is a long signal.

The strategy uses the Price Change Rate indicator (ROC) to filter the Super Trend indicator to avoid invalid signals. Only participate in Super Trend signals when price volatility is large, otherwise do not participate.

For stop loss, the strategy provides two stop loss methods: fixed stop loss percentage and ATR based adaptive stop loss. Fixed stop loss is simple and direct. ATR stop loss can adjust the stop loss range according to market volatility.

The entry conditions are a reversal of the Super Trend indicator and the price change rate indicator passes the filter. The exit conditions are that Super Trend reverses again or breaks through the stop loss line. The strategy adheres to the trend tracking principle and only allows one position in each direction.

Advantage Analysis

The biggest advantage of this strategy is that the Super Trend indicator has higher clarity and stability in judging trend direction compared to ordinary moving averages, with less noise. In addition, the price change rate indicator effectively filters out some false signals.

The ATR adaptive stop loss mechanism also allows the strategy to adapt to a wider market environment. The stop loss will automatically widen during increased volatility to maximize profits.

From the test results, this strategy performs exceptionally well in a bull market. The win rate is very high in long-term trends of significant magnitude, with long consecutive profitable cycles.

Risk Analysis

The main risk faced by this strategy is misjudgment of trend reversal, which may miss reversal signals or generate unnecessary reversal signals. This often happens when prices oscillate and consolidate around key support/resistance areas.

In addition, a stop loss that is set too wide can also lead to greater losses. ATR stop loss adjusts according to market volatility, so stops may be pulled wider during market events.

To address these risks, the ATR calculation period can be shortened appropriately or the ATR stop loss multiplier adjusted. Additional indicators can also be added to determine key support/resistance areas to avoid misleading signals from those areas.

Optimization Directions

The strategy can be optimized in the following aspects:

-

Adjust the parameters of the Super Trend indicator to optimize the ATR period and ATR multiples to make the Super Trend line smoother.

-

Adjust the parameters of the price change rate indicator to optimize the period and change rate threshold to reduce false signals.

-

Try different stop loss mechanisms such as trailing stops, or optimize the stop loss amplitude of fixed stops.

-

Add additional judgment indicators to determine key support/resistance and avoid misjudgment of trend reversals.

-

Test parameter settings and effects on different products to find the optimal parameter combination.

-

Conduct backtest optimization to find the best parameter settings.

Conclusion

Overall, the Super Trend Daily Reversal Strategy is a relatively stable and reliable trend following strategy. It combines the Super Trend indicator and the price change rate indicator for filtering, which can effectively identify the direction of medium and long term trends. The ATR adaptive stop loss mechanism also enables it to adapt to most market environments. Through further optimization of parameter settings and added judgment indicators, the stability and profitability of this strategy can be improved.

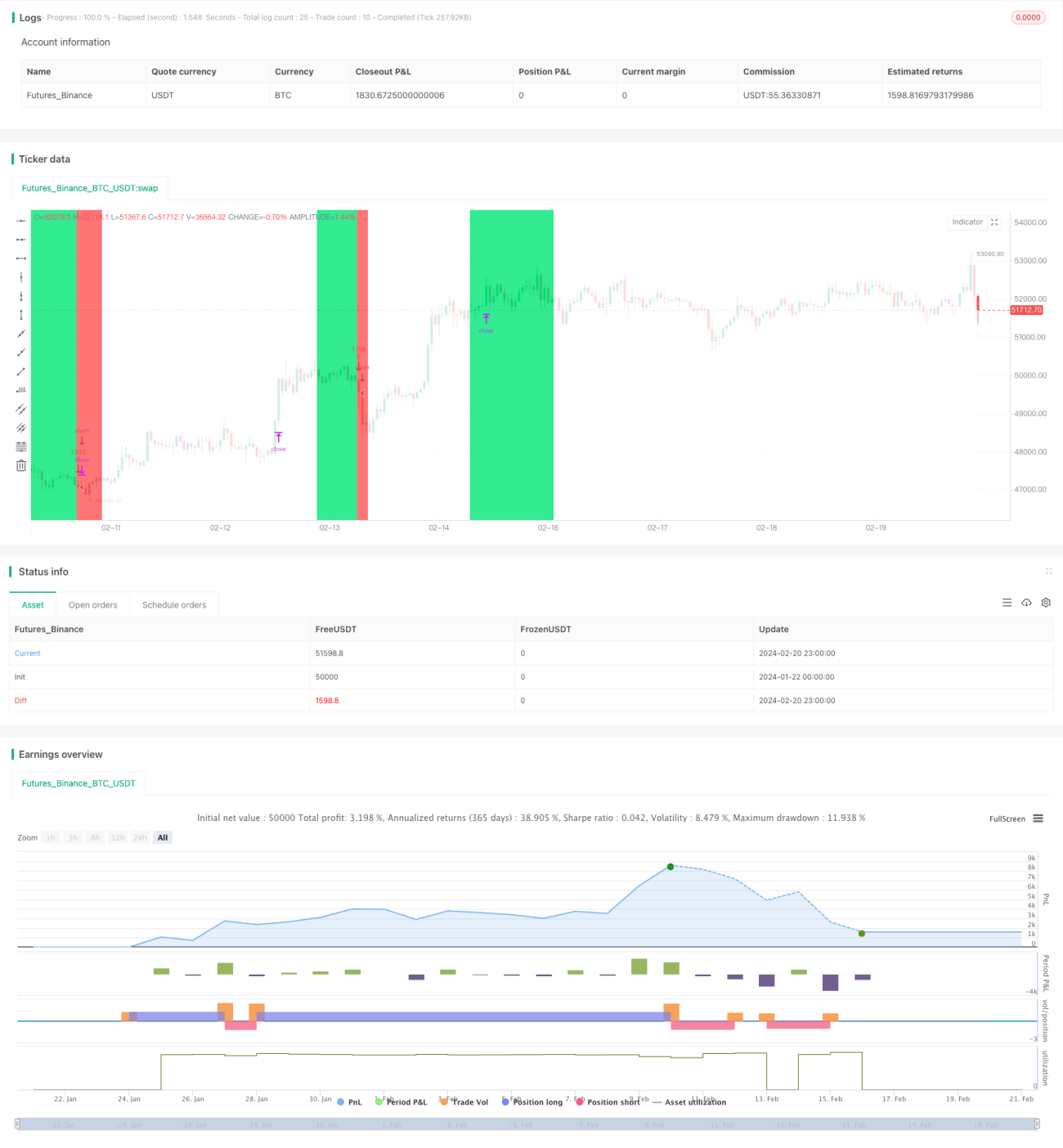

/*backtest

start: 2024-01-22 00:00:00

end: 2024-02-21 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Super Trend Daily BF 🚀", overlay=true, precision=2, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.075)

/////////////// Time Frame ///////////////- 1