Dynamic Regression Channel Strategy

Overview

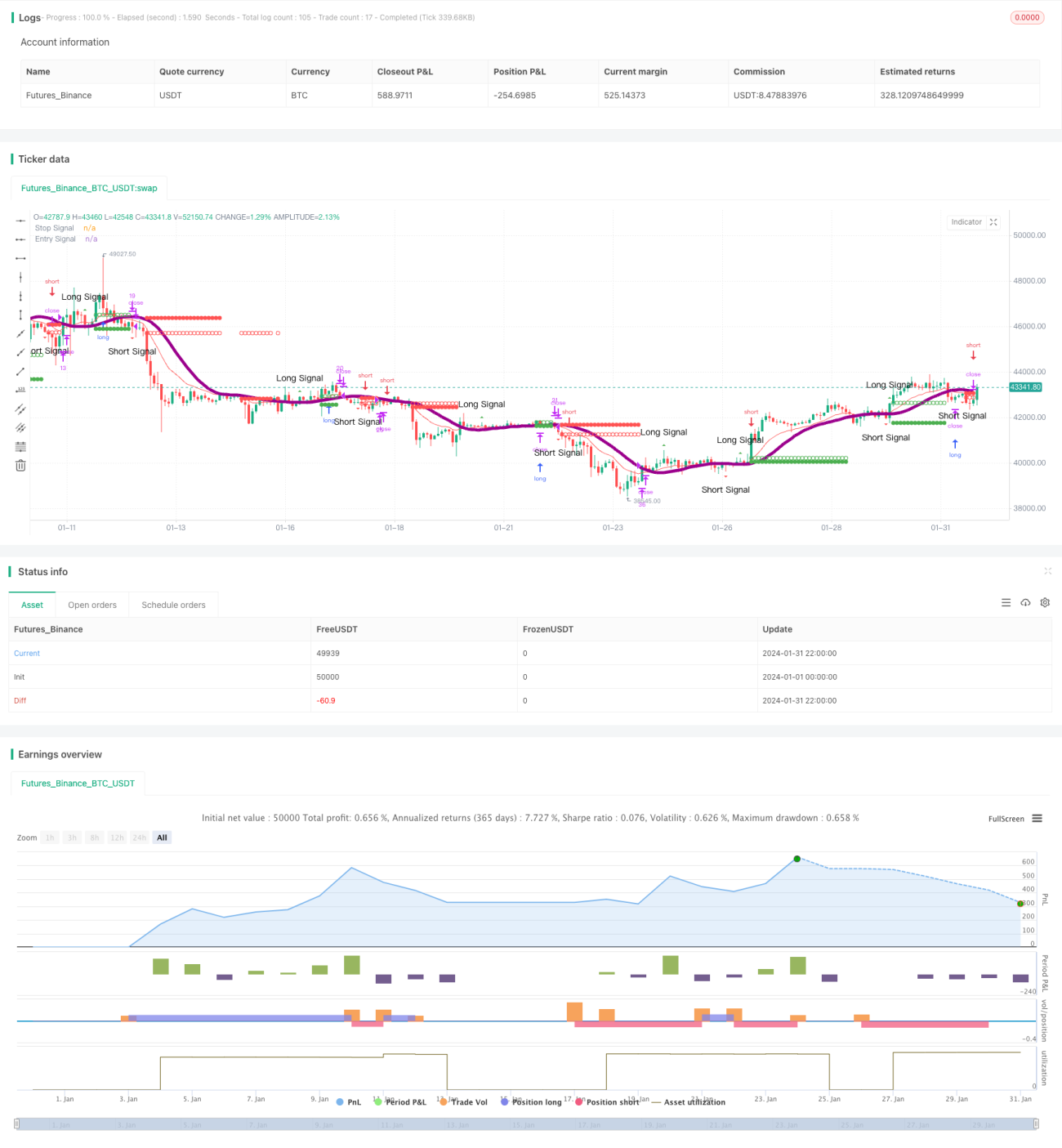

The Dynamic Regression Channel strategy utilizes linear regression analysis of price trends combined with dynamic stop loss to implement trend following in quantitative trading. The strategy employs linear regression to plot a price channel and generate buy and sell signals when prices break out of the channel. At the same time, the strategy tracks prices in real-time to update stop loss levels to lock in profits.

Strategy Logic

The strategy first calculates a linear regression curve of prices to determine if prices break out above or below the regression channel. When prices rise above the upper rail of the channel, a buy signal is generated. When prices fall below the lower rail, a sell signal is triggered.

After entering a position, the strategy keeps tracking if prices break the stop loss moving average line. For long orders, if prices fall below the stop loss line, a stop loss sell order will be issued. For short orders, if prices rise above the stop loss line, a stop loss buy order will be triggered. This locks in profits and controls risks.

It is important to note that if prices break the channel again reversing direction, the strategy will immediately flatten the original position and switch to trade in the opposite direction.

Advantage Analysis

This strategy combines both trend following and mean reversion concepts, riding with the overall price trend while catching short-term reversals. The dynamic stop loss also effectively controls risks. As such, it is a balanced trading approach.

Compared with simple moving average strategies, the Dynamic Regression Channel Strategy is more sensitive to price changes and can reduce mistrades. In addition, the strategy only trades on breakouts of the channel, avoiding unrestrained aggressive trades.

Risk Analysis

The main risk lies in inaccurate fitting of the regression curve. If the channel range is set improperly, being too wide or too narrow, it will increase invalid trades or miss trading opportunities.

In addition, proper stop loss positioning is critical. A stop loss too close to market prices is prone to premature liquidation by short-term volatility while a stop loss too far away cannot serve its purpose of risk control. Fine tuning is needed across different products.

Optimization

Consider auto-optimizing parameters for different periods or products to make the regression channel and stop loss line fit better to price trends. For instance, machine learning algorithms can potentially be leveraged to train optimal parameters.

Alternatively, different types of regression such as polynomial regression and locally weighted regression can be tested to improve fitting. Combining multiple regression metrics to construct trading rules may also enhance strategy stability.

Conclusion

The Dynamic Regression Channel Strategy skillfully utilizes both trend following and mean reversion techniques, riding the overall price trend while capturing short-term reversals. Proper tuning of the key regression channel and stop loss parameters is vital to strategy performance. Further refinements can be made through parameter optimization and model iteration.

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Estratégia de Regressão Linear", shorttitle="Regressão Linear Estratégia", overlay=true, initial_capital = 100, default_qty_value = 10, default_qty_type = strategy.percent_of_equity)

// média móvel exponencial para definição de regressao linear- 1