Rainbow Oscillator Trading Strategy

Overview

The Rainbow Oscillator trading strategy mainly uses multiple smoothed moving averages and oscillation indicators to build a multi-layer oscillation channel and generate clear long/short signals. It belongs to the trend-following strategy category. This strategy combines RSI, CCI, Stochastic and MA composite indicators to determine the overall market trend and overbought/oversold areas. It is a multi-factor rating strategy.

Principles

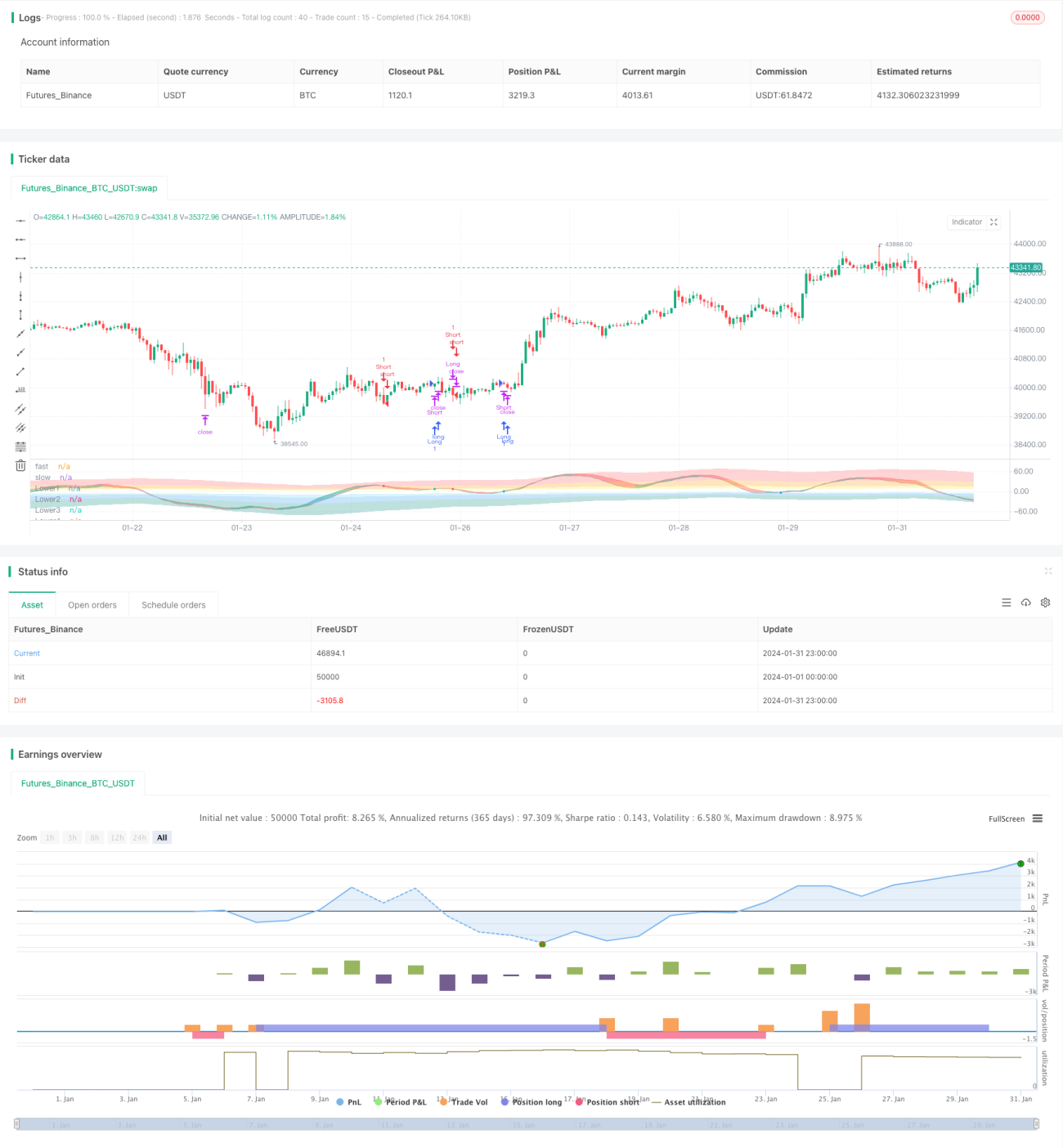

- Calculate the weighted average of RSI, CCI and Stochastic to build a combined oscillation indicator called Magic;

- Apply exponential smoothing to Magic multiple times to generate two lines called sampledMagicFast and sampledMagicSlow;

- sampledMagicFast represents the fast EMA line, sampledMagicSlow represents the slow EMA line;

- A buy signal is generated when sampledMagicFast crosses above sampledMagicSlow;

- A sell signal is generated when sampledMagicFast crosses below sampledMagicSlow;

- Calculate the direction of the last bar's sampledMagicFast relative to previous bar to determine the current trend;

- Determine entry and exit points based on trend direction and crossing situation between sampledMagicFast and sampledMagicSlow.

Advantages

- Combining multiple indicators to determine overall market trend improves signal accuracy;

- Smoothed MA filters out noise effectively;

- Multi-layer oscillation signals provide clear operation guidance;

- Can be configured for trend-following or mean-reversion by enabling/disabling trend filter;

- Customizable overbought/oversold strength for flexibility.

Risks

- Over-smoothed curves may cause missing best entry points;

- Improper overbought/oversold area setting may keep position closed for too long;

- Failure of some factors in the rating model may weaken signals.

Solutions:

- Optimize parameters for appropriate smoothing extent;

- Adjust overbought/oversold area strength to reduce time in flat position;

- Test and weight each indicator by its predictive power.

Optimization Directions

- Dynamically adjust indicator parameters based on market conditions;

- Introduce machine learning methods to auto optimize indicator combinations;

- Add factors like volume and volatility filters to entry signals.

Conclusion

The Rainbow Oscillator strategy combines signals from multiple indicators and uses exponential smoothing to improve stability. It can be configured for both trending and sideways markets, or for specific products. Further improvements can be made by parameter tuning and indicator expansion. Overall this is a clear, easy-to-use strategy.

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © businessduck

//@version=5

strategy("Rainbow Oscillator [Strategy]", overlay=false, margin_long=100, margin_short=100, initial_capital = 2000)

bool trendFilter = input.bool(true, 'Use trend filter')

float w1 = input.float(0.33, 'RSI Weight', 0, 1, 0.01)

float w2 = input.float(0.33, 'CCI Weight', 0, 1, 0.01)

float w3 = input.float(0.33, 'Stoch Weight', 0, 1, 0.01)

int fastPeriod = input.int(16, 'Ocillograph Fast Period', 4, 60, 1)

int slowPeriod = input.int(22, 'Ocillograph Slow Period', 4, 60, 1)- 1